Luxor Hashrate Lookback Series – May 2026

May 2026’s hashrate and hashprice trends, forward market participation, trading activity and contract performance.

Luxor’s Monthly Lookback Series is a deep dive into Bitcoin hashrate market activity. In this post, we cover May 2026’s hashrate market and hashprice trends, forward market participation, trading activity and contract performance.

Summary

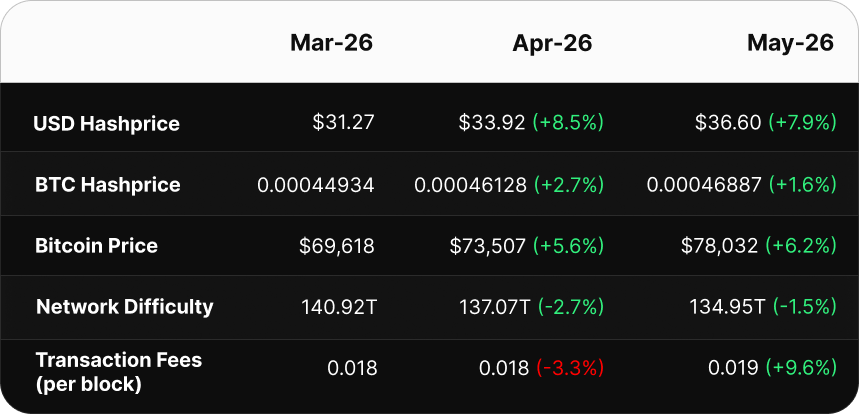

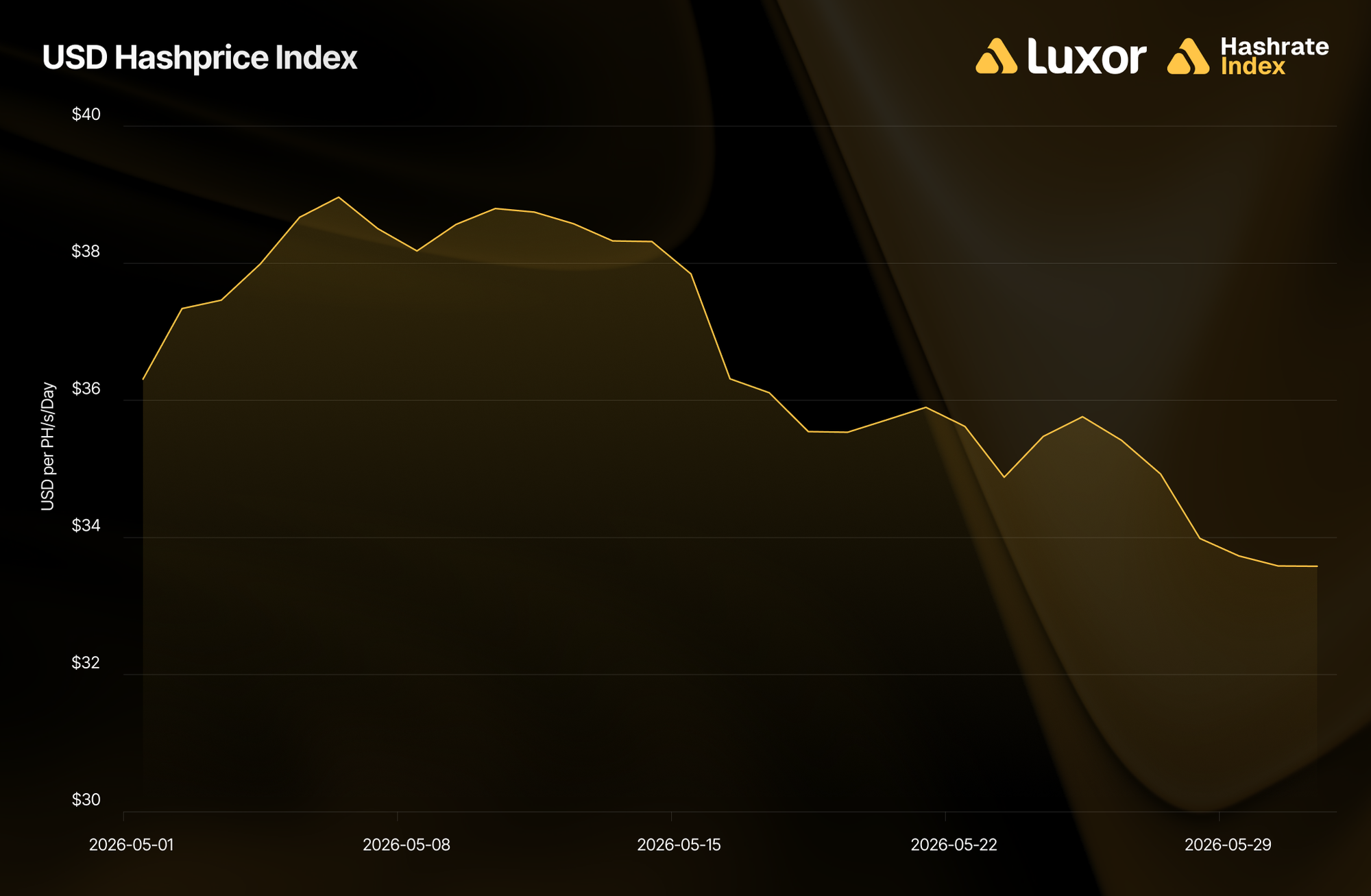

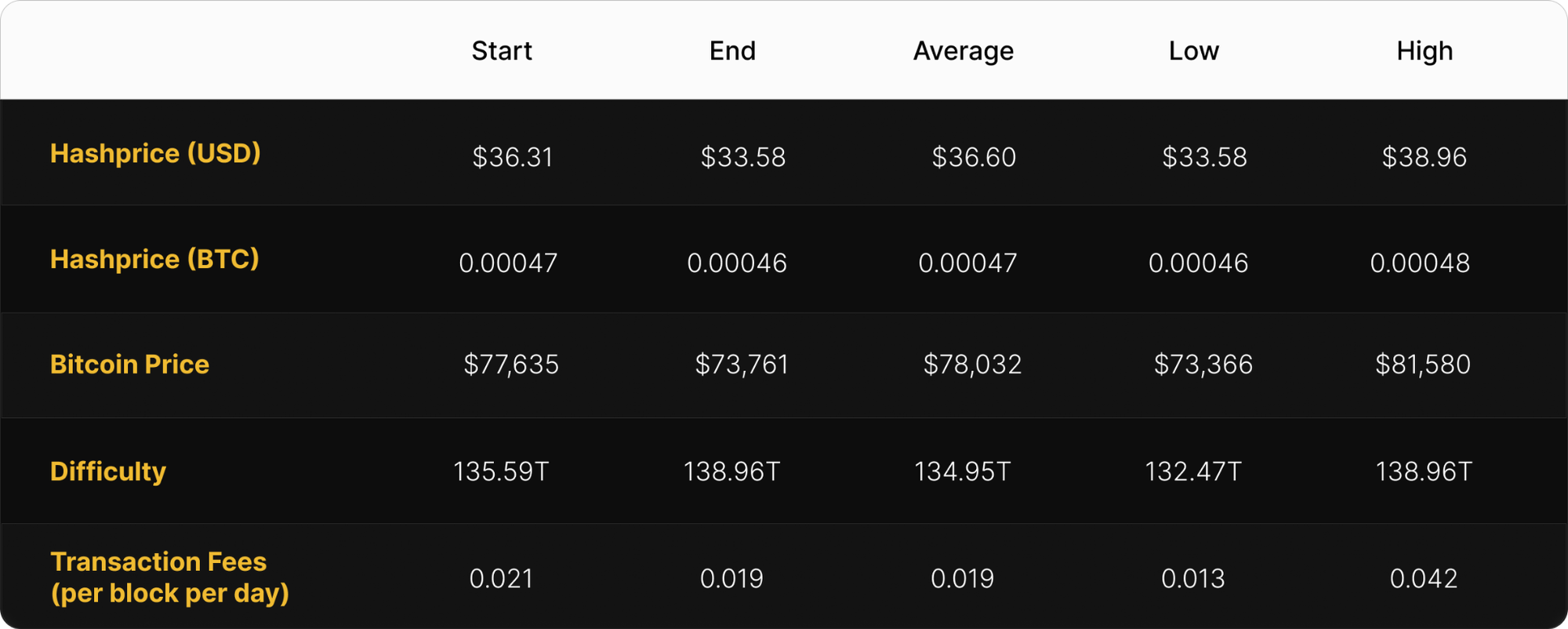

- High-Then-Fade in Mining Economics: USD hashprice and BTC both rallied through early May, peaked on May 6, then faded to close the month at their lows. The monthly average still landed higher — USD hashprice at $36.60 per PH/s/day (+7.9%) — but the trend had reversed well before month-end.

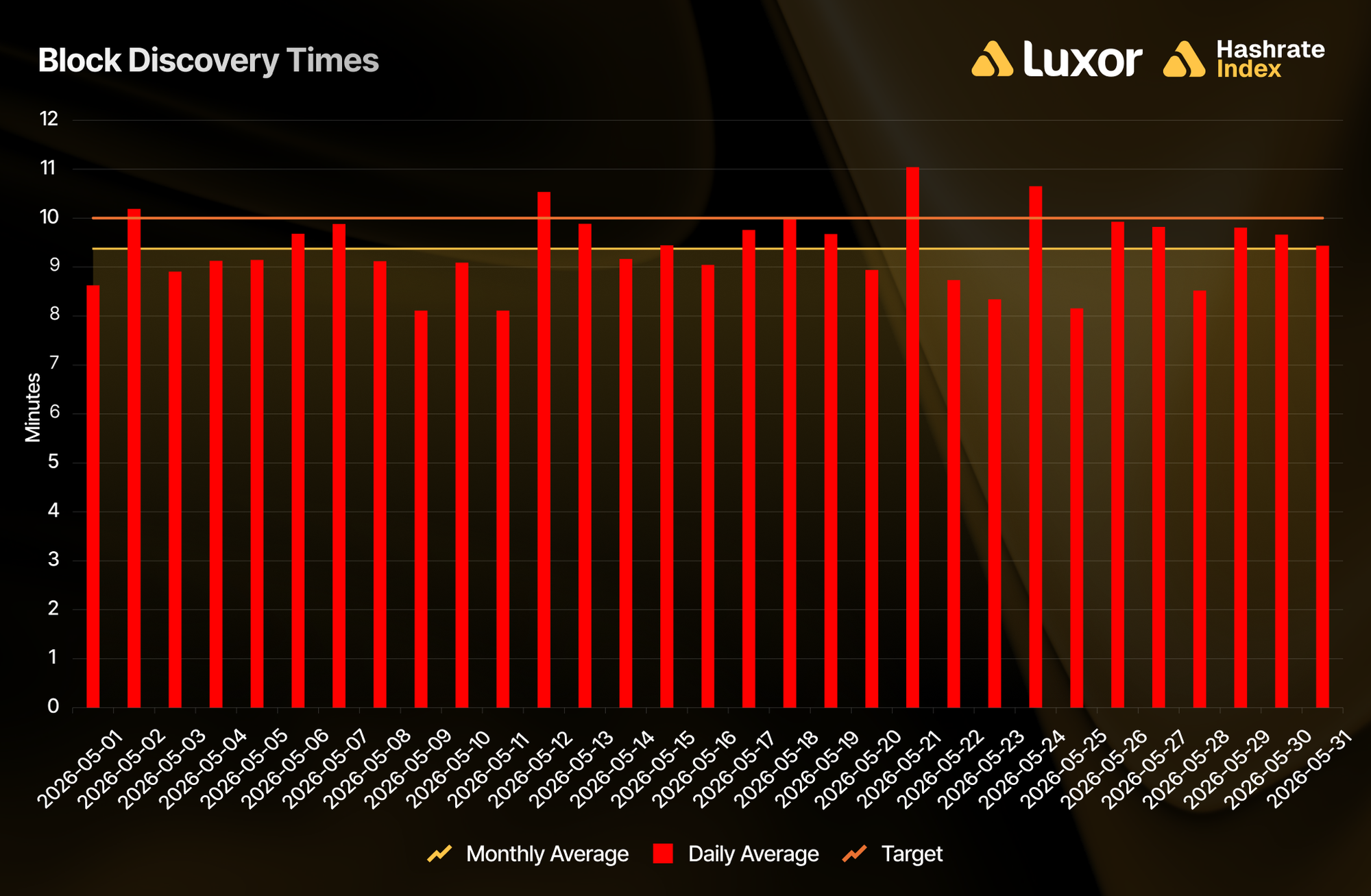

- Difficulty Averaged Lower but Netted Higher: Three adjustments — down on May 1, up on May 15 and May 29 — left difficulty 2.5% higher start-to-finish, even as the monthly average slipped 1.5% to 134.95T. Block times stayed fast, averaging 9m22s with 27 of 31 days under the 10-minute target.

