Luxor Hashrate Lookback Series – April 2026

April 2026’s hashrate and hashprice trends, forward market participation, trading activity and contract performance.

Luxor’s Monthly Lookback Series is a deep dive into Bitcoin hashrate market activity. In this post, we cover April 2026’s hashrate market and hashprice trends, forward market participation, trading activity and contract performance.

Summary

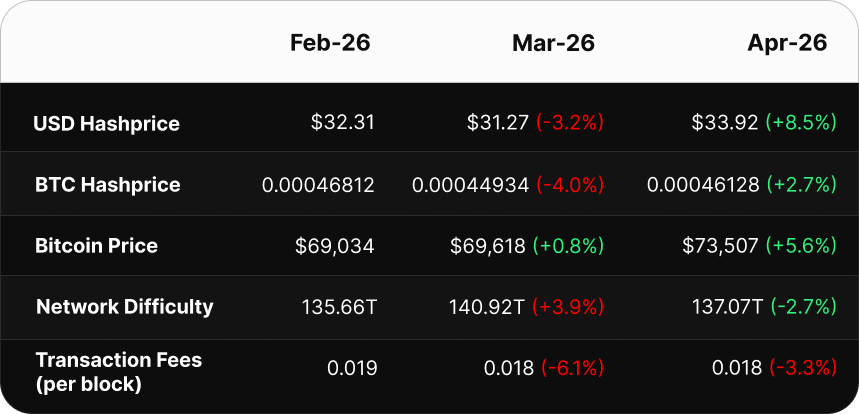

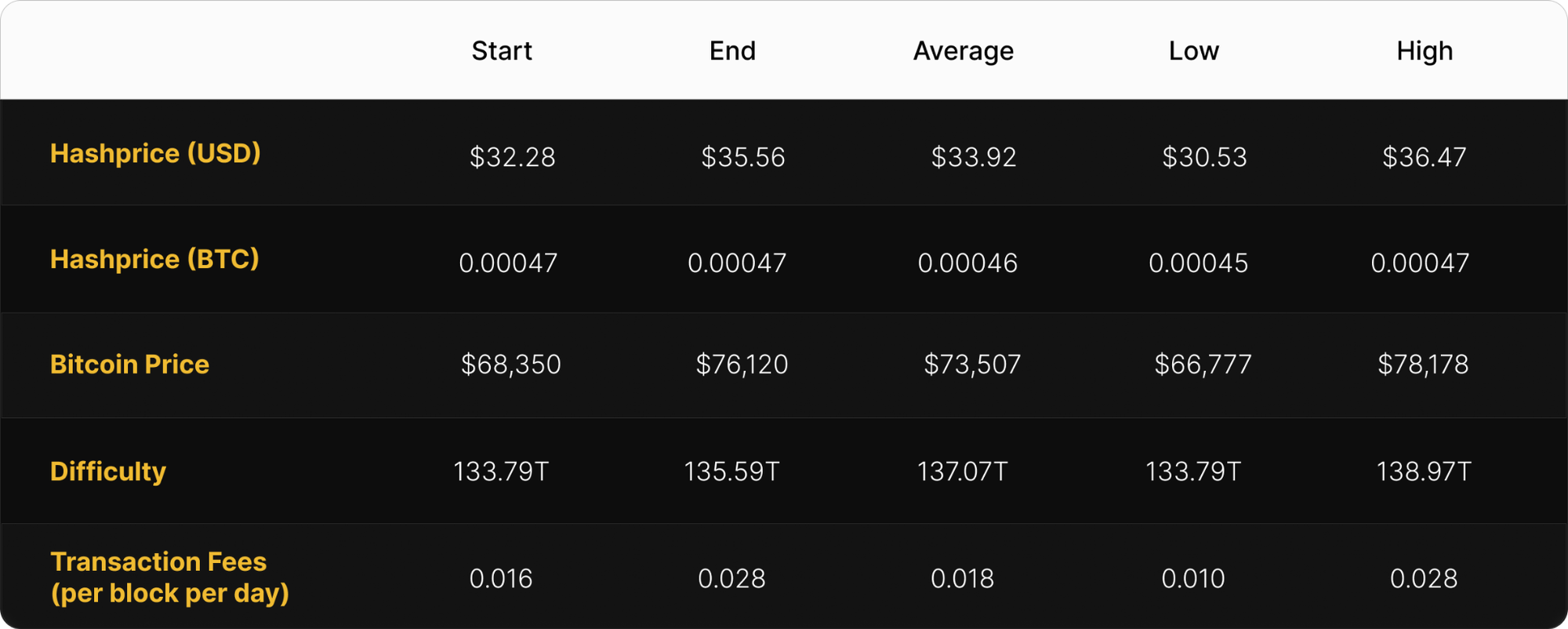

- Modest Rebound in Mining Economics: Monthly average USD hashprice rose 8.5% to $33.92 per PH/s/day, the first increase since the all-time low streak began in February. Monthly average BTC price rose to $73,507 (+5.6%), network difficulty fell to 137.07T (−2.7%), and BTC hashprice rose to 0.00046 BTC per PH/s/day (+2.7%).

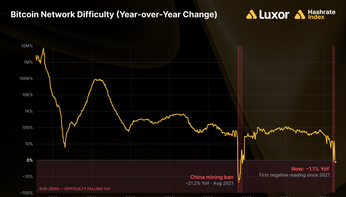

- Difficulty Holds Below 1 ZH for Four Straight Epochs: April delivered two unremarkable adjustments: +3.87% on April 3 and −2.43% on April 17. Network difficulty has now stayed below 139.70T (the 1 ZH/s equivalent) for four consecutive epochs spanning March 20 through May 2, the longest sub-1 ZH/s stretch since the network first crossed the threshold in September 2025. The May 2 adjustment of −2.30% took difficulty down to 132.47T (948 EH/s), pulling it back near the March 20 trough (133.79T) rather than recovering. Marginal hashrate that went offline at all-time low hashprice has not yet returned.

- Split Results in USD-Denominated Hedging: USD-denominated 5/4/3-month sellers captured premiums of 5.6% to 15.4% versus spot, but 2-month and 1-month sellers locked in below spot settlement (−10.3% and −7.1%) as USD hashprice rallied into month-end.

- BTC-Denominated Buyers Win on the Difficulty Story: BTC-denominated buyers outperformed at every horizon. This was driven by six straight months of unexpected contraction in network difficulty, beginning after difficulty peaked at 155.97T on October 29, 2025.

- Forward Curves Repriced Higher, Asymmetrically: May–Sep 2026 USD hashrate contracts rose ~17% during April and ~20% through May 4 as the forward market priced in BTC price recovery. BTC-denominated hashrate contracts rose more modestly (~4.5% across the curve). Implied network hashrate expectations fell ~4.0%, signalling that the market doesn’t expect the hashprice tailwind to bring marginal hashrate back online in the near future.

