The State of Bitcoin Mining in Bolivia (2026)

A 2,400% hashrate spike built on subsidized gas, a new government, and one European operator.

This article is part of Hashrate Index's State of Bitcoin Mining in Latin America series.

TLDR

- Bolivia's +2,400% hashrate spike was pure arbitrage on subsidized gas ($1.30/MMBTU vs. $8–12 market) — and the Q2 2026 pullback shows the market already pricing in its expiration.

- Alps (Italian data center group) is the only operator with a durable thesis: reviving a 127 MW idle Cochabamba thermal plant via a USD auto-consumption model that bypasses Bolivia's boliviano currency crisis entirely.

- Beyond the gas window, Bolivia has genuine long-term energy assets — COBEE's 188 MW Zongo hydro cascade, Uyuni solar, and Laguna Colorada geothermal — plus a new government actively opening the door to foreign capital.

- The real Bolivia opportunity mirrors how Paraguay became the #4 mining country: structural energy surplus + government willing to build a legal framework + serious institutional capital. Bolivia now has two of three, and Alps is building the third.

Introduction

Bolivia's Bitcoin mining story is one of the most quiet ones in Latin America, and one of the least understood outside the region.

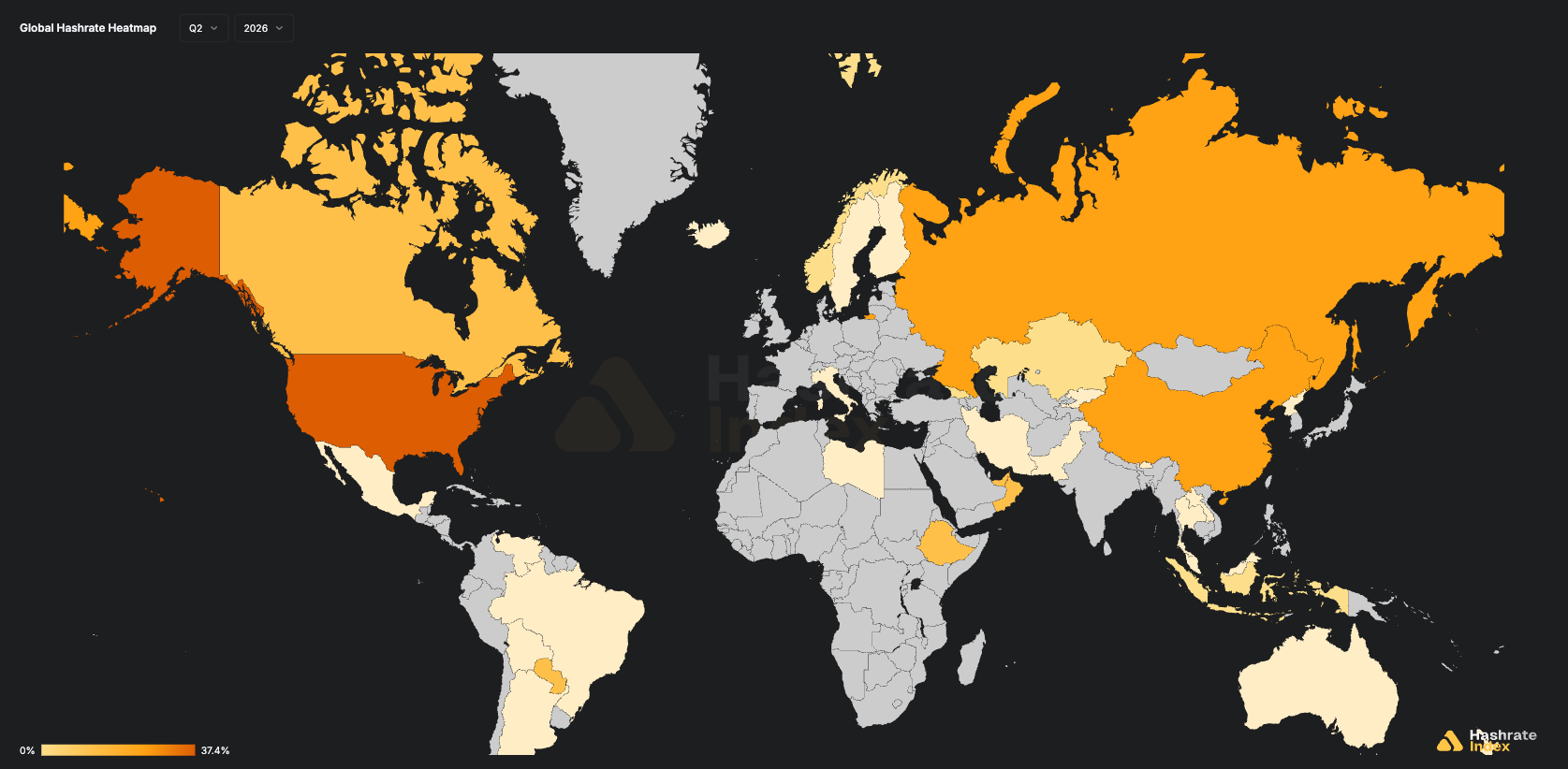

In the span of roughly eighteen months through early 2026, the country went from having virtually no trackable mining presence on the Hashrate Index Global Hashrate Heatmap to a +2,400% year-over-year hashrate spike that made it one of the fastest-growing mining markets on earth. By Q2 2026, that growth had begun to pull back. The divergence between the explosive headline and the subsequent retreat reveals something important about what Bolivia is (and is not) as a bitcoin mining market.

Bolivia is not Paraguay. It does not have a chronic hydro surplus from a long-depreciated river dam that prices power at near-zero marginal cost. What Bolivia has is a grid that runs 70% on gas supplied at a heavily subsidized $1.30/MMBTU by the state oil company YPFB, when the international LNG market trades at $8-12/MMBTU. That spread created cheap electricity, cheap enough to mine Bitcoin profitably, and operators found it.

The problem is that the spread has an expiration date. Bolivia is on a trajectory toward net gas importer status within 2-5 years. When that transition happens, the economics that made the hashrate spike possible will deteriorate sharply.