- USD Hedging Split, One Winner: Of the May 2026 USD contract, only the four-month-ahead sellers in January beat spot (FPPS) mining, locking in $37.99 (+3.8%) versus $36.60. Every other hedge horizon settled below spot as USD hashprice faded into the month-end.

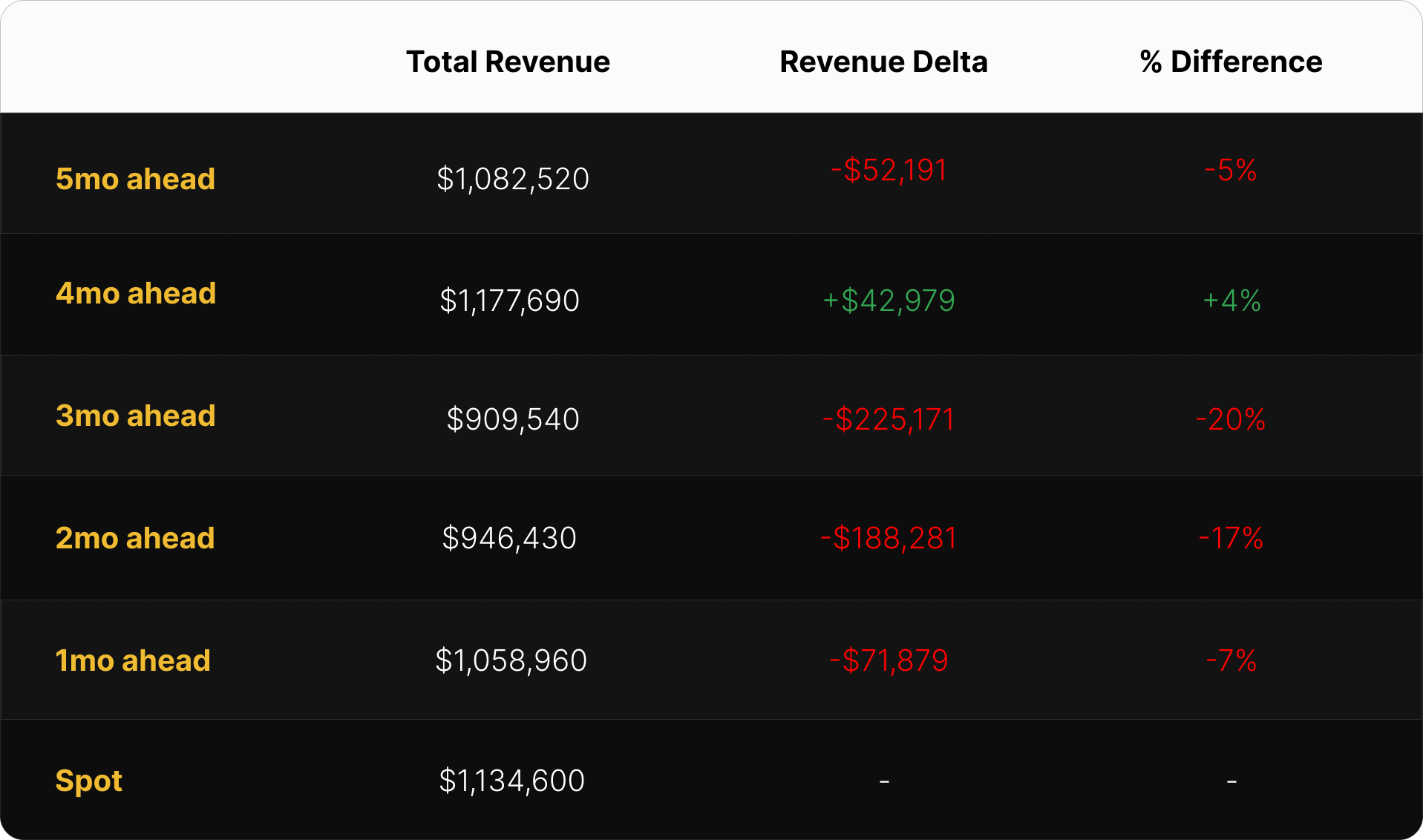

- BTC Buyers Swept the Board: BTC-denominated buyers outperformed across the board for the May 2026 contract, with sellers giving up 1.6% (1-month) to 19.0% (5-month) versus spot settlement at 0.00047 BTC per PH/s/day. Difficulty contracting on a monthly-average basis kept BTC hashprice settling above forward lock-in rates.

- Forward Curve Flips to Contango: as of early June, the forward curve has flipped into contango: June and July contracts are trading near ~$30, a premium of over 6% over current spot hashprice at ~$27-28. The forward market is pricing a near-term difficulty pullback as summer 4CP curtailment season begins.

May 2026 Spot Hashprice & Its Constituents

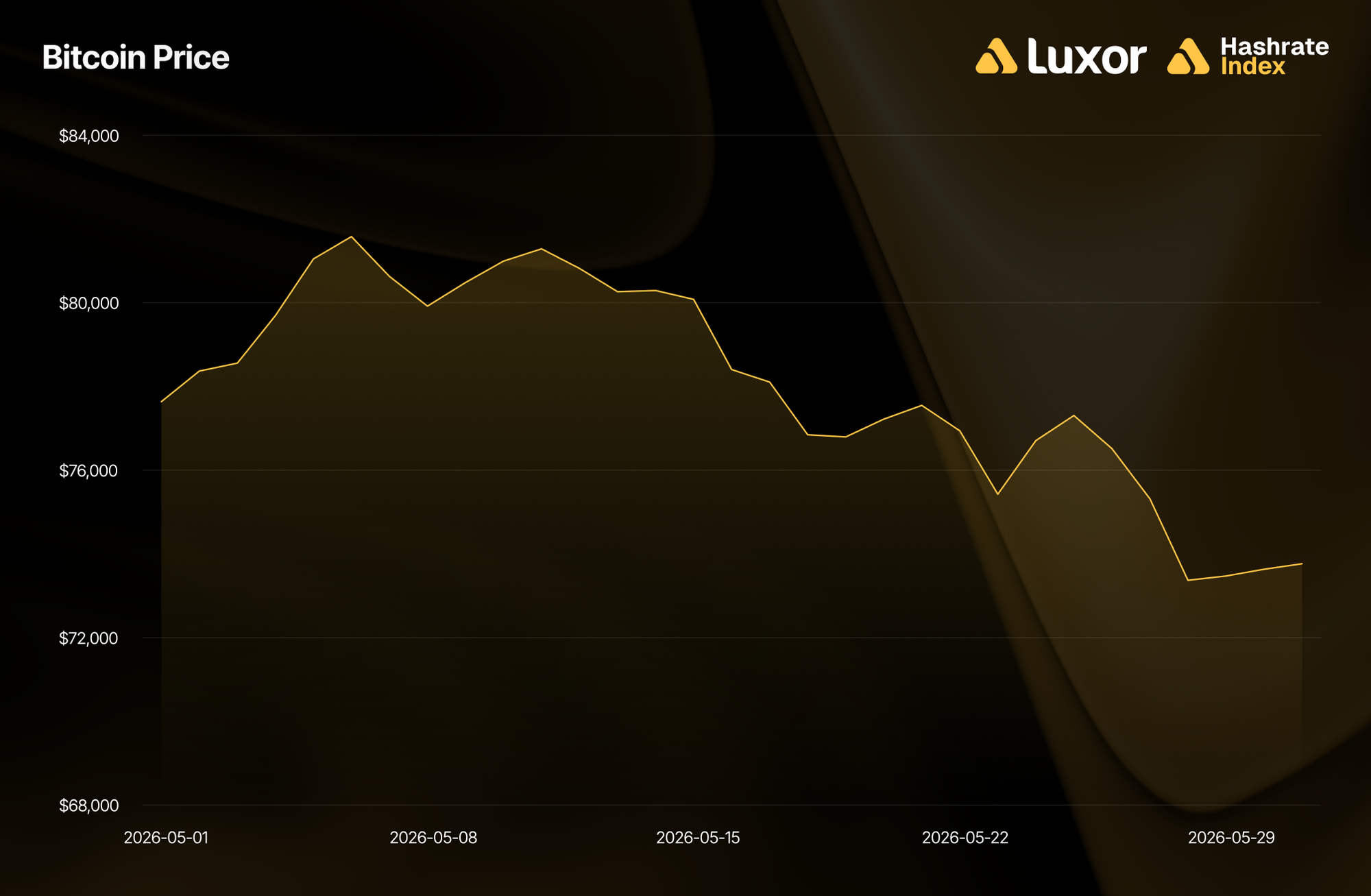

May 2026 was a high-then-fade month for Bitcoin mining markets. USD hashprice and BTC price both rose on a monthly-average basis, peaking on May 6, but weakened into the close. Difficulty told the opposite story: down on average, but net higher from the first epoch to the last.

USD Hashprice — Rose on Average, Faded into the Close

Monthly average USD hashprice rose 7.9%, from $33.92 to $36.60 per PH/s/day, a second straight monthly increase off the February–March all-time-low period.

The average understates how the month trended. Hashprice opened May at $36.31, climbed to a monthly local peak of $38.96 on May 6, then reversed course to close at $33.58, the month’s local low. The close came in below the open, though well above February 24’s daily all-time low ($27.89) and March 2026’s record-low monthly average ($31.27). For context, 2025’s monthly averages ranged from $37.89 to $59.38 with a mean of ~$50.69; May 2026’s $38.96 peak remained at the low end of last year’s range.

BTC Price — Same Arc Under a Persistent Macro Shock

BTC averaged $78,032 in May, up 6.2% from April. It opened at $77,635, peaked at $81,580 on May 6, slid to a $73,366 low on May 28, and closed at $73,761. After leading the February drawdown and re-coupling with risk assets through April’s equity rally, BTC spent May losing the front half of its monthly gain.

The macro backdrop is the continuation of conflict in the Middle East, which began February 28 when U.S. and Israeli strikes hit Iranian targets and Iran responded by closing the Strait of Hormuz, where roughly 25% of the world's seaborne oil and 20% of its LNG travel through.

The mining-relevant detail is geographic. Per Hashrate Index's Oil Shocks and the Bitcoin Network analysis, the direct link between crude prices and mining cost is weak for ~90% of global hashrate, which runs on U.S., Canadian, Russian, Chinese, and hydro-dependent grids where power pricing is largely decoupled from crude. Only Gulf-state operators (UAE, Oman, and Iran, an estimated 8–10% of hashrate) are directly exposed, and Iran's ~7 EH/s had already dropped offline earlier in Q1. With network hashrate back near 1 ZH/s (~995 EH/s) by month-end, that loss has been offset elsewhere by new-generation deployment and marginal miners returning as economics improved. The crisis continues to be a macro overhang on BTC price, but not a supply shock to grid-tied hashrate.