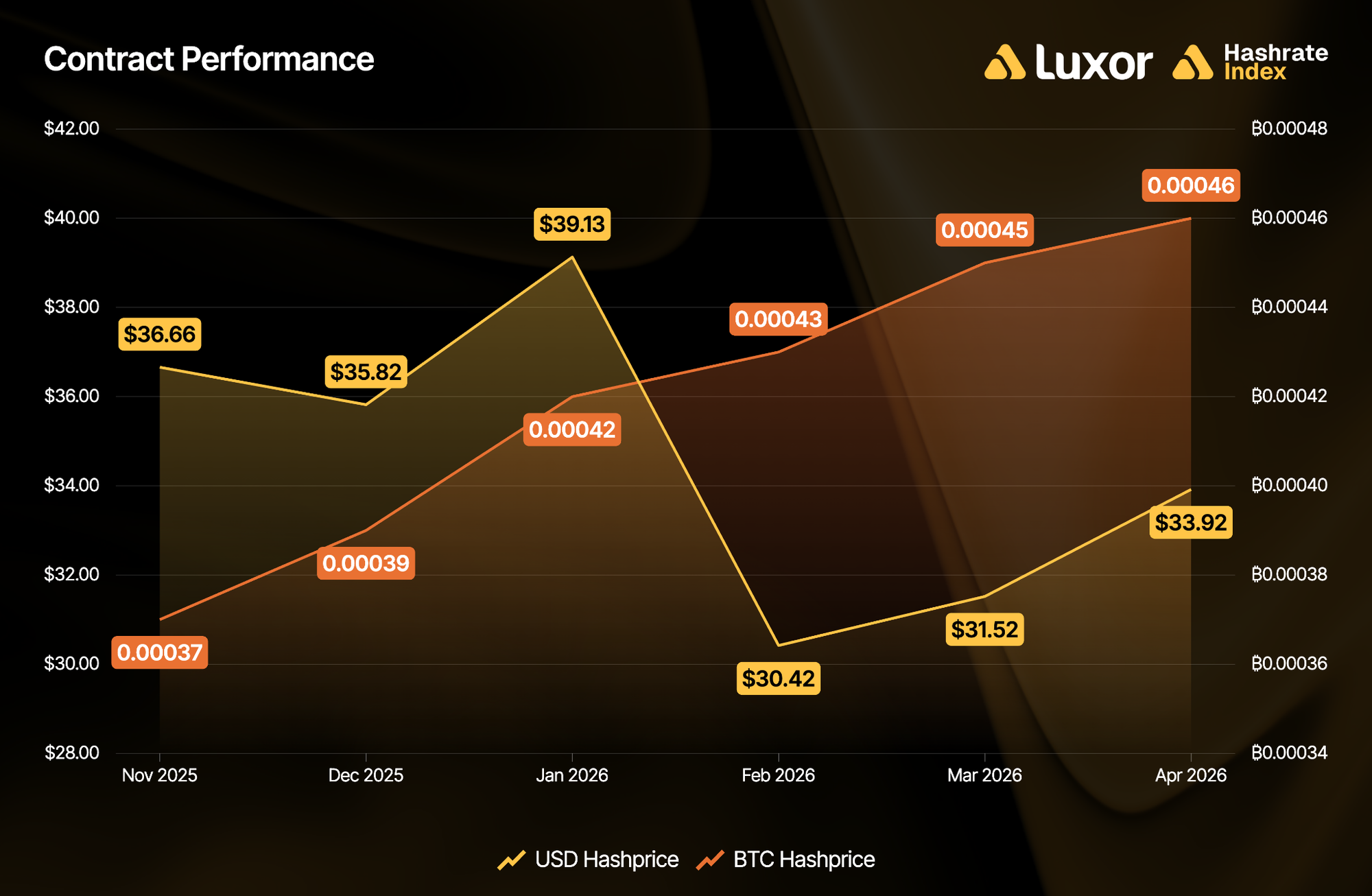

April 2026 Spot Hashprice & Its Constituents

USD Hashprice — A Modest Rebound

After two consecutive all-time low monthly averages, April broke the streak.

Monthly average USD hashprice rose 8.5% from $31.27 to $33.92 per PH/s/day, driven by a 5.6% recovery in BTC price and a modest decline in network difficulty. Hashprice opened the month at $32.28, dipped to $30.53 on April 5 (the monthly low), and traded above $35 for most of the second half before closing the month at $35.56. Hashprice is currently back in the December 2025–January 2026 range of $37–$39, and on the lower end of 2025’s monthly averages, which ranged from $37.89 to $59.38 with a mean of ~$50.69.

BTC Price — Rallying With Equities

BTC opened April at $68,350, rallied 11.4% throughout the month, and closed at $76,120, averaging $73,507 (+5.6%) versus March's $69,618 average. April 22 marked the monthly high at $78,178, BTC's highest level since early February.