But Bolivia's energy story does not end with the gas subsidy. Italian data center group Alps, together with Qurubiqa, is looking to revive a 127 MW gas thermal plant in Cochabamba sitting essentially idle because Bolivia's currency crisis makes it impossible to operate commercially. Bolivia also has hydroelectric cascades, an altiplano solar resource that rivals the Atacama, and a new right-leaning government that is actively seeking foreign capital to solve its dollar-liquidity crisis. It is this combination (idle industrial energy infrastructure and a government that needs USD inflows) that brought Alps and Qurubiqa to Cochabamba, and it could make Bolivia's mining market far more durable than the 2,400% spike highlighted in our State of Bitcoin Mining in LATAM 2026 article.

The Grid: Understanding Bolivia's Energy Matrix

Bolivia's Sistema Interconectado Nacional (SIN) is managed by the CNDC (Comite Nacional de Despacho de Carga) and regulated by the AETN (Autoridad de Fiscalizacion de Electricidad y Tecnologia Nuclear). Demand has grown 85% since 2010, from 5,664 GWh to approximately 10,450 GWh in 2024. The dominant operator is ENDE Corporacion, the state-owned utility, with its ENDE Andina subsidiary alone responsible for 57% of all energy injected into the system.

| Source | Share of Generation | Installed Capacity | Key Constraint |

|---|---|---|---|

| Thermoelectric (gas) | ~70% | ~1,560 MW (ENDE Andina) | Gas supply from YPFB at $1.30/MMBTU vs $8-12 market |

| Hydroelectric | ~20% | ~472 MW (COBEE + ENDE Corani) | Seasonal hydrology, aging infrastructure |

| Renewables (solar/wind) | ~10% | ~197 MW (Uyuni solar + Qollpana/Santa Cruz wind) | No BESS, curtailment risk rising |

The Thermal Backbone

The three ENDE Andina plants in Cochabamba, Tarija, and Santa Cruz are the load-bearing columns of the Bolivian grid. All operate on combined-cycle gas technology, converting exhaust heat into additional steam generation to maximize efficiency from each cubic meter of YPFB gas.

| Plant | Location | Capacity | Configuration |

|---|---|---|---|

| Termoelectrica Entre Rios | Cochabamba | 526.77 MW | 4 open-cycle + 3 combined-cycle blocks |

| Termoelectrica del Sur | Yacuiba, Tarija | 505.83 MW | 4 combined-cycle blocks |

| Termoelectrica Warnes | Warnes, Santa Cruz | 527.41 MW | 1 open-cycle + 4 combined-cycle blocks |

Gas is supplied by YPFB at approximately $1.30/MMBTU under a subsidized domestic pricing structure. The international market price for LNG has traded between $8 and $12/MMBTU. That $6.70-$10.70/MMBTU spread is both the source of Bolivia's cheap industrial electricity and the structural vulnerability that defines its medium-term energy outlook.