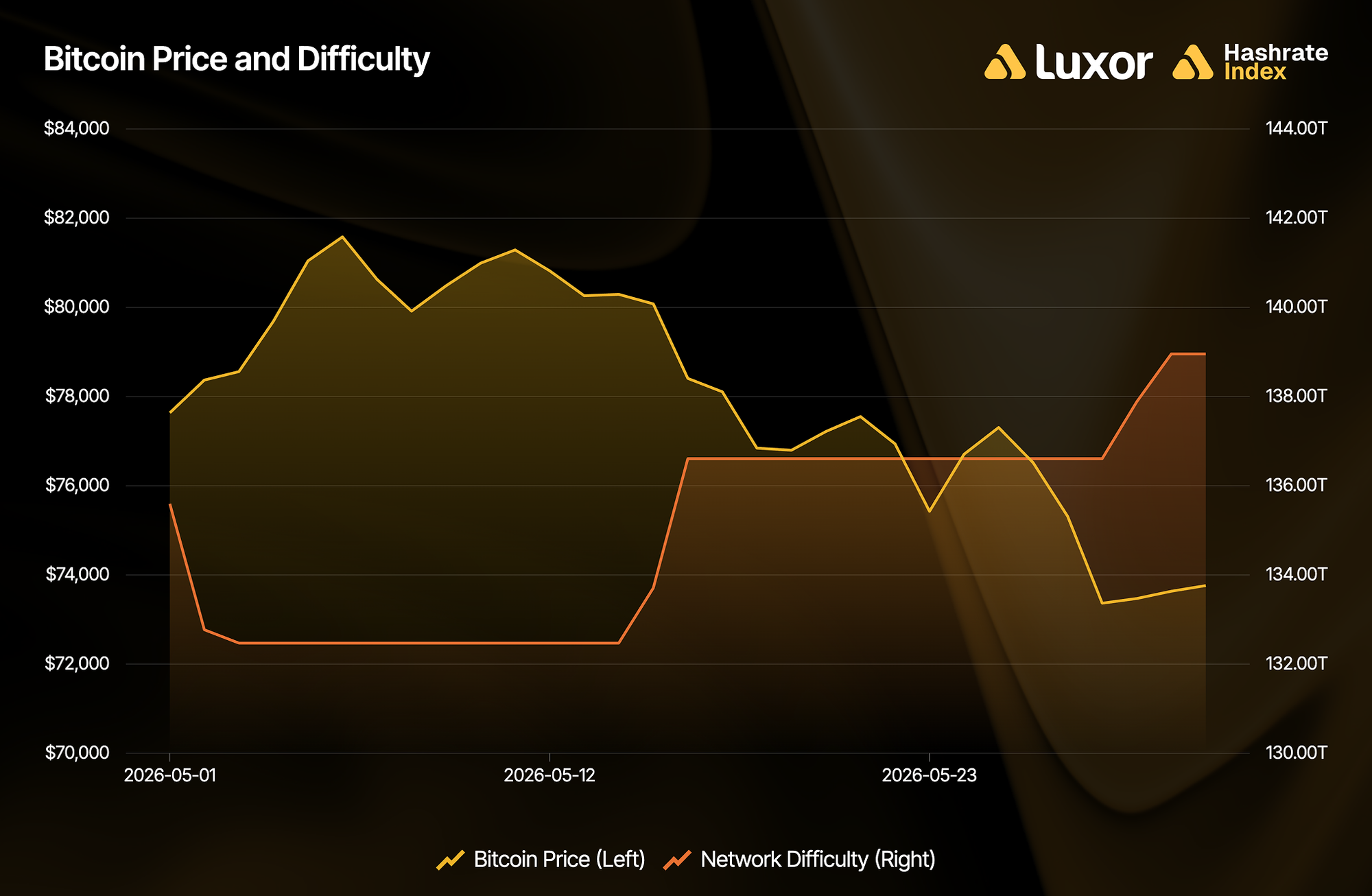

Network Difficulty — Averaged Lower, Netted Higher

Difficulty averaged 134.95T in May, down 1.5% from April. Three adjustments landed during the month. The May 1 epoch dropped difficulty by -2.30%. The May 15 epoch reversed course, +3.12% to 136.61T (~978 EH/s), and the May 29 epoch adjusted +1.72% up to 138.96T (~995 EH/s). The net effect was a +2.5% climb from the start of the month to the end, even though the monthly average came in below April 2026.

Blocks ran fast: the network averaged 9 minutes 22 seconds per block, with 27 of 31 days below the 10-minute target. The cause was marginal hashrate recovery off early-May strength. Hashrate returned as economics improved through mid-month, then difficulty rose into a fading hashprice and squeezed margins tighter again by month-end.

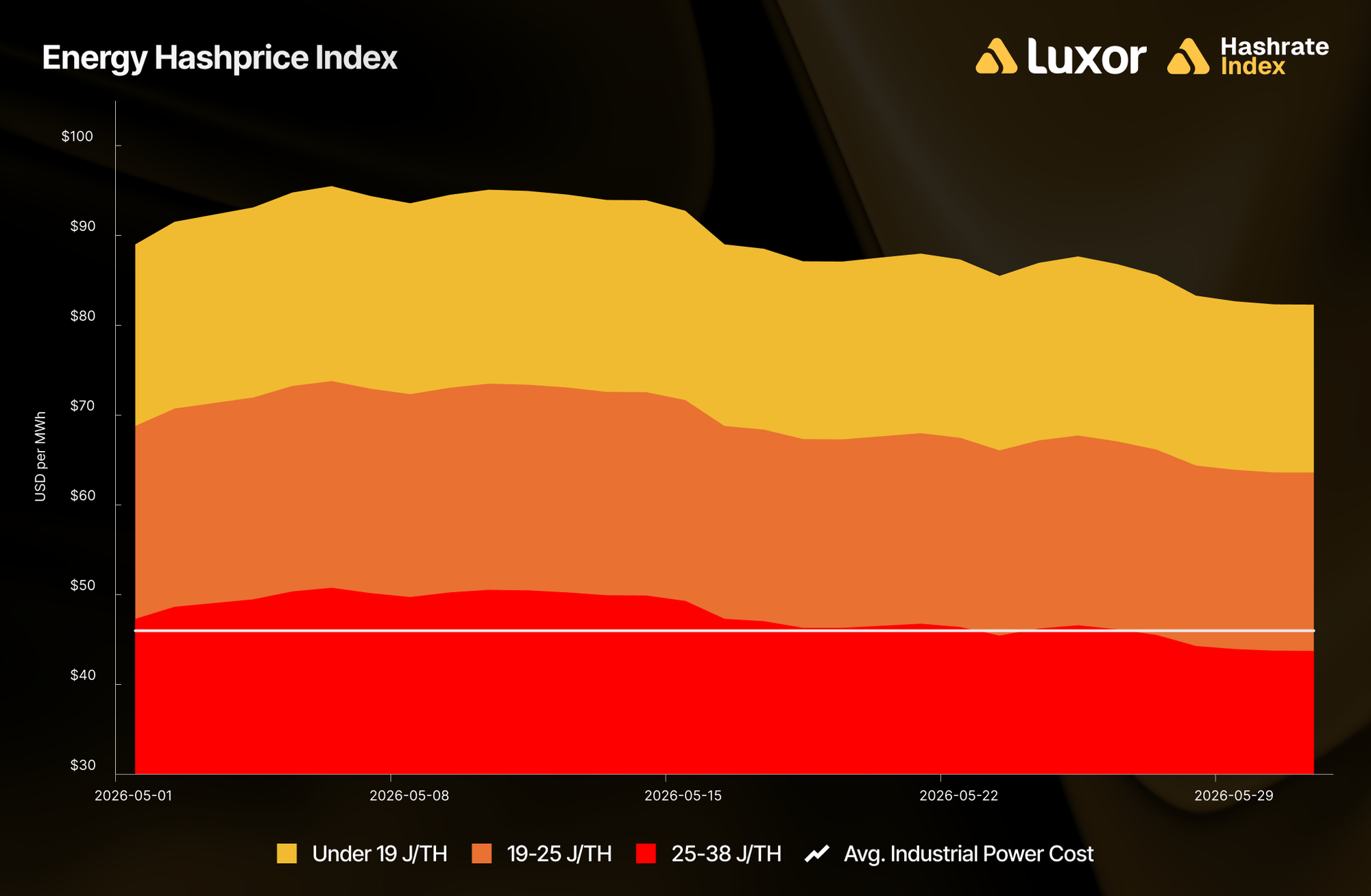

Mining revenue per unit of electricity consumed improved across fleets. Implied energy hashprice averaged ~$90/MWh for fleets under 19 J/TH, ~$69/MWh for 19–25 J/TH fleets, and ~$48/MWh for 25–38 J/TH fleets. Against an estimated network-average power cost of ~$46/MWh, the 25–38 J/TH tier just broke even on average, a step up from Q1’s deep deficit.

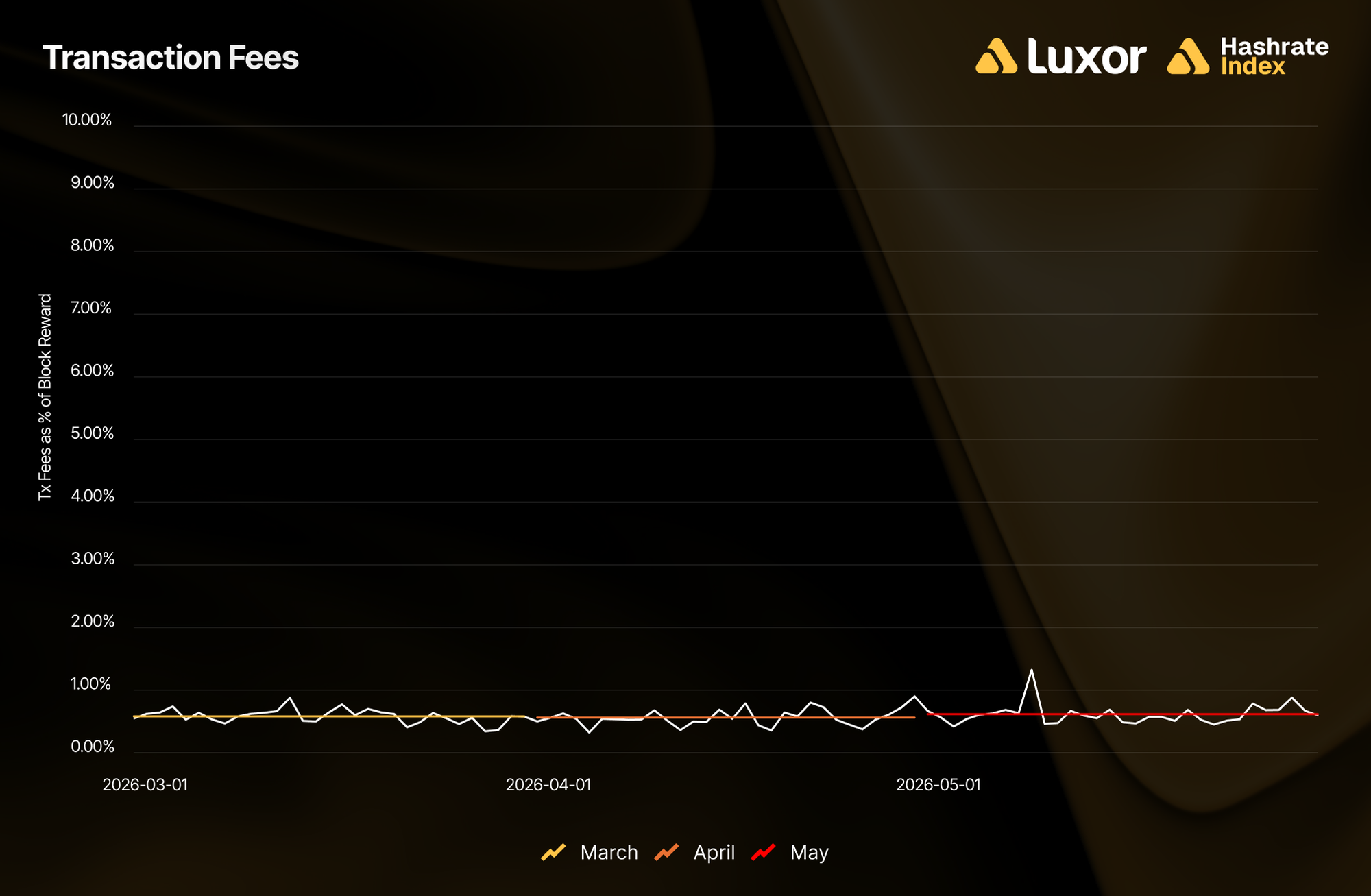

Transaction Fees — Up Modestly

Average fee collection rose 9.6% to 0.01941 BTC per block in May, from 0.01771 in April — a modest uptick in an otherwise dry fee environment. Fees accounted for approximately 0.62% of total block rewards, still under 1% as they have been since July 2025. In USD terms, average fee revenue per block was approximately $1,514 (+16.0%) versus April at $1,306.