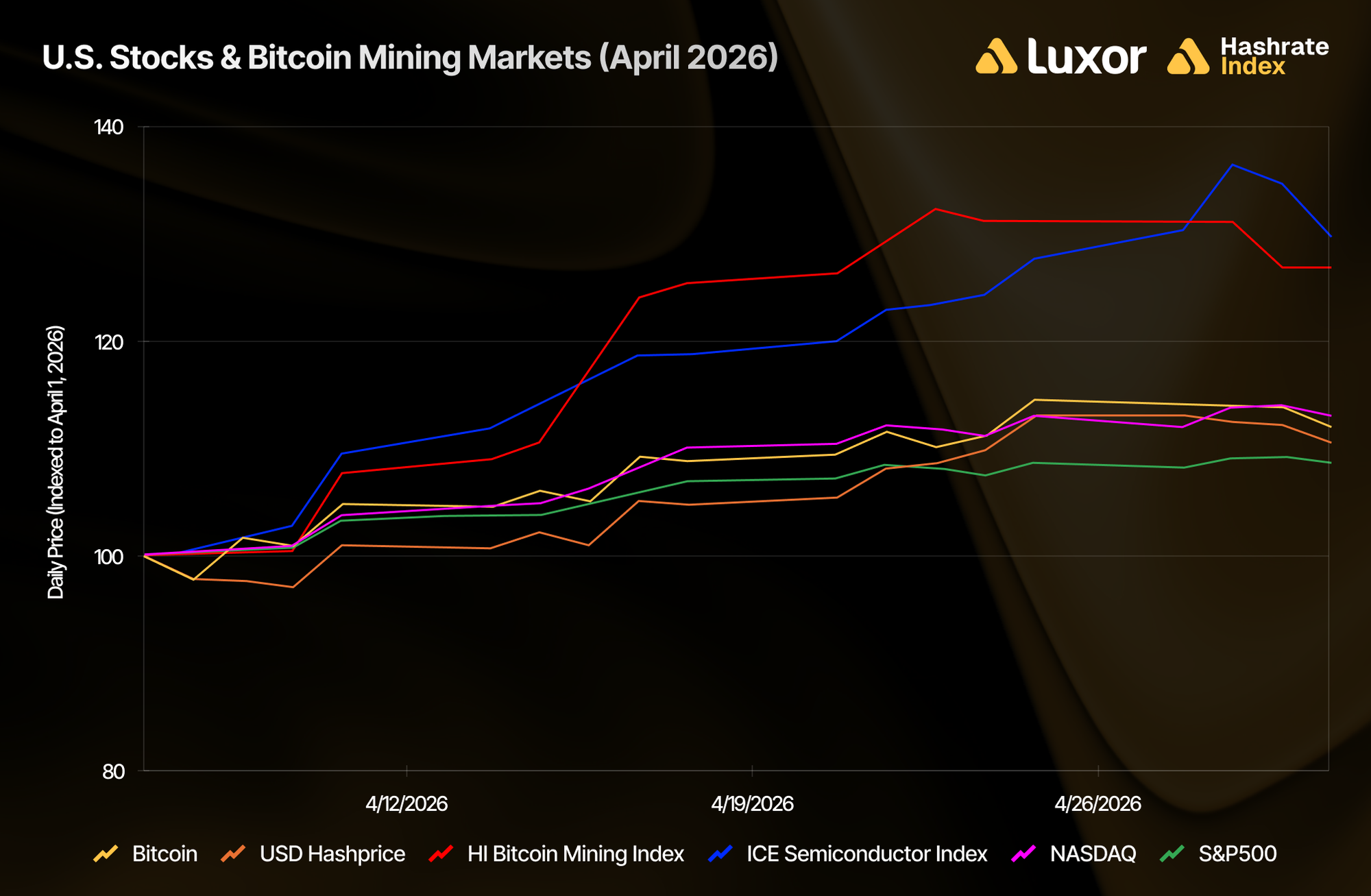

What stands out is what happened alongside BTC's recovery. April 2026 was one of the strongest months in modern Wall Street history: the S&P 500 returned +10% and the Nasdaq Composite +14%, both their best month since November 2020, on a wave of upside earnings surprises and AI CapEx guidance raises from mega-cap tech. The semiconductor complex led the broader rally — the ICE Semiconductor Index gained +36% — Bitcoin mining equities followed close behind, with Hashrate Index's Bitcoin Mining Index up +27%. Bitcoin itself participated but lagged the move, returning +11% and tracking the broad equity indexes more closely than the AI-adjacent corners of the market. After leading equities lower in March, BTC followed equities higher in April.

This reversal is a signal. The narrative shift from February ("worst drawdown of the cycle") and March ("flat with spikes") sharpened in April: BTC re-coupled with risk-on assets. However, the drawdown context from prior months still isn't resolved. BTC closed April 2026 ~40% below its ~$126,000 October 2025 peak.