The Renewable Layer

Bolivia's renewable portfolio is real but limited in scale. COBEE's Sistema Zongo hydroelectric cascade (10 Pelton-turbine plants on the Zongo River, 188 MW total, operational since the 1930s) and ENDE Corani's Misicuni (120 MW, 3 Pelton turbines) and San Jose projects (124 MW cascade) provide approximately 472 MW of hydro capacity that generates at near-zero marginal cost. These assets are the foundation of Bolivia's durable mining opportunity.

On renewables, ENDE Guaracachi operates 108 MW of wind capacity across three Santa Cruz parks using 30 Vestas 3.6 MW turbines, and 62.5 MW of solar at the Uyuni salt flat (over 3,700 metres above sea level, requiring IP54-rated equipment and specialized inverter derating). Laguna Colorada in Potosi hosts a 5 MW geothermal pilot plant targeting a 100 MW commercial expansion. None of these assets yet have the storage or grid integration needed to serve as reliable baseload for industrial mining operations, but they represent the long-term foundation once battery storage policy catches up.

The Structural Crisis: Gas Depletion

Bolivia's gas reserves are depleting faster than new fields are being discovered. The country's thermoelectrics consume approximately 1,500 million cubic metres of gas per year. Bolivia is approaching net gas importer status within a 2-5 year horizon, and the government is already studying reversed pipeline flows to import Argentine gas from Vaca Muerta via existing Tarija infrastructure.

The financial arithmetic is stark. At market import prices, the annual cost of running the thermoelectric fleet would increase by approximately $400 million. ENDE's total annual profit is roughly $160 million. Something has to give: either industrial tariffs rise significantly, the state absorbs a structural energy deficit it cannot afford, or the generation mix shifts away from gas. For mining operations built on the subsidized thermal rate, the clock is running.

The Hashrate Spike: What Actually Happened

Bolivia's +2,400% year-over-year hashrate growth through early 2026 was a rational response to an identifiable spread. Operators found subsidized electricity priced at roughly $0.03-0.06/kWh equivalent and moved machines in quickly to capture the arbitrage before conditions changed. The Q2 2026 pullback was the market pricing in the end of the subsidy before the subsidy formally ends.

This is not unique to Bolivia. It is exactly the same dynamic that played out in countries like Iran, Kazakhstan, and Kosovo over the previous decade: a policy-created energy discount attracts mining capital, the government eventually adjusts tariffs or restricts access, and the hashrate that arrived fast departs just as quickly. The operators who built the 2,400% spike were mostly capturing short-term opportunity, not building infrastructure.

The question for Bolivia's mining market is whether there is a durable layer underneath the arbitrage. The answer depends almost entirely on whether private capital can access Bolivia's stranded industrial energy assets at USD-denominated terms before the gas subsidy unwinds.

Alps: Bolivia's First Industrial-Scale Bitcoin Mining Operator

In the broader context of Bolivia's volatile hashrate data, one operator stands apart. Alps, the Italian mining and data center company co-founded by CEO Francesco Buffa and CFO Francesca Failoni, is not in Bolivia chasing the subsidized gas spread. Alps is partnering with Qurubiqa in Bolivia to revive a 127 MW gas thermal plant in the Cochabamba region that’s sitting completely idle, a stranded asset created by Bolivia's currency crisis. Alps now holds a first-mover advantage in the market to lead the first Bitcoin mining operation at scale that could auto-consume energy on-site and pay it in USD, which is precisely the mechanism Bolivia needs to monetize that asset.

It is a meaningfully different thesis from every other operator in the country.

The Cochabamba Opportunity: A Currency Problem Solved by Bitcoin Mining

The 127 MW thermal plant Alps identified operates on a structural paradox. The plant pays for its gas input in US dollars but was selling electricity to the Bolivian grid in bolivianos at the official exchange rate of 7:1. The real market rate has traded closer to 12-13:1. At that distortion, operating the plant commercially was a guaranteed way to destroy value. The plant went idle not because of any technical failure but because Bolivia's monetary system made it economically irrational to run.