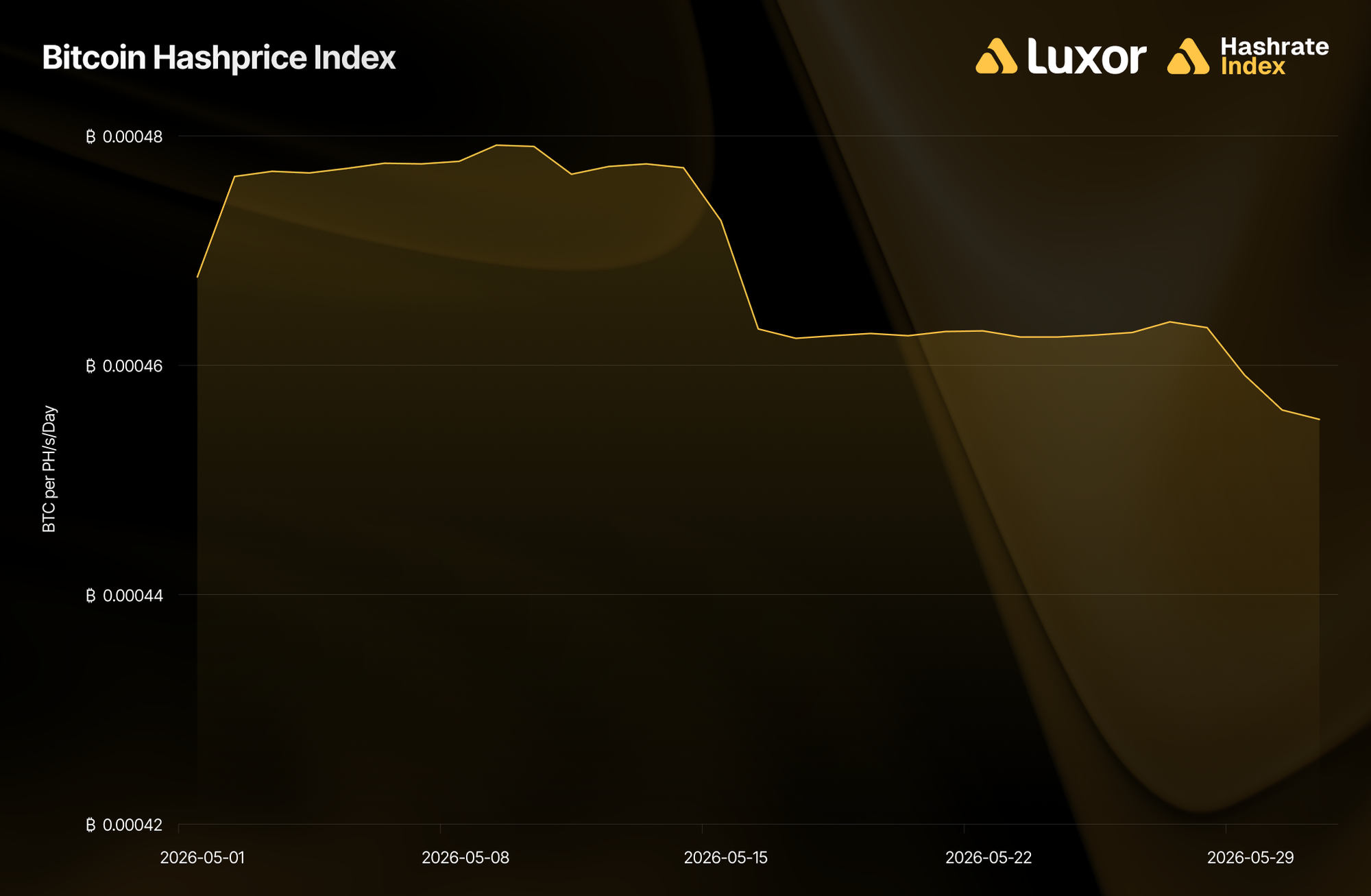

BTC Hashprice — Up With Difficulty Relief and Higher Fees

Monthly average BTC hashprice rose 1.6%, from 0.00046128 to 0.00046887 BTC per PH/s/day. The move came from its two constituents: a lower average difficulty (-1.5%) and the rise in transaction fees (+9.6%), which together lifted BTC rewards per unit of hashrate. Intra-month, BTC hashprice opened at 0.000468, climbed to a monthly high of 0.000479 on May 9–10 (as difficulty held at its 132.47T floor), then declined to close at 0.000455 (the monthly low) as the May 15 and May 29 epochs lifted difficulty back toward ~1 ZH/s.

May 2026 Hashrate Market Activity

Our analysis of the May 2026 hashrate market focuses on two key points: how the May 2026 hashrate contract traded in previous months and how the forward curve shifted in May, based on pricing for forward hashrate during the month.