Network Difficulty — A Quiet Month, Hashrate Holds Below 1 ZH/s

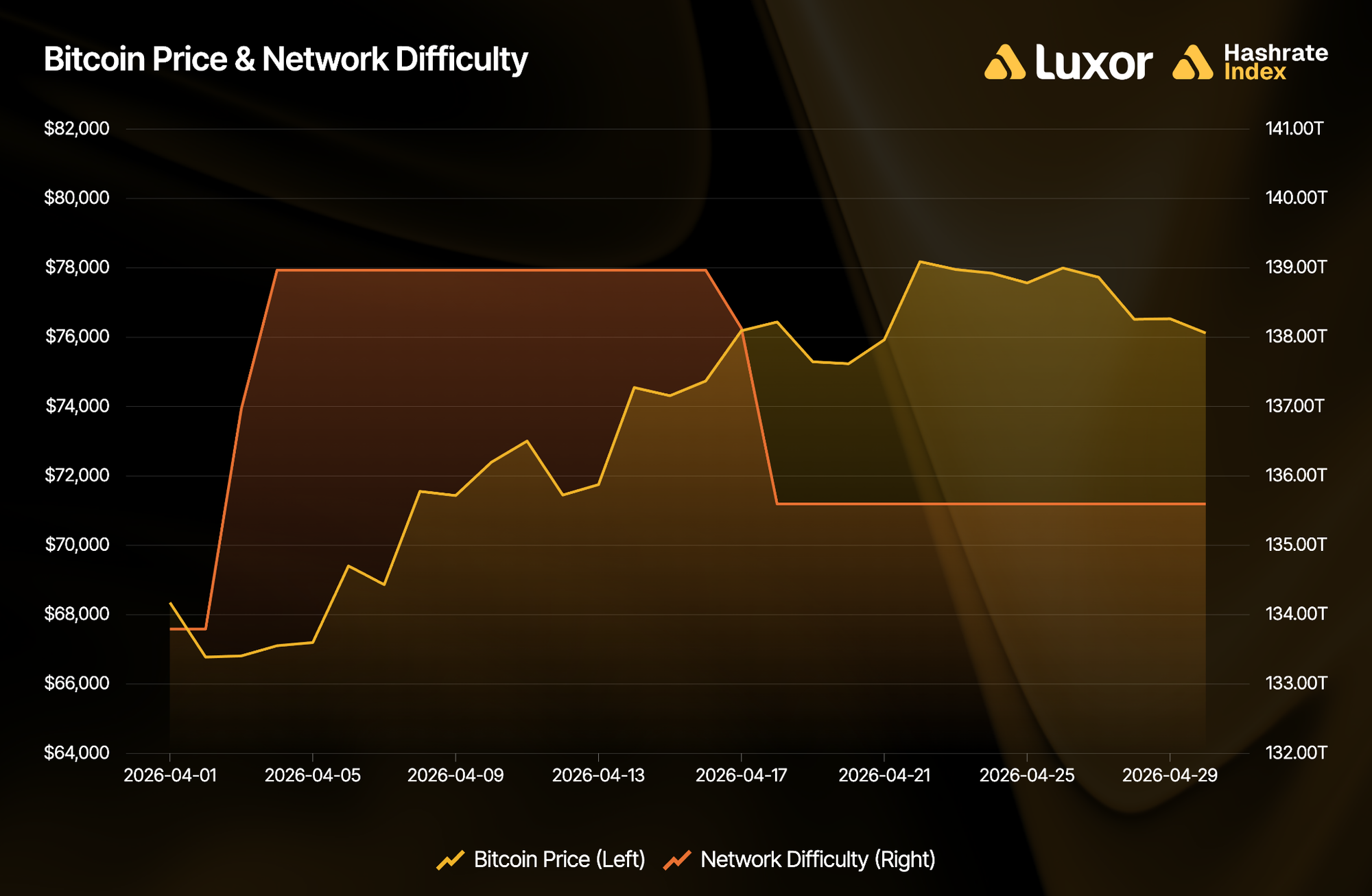

April delivered two unremarkable difficulty adjustments after Q1's turbulence.

The first was an upward adjustment on April 3: +3.87% from 133.79T (~958 EH/s) to 138.97T (~995 EH/s), responding to marginal hashrate that came back online after March's −7.76% drop. The second was a downward adjustment on April 17: −2.43% from 138.97T (~995 EH/s) to 135.59T (~971 EH/s) — neither extreme nor particularly informative on its own.