Alps' auto-consumption model dissolves that paradox. By consuming the plant's output directly for Bitcoin mining operations, Alps pays for energy in USD at a negotiated rate and the plant operator receives hard currency. The Bolivian government, which needs USD inflows to defend its foreign reserves, gets an industrial operator that brings dollars into the country and keeps a stranded asset generating economic activity. Neither party touches the boliviano exchange rate problem.

"Bolivia has a 'big opportunity' if it avoids the mistakes that other markets made by attracting operators who are not serious. The opportunity here is not the gas subsidy. It is that we can help Bolivia solve a real economic problem with a model that benefits everyone."

— Francesco Buffa, CEO, Alps

The Deployment: From 30 MW to 127 MW

Alps’s initial deployment targets 30 MW of capacity at the Cochabamba site, by relocating machines from their Paraguay operations, a pragmatic decision that solves two problems simultaneously: reducing stranded capital in Paraguay as that market tightens, and seeding Bolivia with proven hardware that does not require new customs clearance.

The scaling roadmap is ambitious. Alps targets 45 MW by end of 2026, representing full utilization of one turbine at the Cochabamba plant. The ultimate objective is the full 127 MW, which would make Alps by far the largest Bitcoin mining operator in Bolivia and one of the largest in South America outside Paraguay.

Two additional sites are under evaluation: one in the highlands near La Paz and one near the Argentine border, both potentially accessing different energy sources and logistical corridors.

Why Alps is Positioned as a First Mover, Not Just an Early Entrant

The distinction between a first mover and an early entrant matters in mining markets. Early entrants capture the initial arbitrage and leave when conditions change. First movers build the infrastructure, relationships, and regulatory understanding that create durable competitive advantages.

Alps qualifies as a first mover in Bolivia for three reasons. First, its autoconsumption model at an industrial-scale thermal plant is structurally different from operators plugging into the ENDE grid at subsidized rates. It survives the gas subsidy unwind because it has negotiated direct access to a specific plant rather than depending on the national tariff. Second, Alps' local partner through the Parak entity has direct relationships with the new government, including a connection to Bolivia's Ministry of Economy. When regulatory questions arise, Alps has channels that newly arriving operators will take years to build. Third, the company is positioning Bolivia as its primary growth market globally, not a secondary deployment. Bolivia is Alps' number one strategic priority for 2026, with capital and senior management attention to match.

"Our vision is more global than most operators. We invested in the US to show we can operate there for institutional investors, but our capital and strategic focus are going to Bolivia. Bolivia is the market where we can genuinely help solve an economic problem and build something that lasts beyond the first hashprice cycle. If other markets, like Venezuela, were to open up we could consider it, as it has similarities with Bolivia’s currency crisis, and vast energy resources."

— Francesco Buffa, CEO, Alps

The Logistical Reality: Customs and the Landlocked Challenge

Operating in Bolivia is not straightforward, and Alps has been candid about the friction. Bolivia is landlocked. ASIC shipments follow the same bimodal route used for industrial equipment more broadly: ocean freight to an Argentine or Brazilian Atlantic port, then the Paraguay-Parana waterway to Puerto Jennefer, then overland to Cochabamba or other deployment sites. The same route was used to deliver 30 Vestas 3.6 MW wind turbines to the Santa Cruz parks, proving the logistics chain works for oversized industrial cargo.

On customs, Bolivia's new government eliminated import taxes on ASICs, a significant policy shift. But a 15% VAT remains, and crucially, it is non-recoverable. On a shipment of machines at scale, that 15% is a real cost that cannot be optimized away. Alps has flagged customs processing time as a genuine operational pain point. For operators accustomed to simpler import environments, the bureaucratic complexity of Bolivian customs is a barrier that experience and local relationships help navigate but cannot eliminate.

The Market Context: Who Else Is Mining in Bolivia

Beyond Alps, Bolivia's mining market is largely composed of smaller operators who arrived during the subsidized gas window and whose durability through the coming tariff adjustment is uncertain. The +2,400% YoY spike reflects a large number of relatively small operations capturing the spread, not a handful of institutional players building permanent infrastructure.