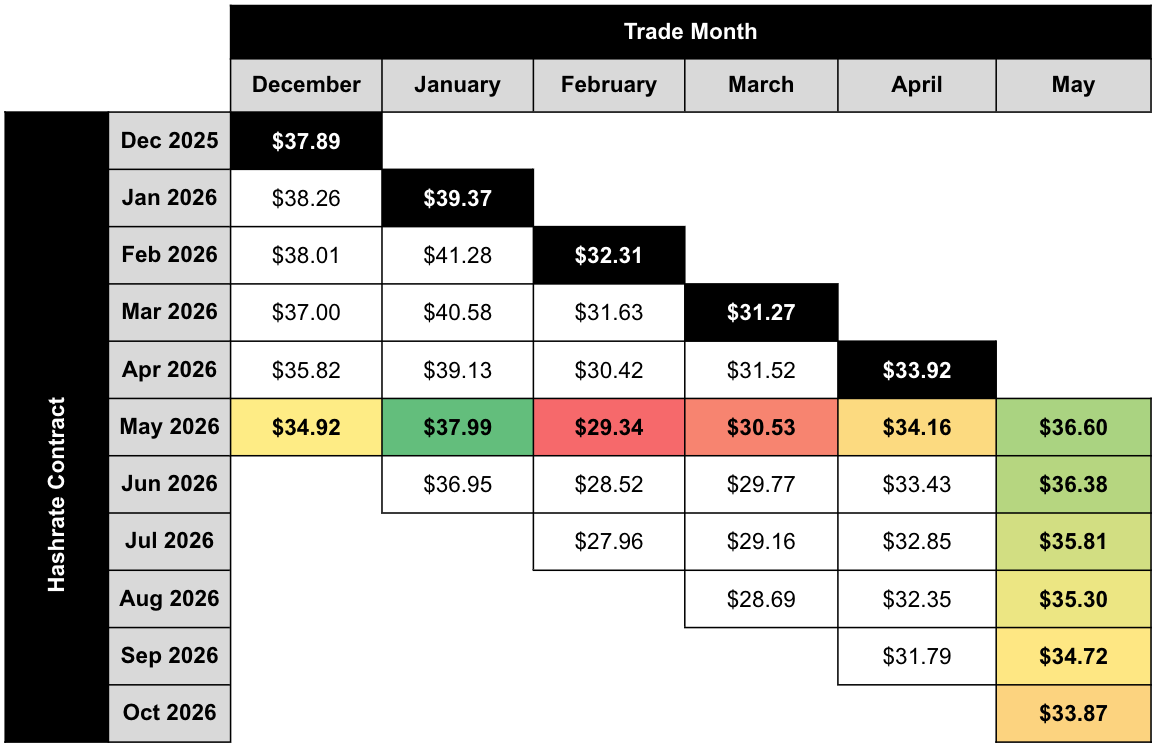

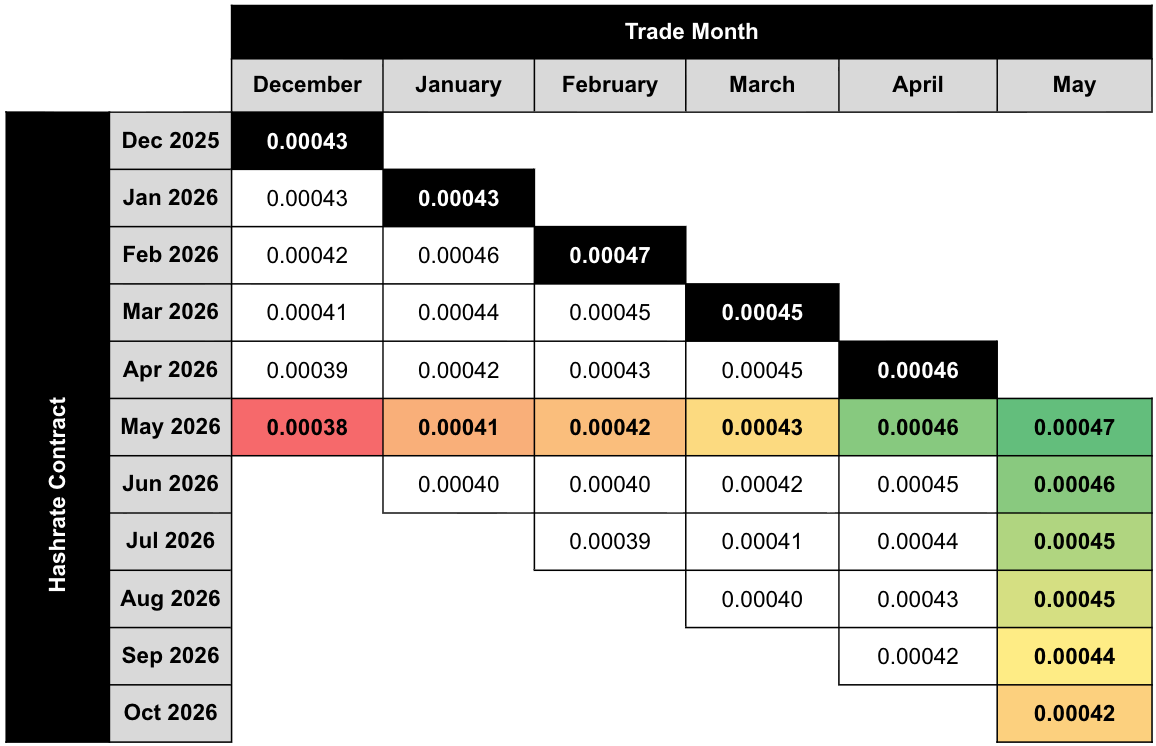

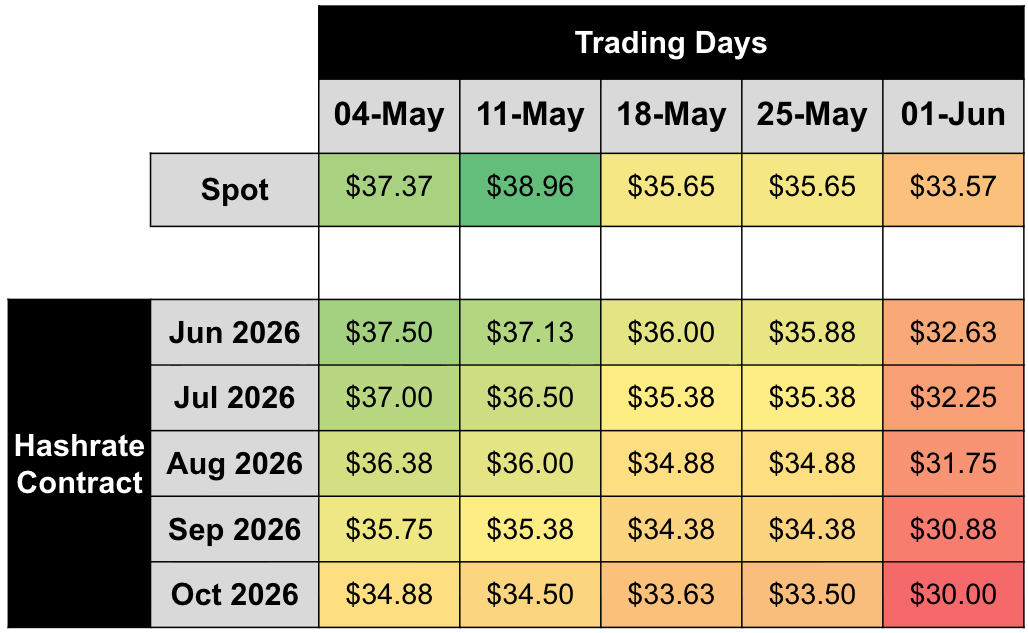

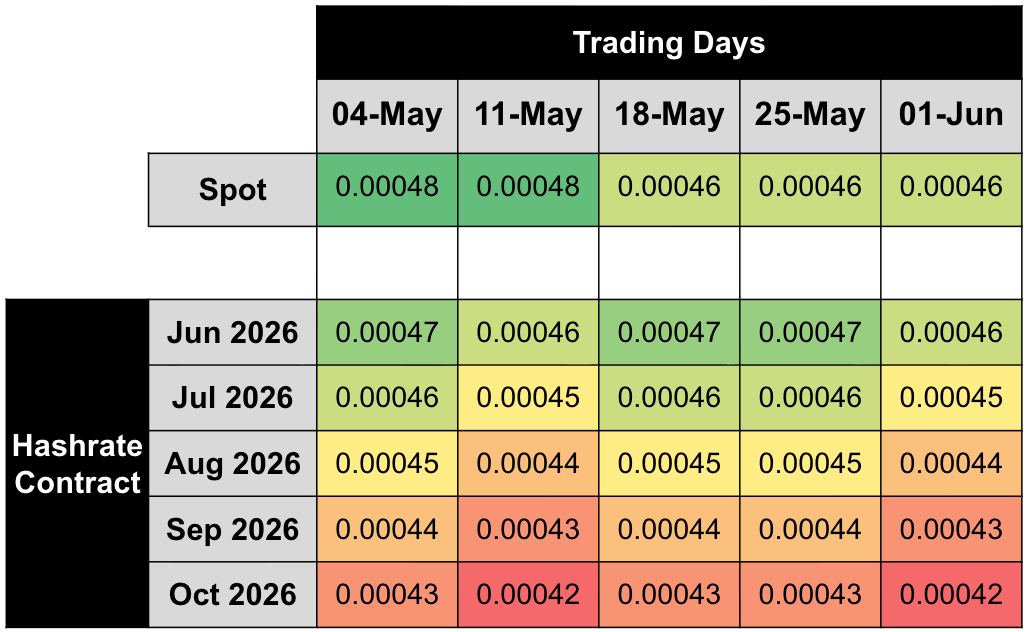

The two tables below show the evolution of Luxor’s USD and BTC-denominated hashrate forward markets from December 2025–May 2026. Rows represent specific monthly contracts, while columns represent each trading month. Cell values indicate the average monthly mid-market hashprice — except for the bold highlighted main diagonal — which shows actual spot hashprice settlement in each month.

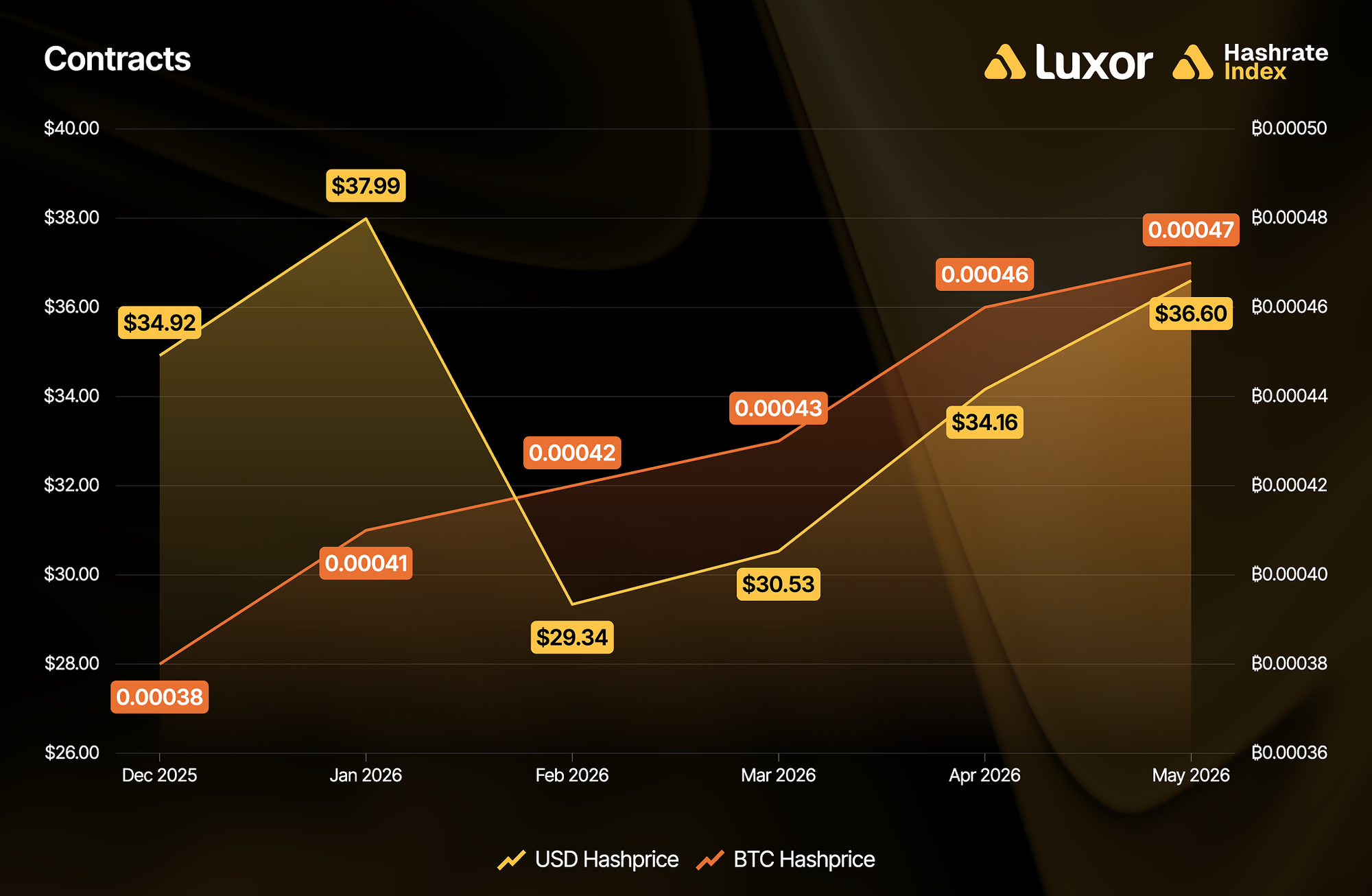

This table summarizes both the trading history of the May 2026 USD-denominated contract (colored row) and the forward curve in May (colored column).

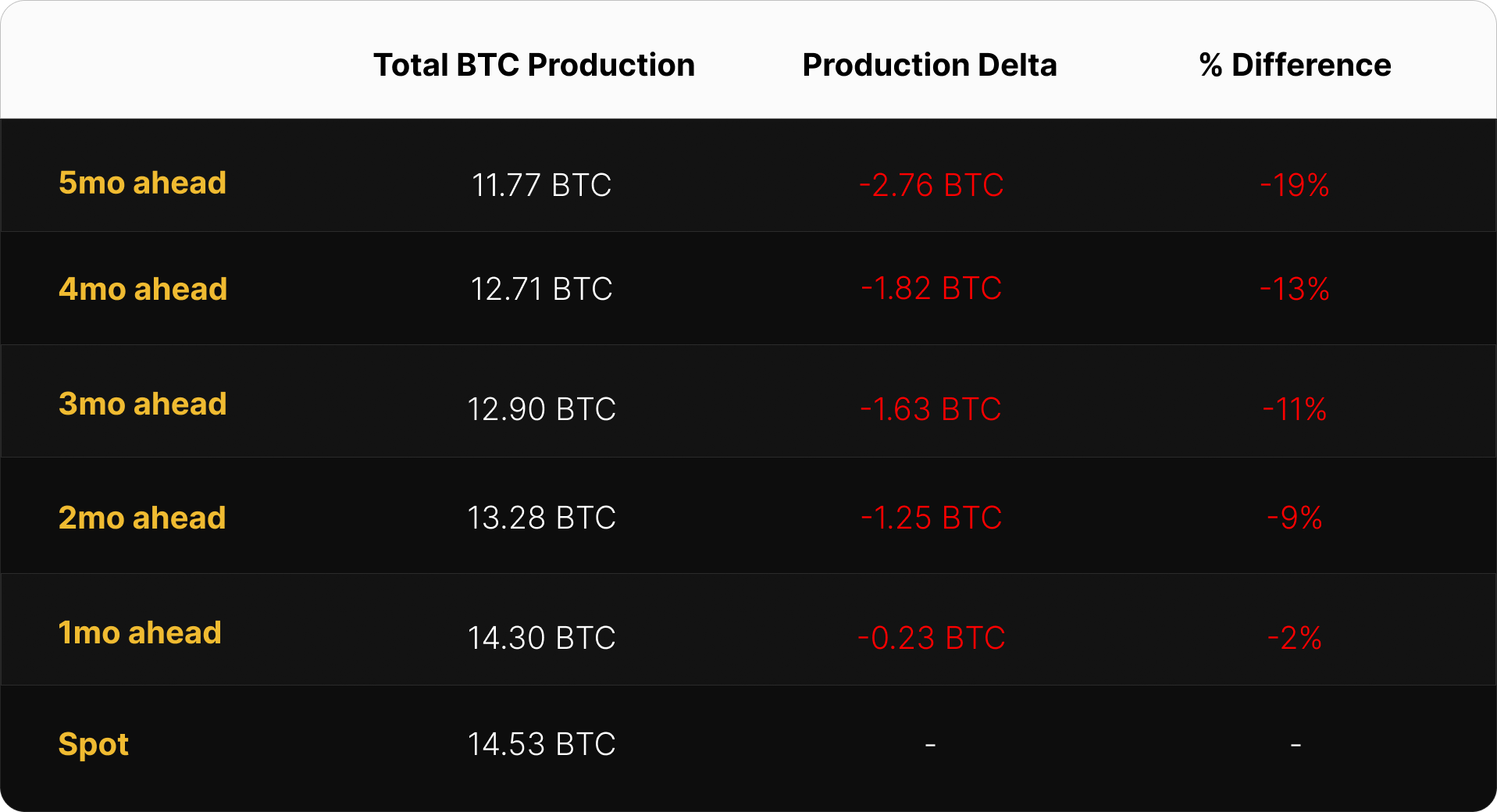

This table summarizes both the trading history of the May 2026 BTC-denominated contract (colored row) and the forward curve in May (colored column).

Note: all values (except for the bold highlighted main diagonal) shown in figures represent mid-market rates, the midpoint of the best bid and ask on Luxor's Non-Deliverable Hashrate Forward market. The bold highlighted main diagonal shows actual spot hashprice settlement in each month, measured by Luxor’s Bitcoin Hashprice Index.