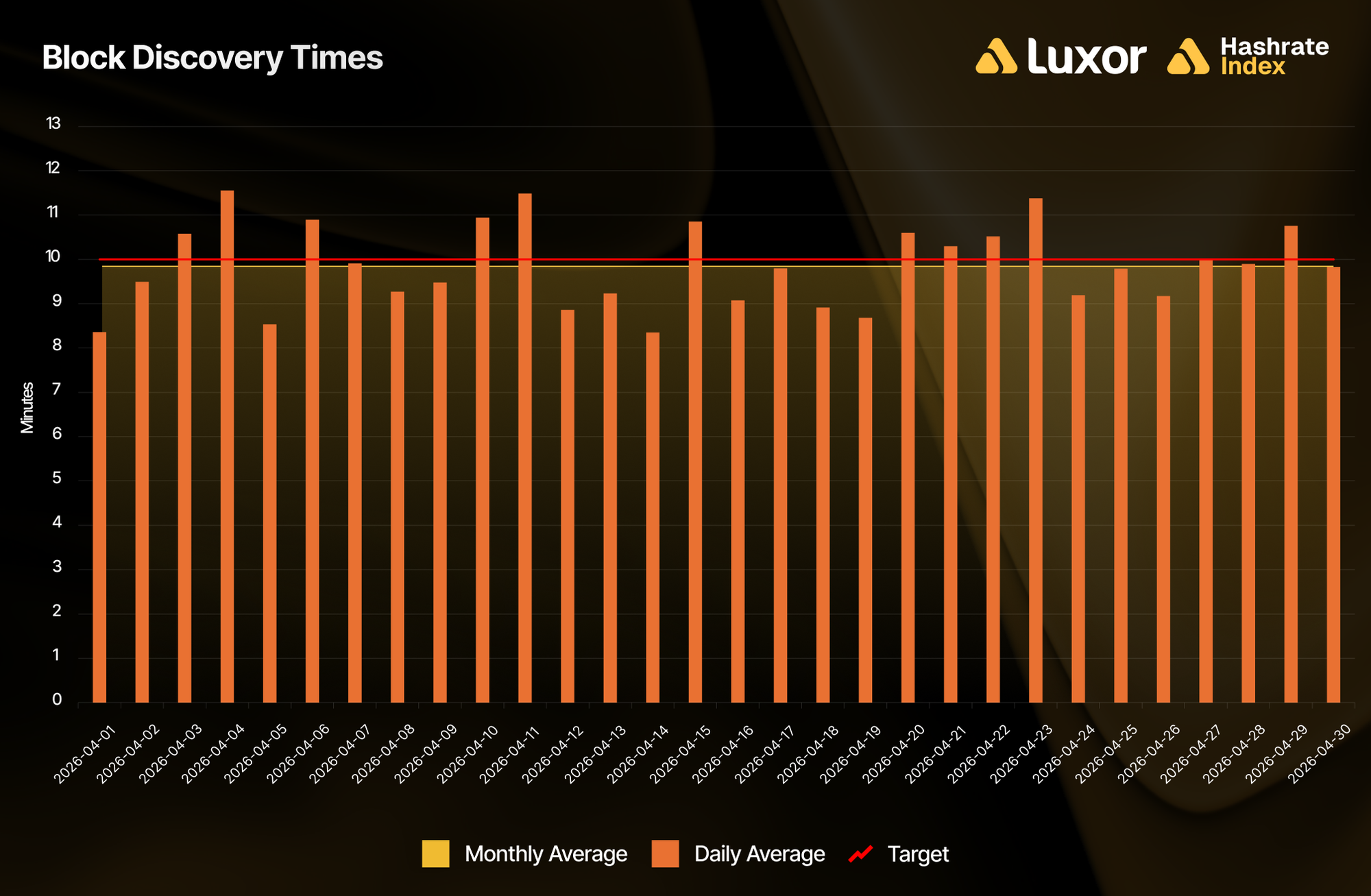

Set against the recent past, two facts stand out. First, neither of the two April difficulty epochs rank anywhere near the modern ASIC era top-10 in either direction; after February's −11.16%/+14.73% whipsaw and March's −7.76% drop, April reads as the network finding equilibrium. Case in point: block times averaged 9.86 minutes per block for the month, just slightly under (but close enough) to the network target of 10 minutes.

Second, difficulty has now held below 139.70T — the 1 ZH/s equivalent — for four consecutive epochs. The March 20 adjustment dropped difficulty to 133.79T (~958 EH/s); April 3 lifted it to 138.97T (~995 EH/s); April 17 pulled it back to 135.59T (~971 EH/s); and May 2 cut it further to 132.47T (~948 EH/s). That spans 43 days, the longest sub-1 ZH/s stretch since the network first crossed 1 ZH/s in September 2025.

Notably, the May 2 difficulty epoch (132.47T) landed near the March 20 epoch (133.79T) rather than recovering toward the 1 ZH/s baseline. This means the marginal hashrate that went offline during Q1’s all-time low hashprice period has not come back, even as USD hashprice rebounded 8.5% in April. The question of whether that offline hashrate is structurally retired or just curtailed remains unresolved, but the May 2 reading argues against a quick marginal hashrate return.