The bifurcation that occurred in Paraguay between 2022 and 2024, when tariff increases and deposit requirements separated institutional operators from arbitrageurs, has not yet happened in Bolivia. It will. When Bolivia's gas subsidy begins to reflect more realistic costs, operators without direct access to stranded assets or durable renewable sources will face the same margin compression that squeezed mid-tier operators out of Paraguay. The operators who survive that transition will be the ones who did what Alps did: build direct relationships with energy asset owners and negotiate USD-denominated auto-consumption arrangements that are insulated from the national tariff trajectory.

The Durable Opportunity: Beyond Thermal

For miners willing to look beyond the immediate gas window, Bolivia has durable energy assets that can support long-term operations at competitive costs. COBEE's Sistema Zongo cascade generates 188 MW of hydroelectric power at near-zero marginal cost from infrastructure that has operated since the 1930s. Long-term PPAs with COBEE represent one of the most structurally sound mining energy arrangements available in South America outside of Paraguay.

The Uyuni solar resource, despite the altitude engineering challenges (IP54-rated equipment, 90-100% inverter derating, specialized thermal management), offers exceptional irradiation. As battery storage policy develops and the grid integrates storage at scale, the altiplano solar resource becomes viable for continuous mining operations. The Laguna Colorada geothermal pilot (5 MW today, 100 MW target) represents the most reliable long-term baseload source in the country: 24/7 availability, zero fuel price exposure, and leverage over a volcanic resource that Bolivia is uniquely positioned to exploit.

The Regulatory Environment: A New Government, A New Opening

Bolivia's political shift toward a right-leaning government has materially changed the conditions for private capital in the energy sector. The previous government's approach to foreign investment in energy was characterized by state dominance and resistance to market-based pricing. The new administration is actively seeking foreign capital to address Bolivia's dollar-liquidity crisis and has demonstrated this through concrete actions: eliminating import taxes on ASICs, establishing the autoconsumption legal framework that Alps is using at Cochabamba, and opening direct dialogue with foreign operators.

Alps' Bolivia partner becoming a key minister is emblematic of the relationship-driven nature of this market. Bolivia does not yet have the established regulatory framework for industrial Bitcoin mining that Paraguay built through the GCIE tariff category. The rules are being written in real time, and operators who are in the market now, working directly with government counterparts, are shaping those rules in ways that later entrants will not be able to influence.

The risk, as Francesco has noted explicitly, is that Bolivia attracts operators who are not serious, creating the political backlash that led Paraguay to implement tariff hikes and deposit requirements. The most important thing Alps can do for Bolivia's long-term mining market, beyond its own commercial interest, is demonstrate that industrial-scale operators who bring genuine dollar investment, employ local staff, and build real infrastructure are the model the government should encourage.

The Bottom Line

Bolivia's 2,400% hashrate spike was arbitrage. Bolivia's mining opportunity is not.

The country has stranded industrial energy assets, a government that needs USD inflows, a regulatory environment that is actively opening to foreign capital, and at least one operator who arrived with the right model, Alps, rather than just the right timing.

The structural risks are real. Gas depletion is not a hypothetical. The boliviano distortion that made the Cochabamba thermal plant idle is a symptom of deeper fiscal problems that will not resolve quickly. Customs friction is a daily operational reality. And the absence of a clear long-term regulatory framework for industrial mining means that the rules governing billion-dollar capital deployments are still being written.

But the opportunity that Alps identified is genuine. A 127 MW thermal plant that cannot be operated commercially under Bolivia's monetary distortions becomes a Bitcoin mining facility that solves the plant operator's dollar problem, generates hard currency for the country, and provides electricity to mining operations at a cost structure that survives the national gas subsidy unwind. That is a different kind of mining thesis from what drove the 2,400% spike, and it is the kind that builds real hashrate.

Paraguay did not become the #4 Bitcoin mining country in the world by accident. It happened because a structural energy surplus, a government willing to create a legal framework for industrial consumption, and serious institutional capital arrived at the same time. Bolivia has two of those three conditions in place. The third is being built now, largely because Alps is there building it.

— Happy Hashing!

About Luxor Technology Corporation

Luxor delivers hardware, software, and financial services that power the global compute and energy industry. Its product suite spans Bitcoin Mining Pools, ASIC Firmware, Hardware trading, Hashrate Derivatives, Energy services, a Miner Management software, Commander, and a bitcoin mining data platform, Hashrate Index.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

){kind=link}