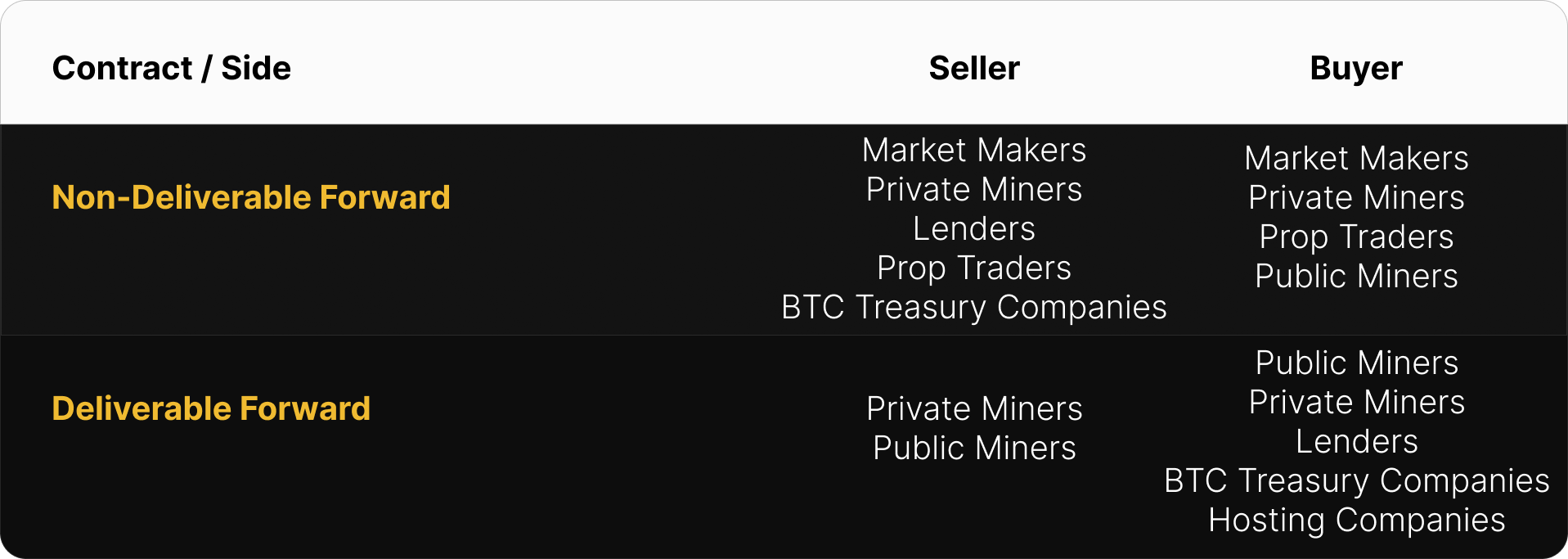

The table below shows the type of market participants on the buy and sell side of Luxor’s deliverable (DF) and non-deliverable hashrate forward (NDF) market. In May, lenders were active on the buy side of the DF market, while public and private miners used the contract to sell forward, receive financing, and expand their fleet.

Since the DF involves upfront payment, it tends to trade at a discount to the NDF, compensating the buyer for the inherent credit risk. We interpret the discount of DFs relative to NDFs as the interest rate in hashrate-based lending markets. Buyers and sellers of the DF with upfront payment can use the NDF to lock-in a fixed yield (cost of capital) instead of having exposure to hashprice uncertainty.

This strategy was used by lenders and Bitcoin treasury companies (buy DF & sell NDF) to earn a BTC-denominated return and by miners (sell DF & buy NDF) to obtain non-dilutive financing. In May 2026, that yield (cost of capital) was 6–13% annualized.

How May 2026 Hashrate Traded

May delivered split results in hashrate hedging, driven by two distinct forces.

In USD-denominated contracts, only one hedge horizon beat spot. Forward sellers of the May 2026 contract locked in between $29.34 and $37.99 per PH/s/day against spot settlement of $36.60. The single winner was the four-month-ahead sale set in January 2026 at $37.99 (+3.8%) — priced while BTC was still trading above $90,000. Every other tenor settled below spot hashprice as early-May BTC price strength arrived and then reversed.

In BTC-denominated contracts, buyers won across the board. Forward sellers received between 0.00038 and 0.00046 BTC per PH/s/day, all below spot settlement of 0.00047. Network difficulty contracting off its Q4 2025 peak (down ~12% from a 153T monthly average in November 2025 to 134.95T in May 2026) kept BTC hashprice settling above forward lock-in rates. This spread compressed sharply at the front of the curve: 5-month BTC sellers (locked in December 2025) gave up 19% versus spot, while 1-month sellers (locked in April 2026) gave up just 2%.

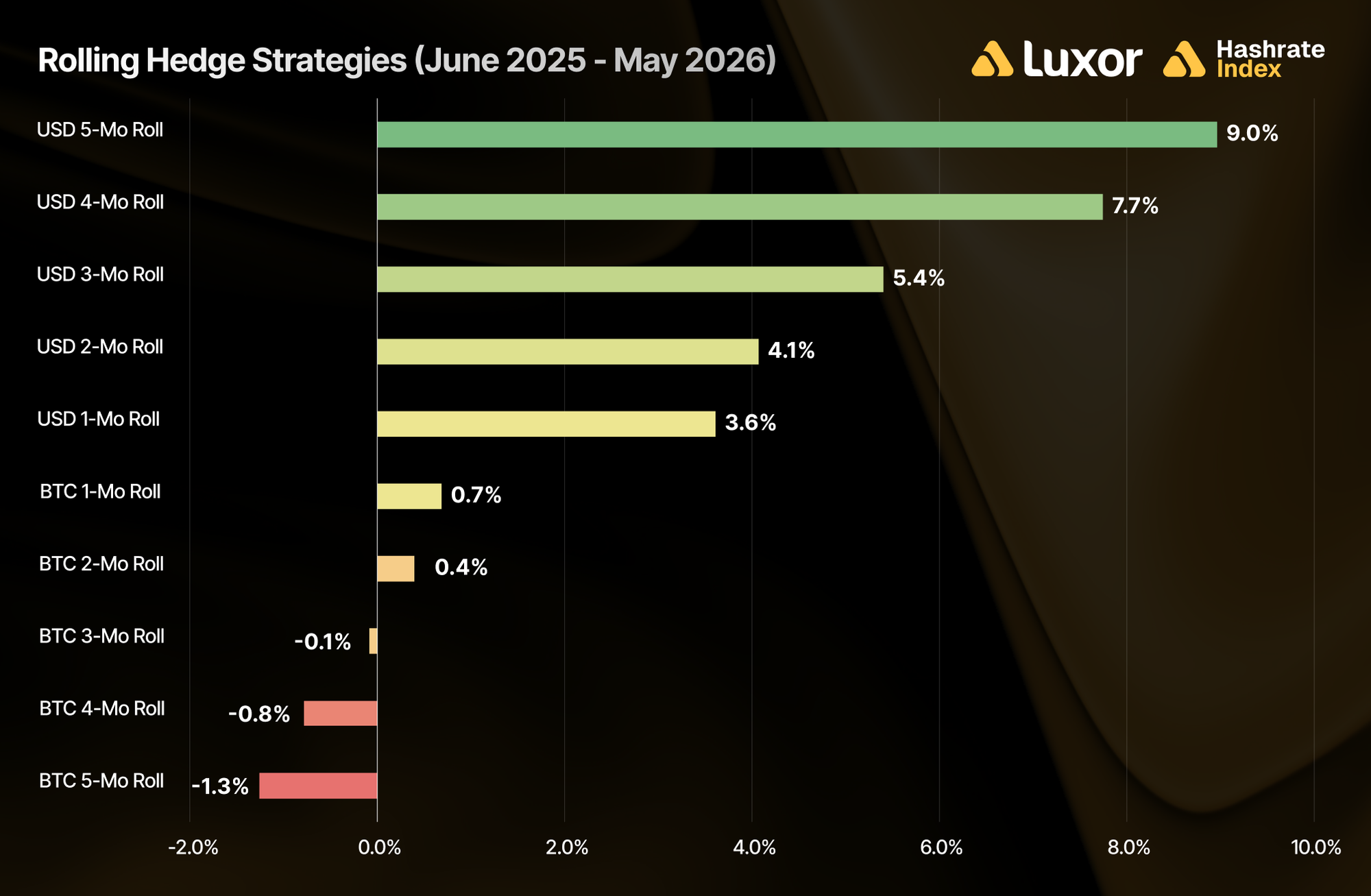

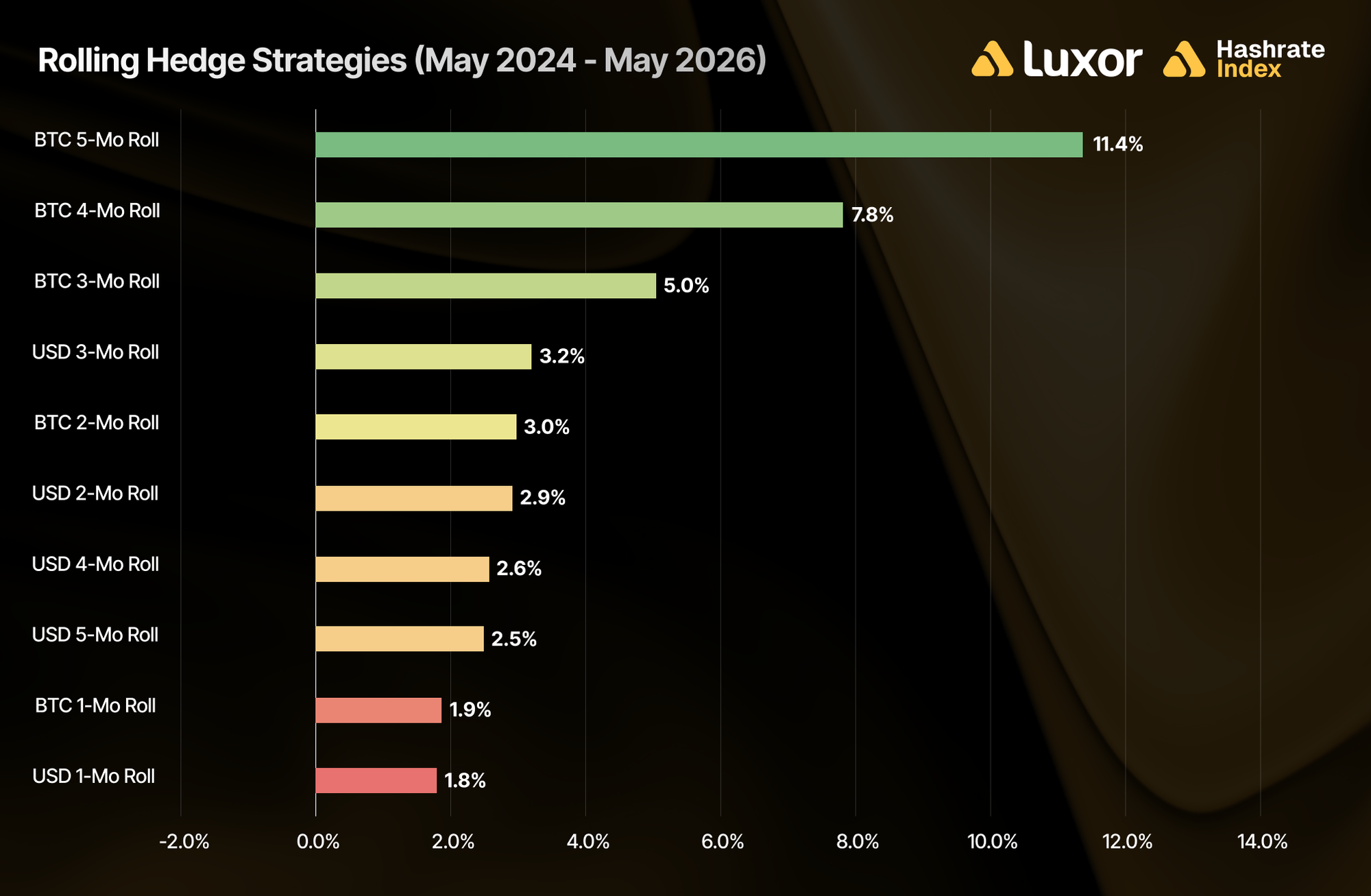

Zooming out, we examine rolling hedge performance across two windows: the trailing twelve months (June 2025–May 2026) and since the April 2024 halving (May 2024–May 2026).