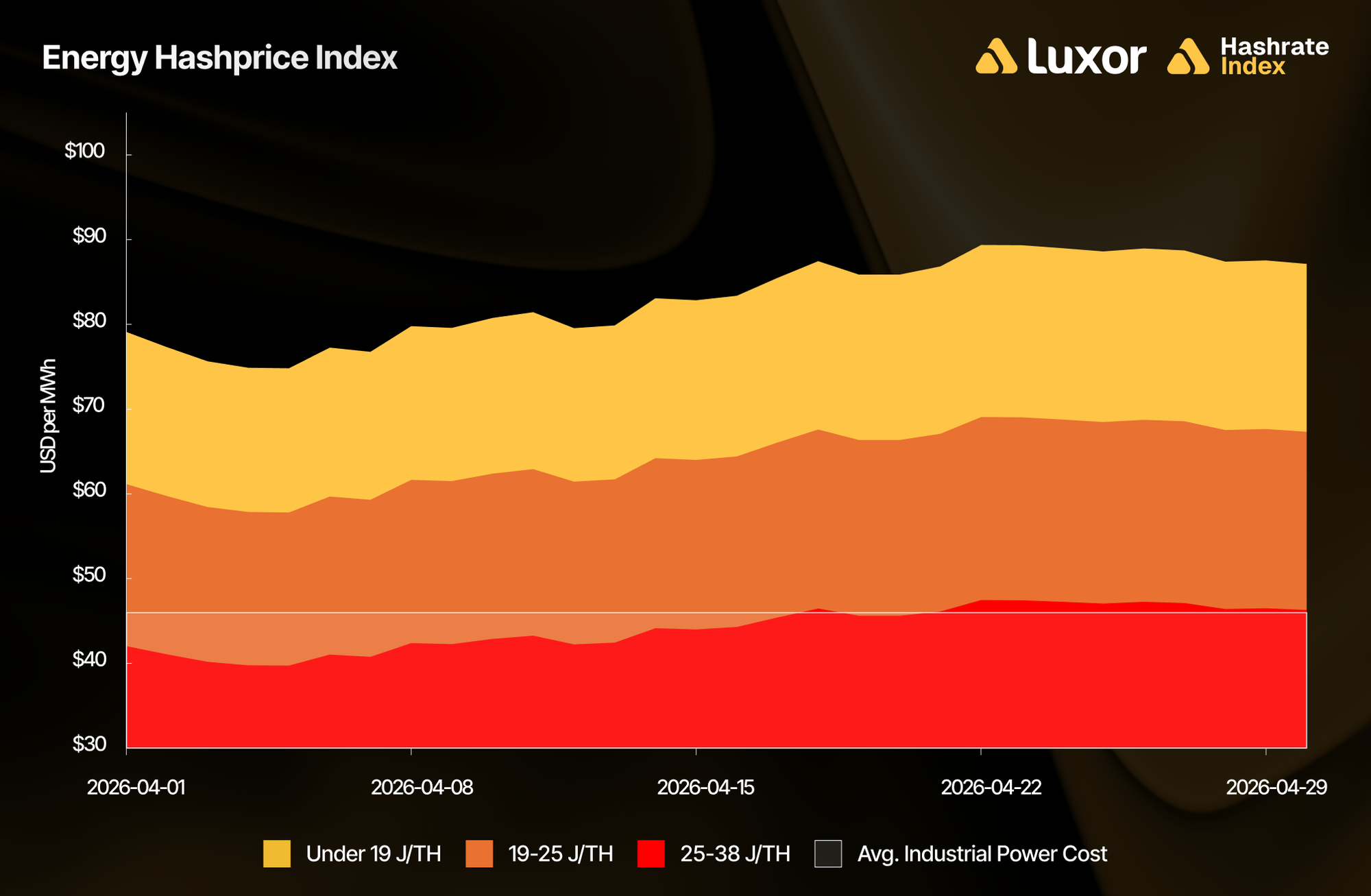

The low-hashprice environment continues to pressure marginal machines, though April's rebound eased the squeeze. Implied mining revenue per unit of electricity consumed averaged approximately $83/MWh for fleets running under 19 J/TH, $64/MWh for 19–25 J/TH fleets, and $44/MWh for 25–38 J/TH fleets; meaningful step-ups from March's $77/$59/$41 readings. At an estimated network-average power cost of $46/MWh, 25–38 J/TH fleets sit just below breakeven on average, versus a deeper deficit through Q1.