Over the past year, rolling USD-denominated hedging strategies outperformed spot mining across every horizon. The strongest results came from the 5-month (+9.0%) and 4-month (+7.7%) USD rolls, which benefited from locking in hashprice ahead of declining BTC price conditions defining early 2026. BTC-denominated rolling hedge strategies clustered near flat (−1.3% to +0.7%) with 3-month to 5-month BTC rolls turning negative — a marked change from the post-halving period, when rolling BTC hedges dominated.

Extending the window back to the 2024 halving still favors BTC-denominated strategies, though the spread continues to narrow. BTC-denominated rolling hedge performance ranged roughly +5.0% to +11.4% versus spot, while USD rolls cluster around +1.8% to +2.9%. Which denomination outperforms in any window depends on whether BTC price or difficulty-plus-fees move faster and further than the forward market anticipated at the time of hedging.

From May 2024 through late 2025, network difficulty expanded faster than forward markets priced in, and BTC-denominated sellers captured the spread. From late 2025 onward, difficulty growth stalled while BTC price weakness compressed USD hashprice below forward expectations, and USD-denominated sellers captured the spread instead. The narrowing gap between the two windows reveals a regime shift: BTC-denominated hedging has lost its edge as difficulty growth stalled, while USD-denominated hedging now stands out amid volatile, uncertain BTC price action. Regardless of regime though, forward sellers have come out meaningfully ahead of operations mining at spot (FPPS) since the halving.

Note: two important caveats apply to both windows. First, figures exclude fees and bid/ask spreads. Second, hedging is a cost of business rather than a revenue generation strategy. Hedgers willingly buy the certainty of predictable cash flows, which increases valuations, reduces capital costs, and ultimately attracts investments.

How Future Hashrate Traded in May 2026

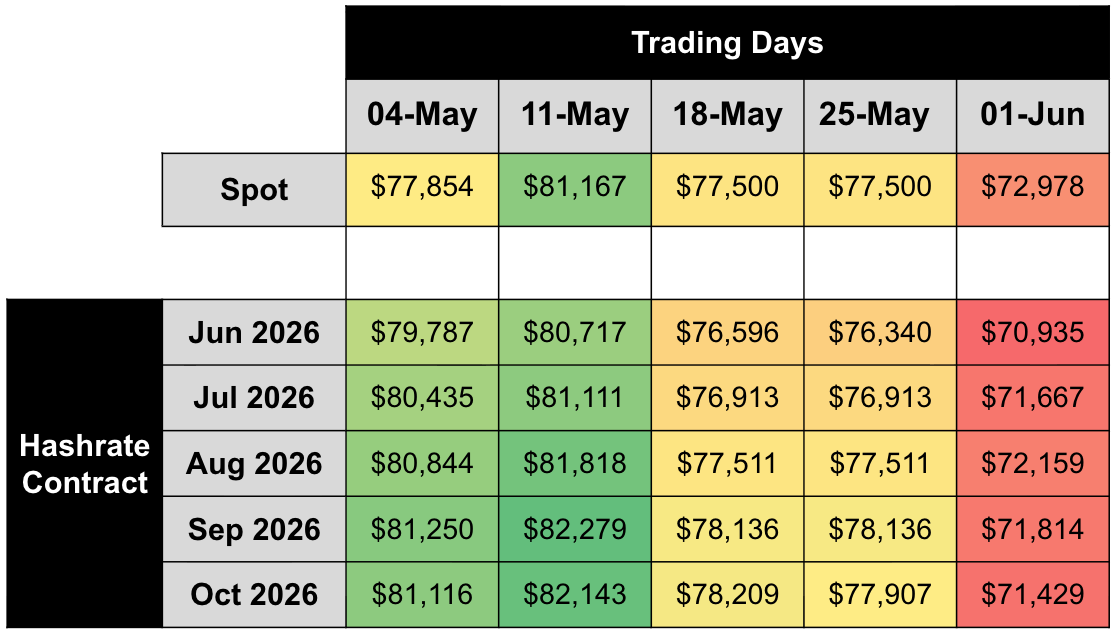

The two tables below summarize the evolution of hashrate forward markets during May 2026, for the subsequent five months from June 2026 to October 2026. Rows represent specific monthly contracts; columns represent specific trading days. Cell values are the average daily mid-market price, except for spot.

In May, the USD-denominated hashrate forward curve drifted lower as BTC price retreated from its May 6 local peak. Lock-in rates for June–October 2026 contracts fell roughly 13% between May 4 to June 1. Both curves traded predominantly in backwardation (discount to spot). The magnitude of the USD repricing was driven primarily by BTC price weakness feeding into USD hashprice expectations.

The BTC-denominated hashrate forward curve barely moved by comparison. June–October 2026 contracts’ lock-in rates slipped on average ~2% between May 4 and June 1 (against the USD curve's ~13% drop), while spot BTC hashprice fell 4.2% (0.00048 BTC to 0.00046 BTC). Because BTC-denominated hashprice strips out BTC price, this muted repricing isolates the forward market's read on difficulty and fees: with BTC price weakness removed, BTC hashprice expectations shifted only modestly.

Dividing USD contract values by BTC contract values reveals the implied BTC price embedded in the forward hashrate market. Implied BTC price fell across May, ending near $71,000–$72,000 by June 1, tracking spot’s month-end retreat.

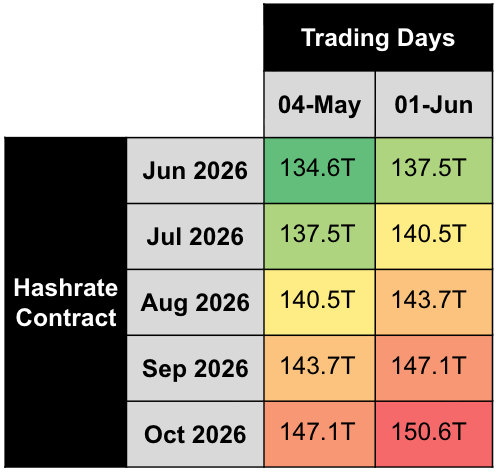

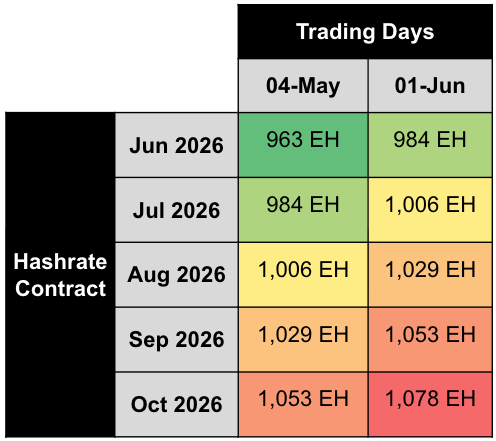

Assuming 0.019 BTC per block in transaction fees, we can also back out implied difficulty and network hashrate expectations:

Note: figures assume 0.019 BTC per block transaction fee collection on May 4 and June 1, 2026.

Based on this analysis, the forward market priced in an average ~2% increase in difficulty and hashrate expectations for the June–October 2026 period during May 2026. Holding implied BTC price roughly flat into the summer while the USD-denominated hashrate forward curve slopes down requires rising difficulty, and the forward market is pricing exactly that: implied hashrate climbed from ~984 EH/s at the June contract to ~1,078 EH/s by October (+9.5%). However, this snapshot has since been overtaken: as of early June, the USD-denominated hashrate forward curve has flipped into contango through to October 2026, repricing the near term toward a summer difficulty pullback rather than an uninterrupted climb.

Concluding Thoughts and Looking Ahead

As of early June, BTC has slid further down to around ~$60,000 and USD hashprice sits near $27-28 per PH/s/day. Conflict in the Middle East has reignited. The strait had been contested for much of the period; on June 1 Tehran broke off talks and moved to fully close it, sending oil sharply higher. Mining economics caught a break from the February–March all-time lows, but that has now firmly reversed.

The 4CP Question: Will Texas Curtailment Bend Difficulty Again?

Four Coincident Peak (4CP) is the mechanism ERCOT uses to allocate transmission costs to large Texas loads. A facility’s transmission charges for the following year are set by its demand during the four 15-minute intervals of highest grid-wide demand (one in each of June, July, August, and September). Miners with the right metering and load-control respond by curtailing during the hours those peaks are likely to form (hot summer afternoons), removing meaningful hashrate from the network for short, predictable windows. With a large share of global hashrate concentrated in ERCOT (~17%), 4CP avoidance is visible at the network level: block times slow down during peak hours, and the cumulative effect tends to pull network difficulty lower across the summer epochs.

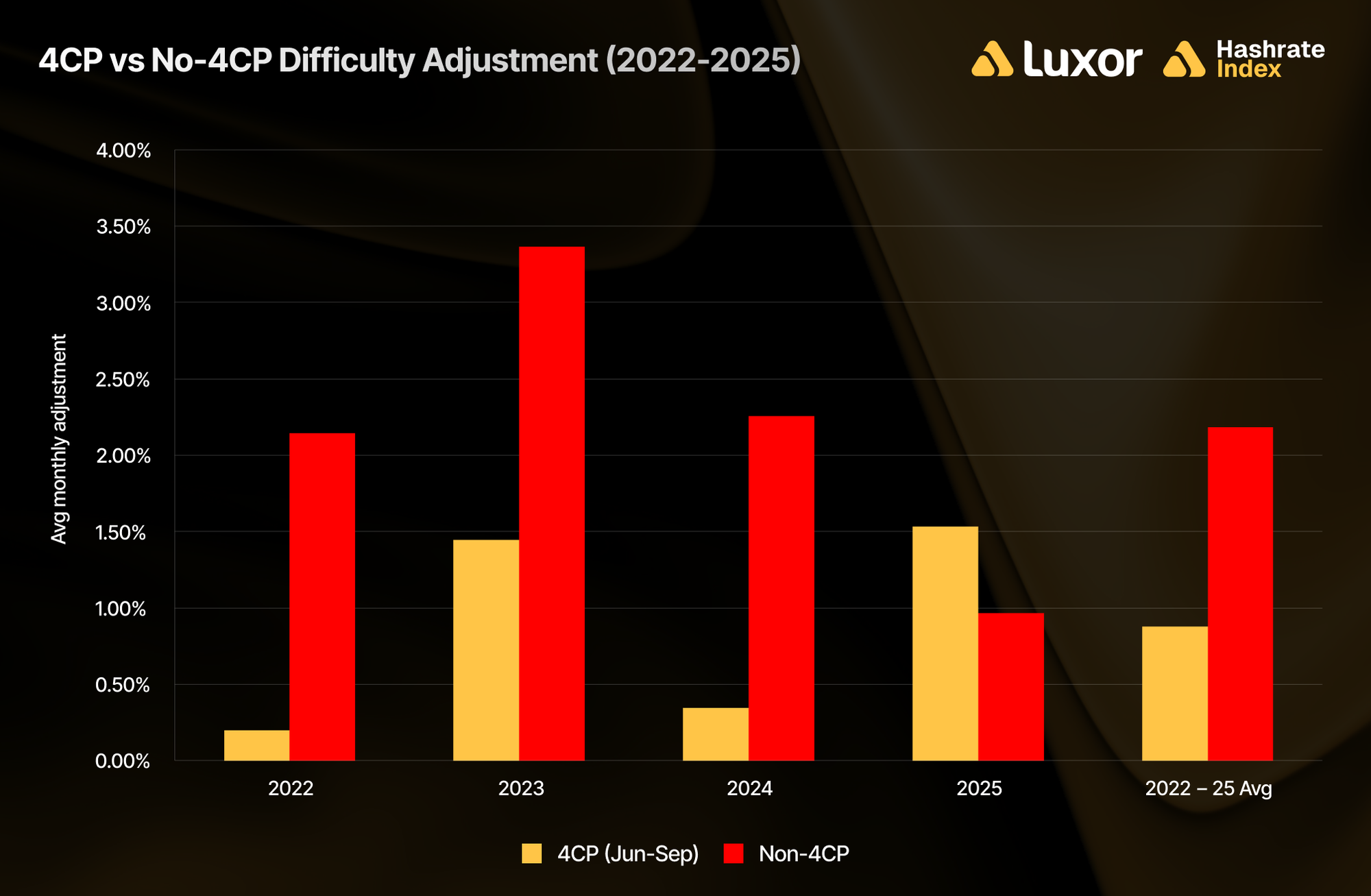

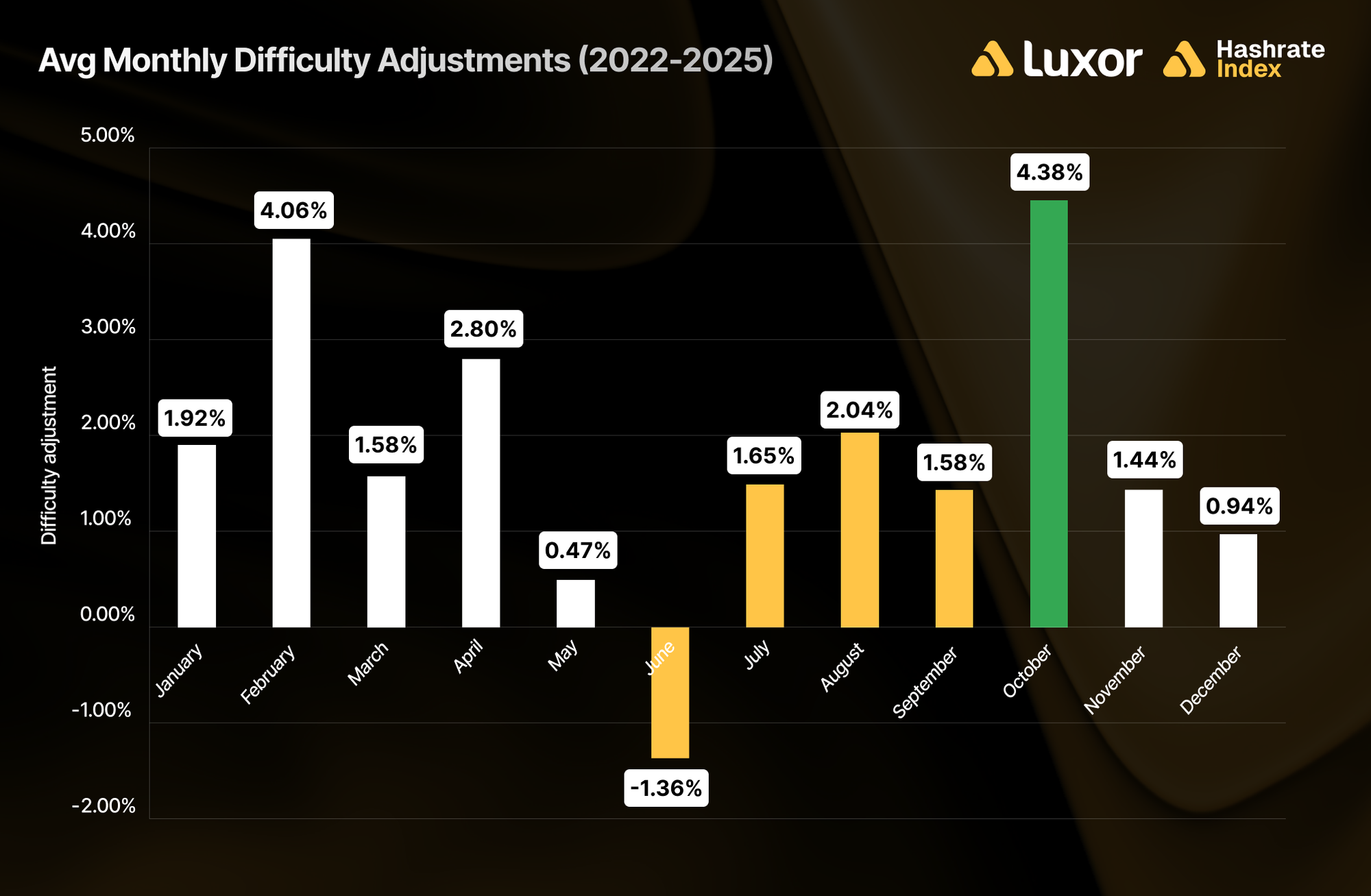

The pattern is consistent across four prior seasons. From 2022 to 2025, difficulty adjustments during the 4CP months (June–September) averaged +1.03% per month against +2.17% for the rest of the year, a 1.1 percentage point seasonal drag.

The whole-season average understates it, because the curtailment concentrates in June and the rebound concentrates in autumn: averaged across 2022–2025, June is the only month with a negative mean adjustment (−1.36%) and has printed negative every year (−0.53%, −0.54%, −0.42%, and −3.96% in 2025), while October is the strongest month of the year (+4.38%).

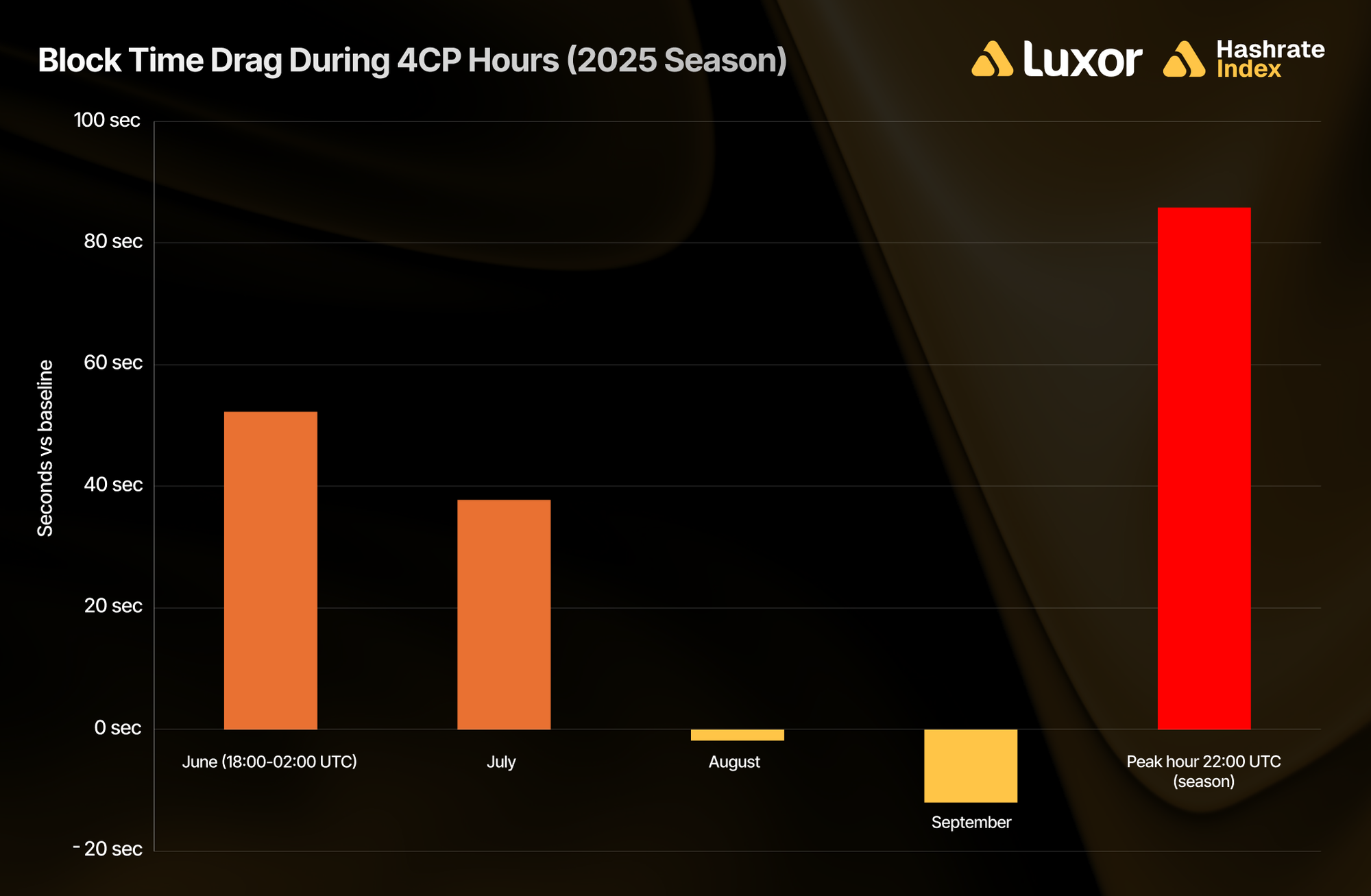

Block times corroborate this. ERCOT's official 2025 4CP peaks landed at 22:00–22:30 UTC on June 19, July 30, August 18, and September 4. Across the season, blocks at the 22:00 UTC peak hour averaged 12.45 minutes against an 11.02-minute baseline (86 seconds slower). The drag was sharpest in June, when blocks during the 18:00–02:00 UTC avoidance window ran 52 seconds slower than the rest of the day and the June 19 peak hour itself averaged 16.60 minutes (66% above target). July still showed a 38-second drag, but by August and September it had faded away back to baseline as the network's hashrate recovery began.

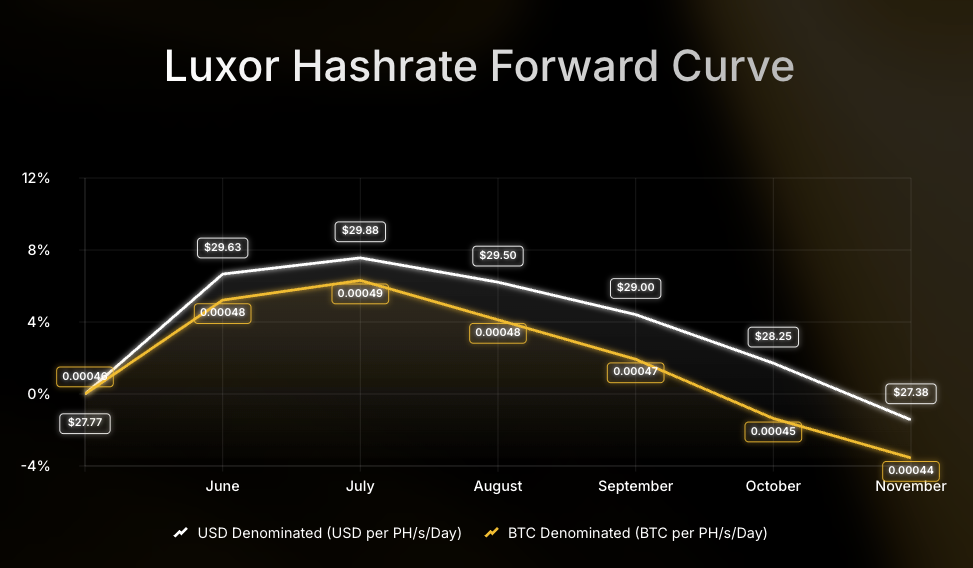

The forward market is pricing in the summer slowdown. The front-end of the hashrate forward curve is in contango: June and July 2026 contracts are currently trading at ~$30, a ~6.6% premium to spot. Contracts through August to October are also above spot, flipping to a $27.38 discount in November. Forward sellers are pricing weaker June–September hashrate (stronger hashprice), as Texas miners are expected to curtail during peak intervals. The back-end backwardation (discount to spot) in November prices the autumn rebound as curtailment risk eventually lifts and difficulty recovers — like a beach ball held under water.

Looking Ahead

Looking forward, Luxor's Hashrate Forward Market is pricing in an average hashprice of $28.94 or 0.00047 BTC per PH/s/day over the next six months. Sellers can currently secure this hashprice while buyers have the opportunity to lock in the same hashcost through November 2026.

If you’d like to learn more about Luxor’s Bitcoin mining derivatives, please reach out to [email protected] or visit https://www.luxor.tech/derivatives.

About Luxor Technology Corporation

Luxor delivers hardware, software, and financial services that power the global compute and energy industry. Its product suite spans Bitcoin Mining Pools, ASIC Firmware, Hardware trading, Hashrate Derivatives, Energy services, a Miner Management software, Commander, and a bitcoin mining data platform, Hashrate Index.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}