Transaction Fees — Quiet, Again

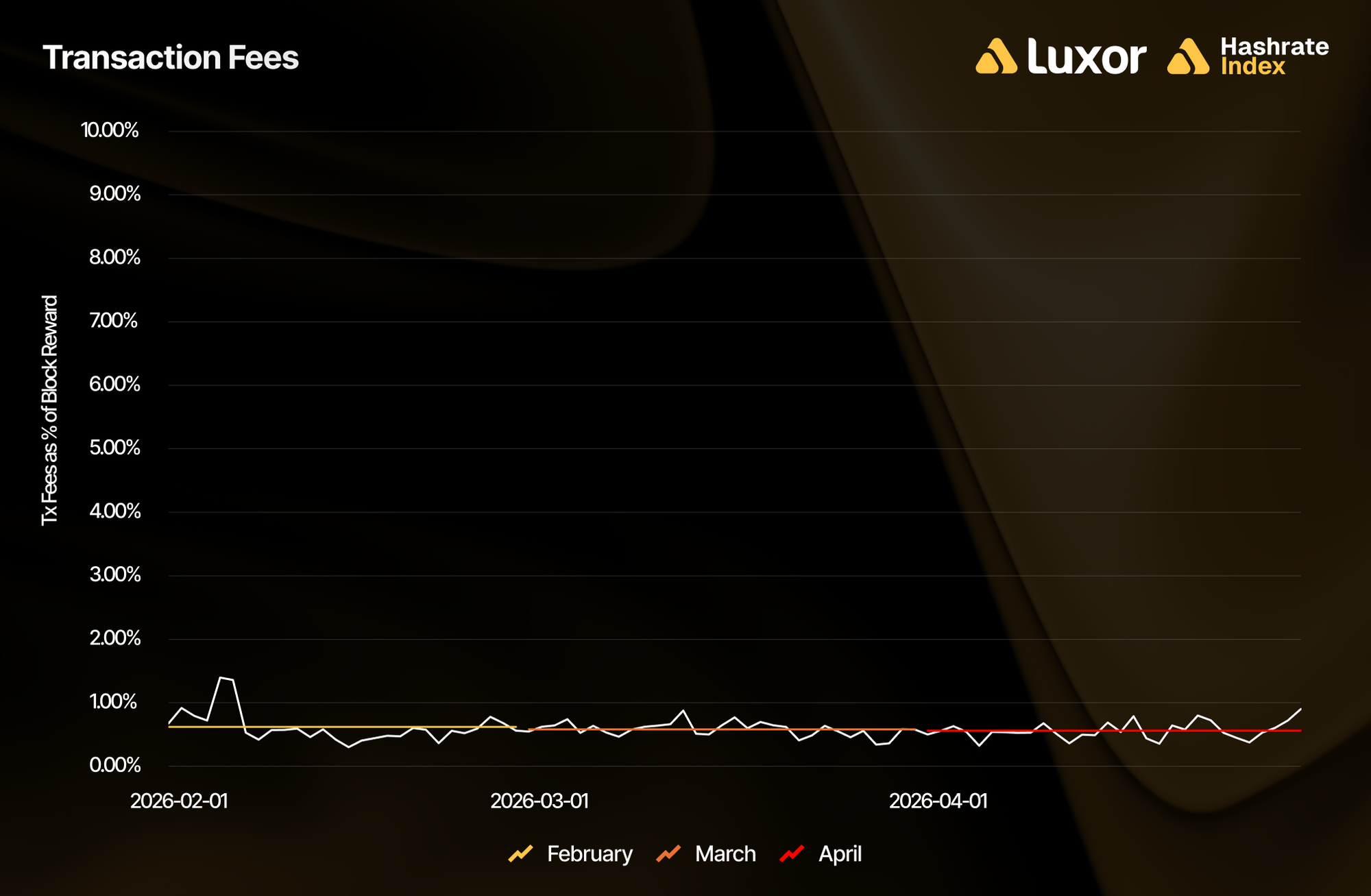

Average fee collection fell 3.3% to 0.0177 BTC per block in April, continuing the subdued fee environment that has persisted since the 2024 halving. Fees accounted for approximately 0.56% of total block rewards in April; this proportion has been under 1% since July 2025. In USD terms, average fee revenue per block was approximately $1,306 (+2.1%), marginally above March's $1,279.

BTC Hashprice — Up With Difficulty Relief

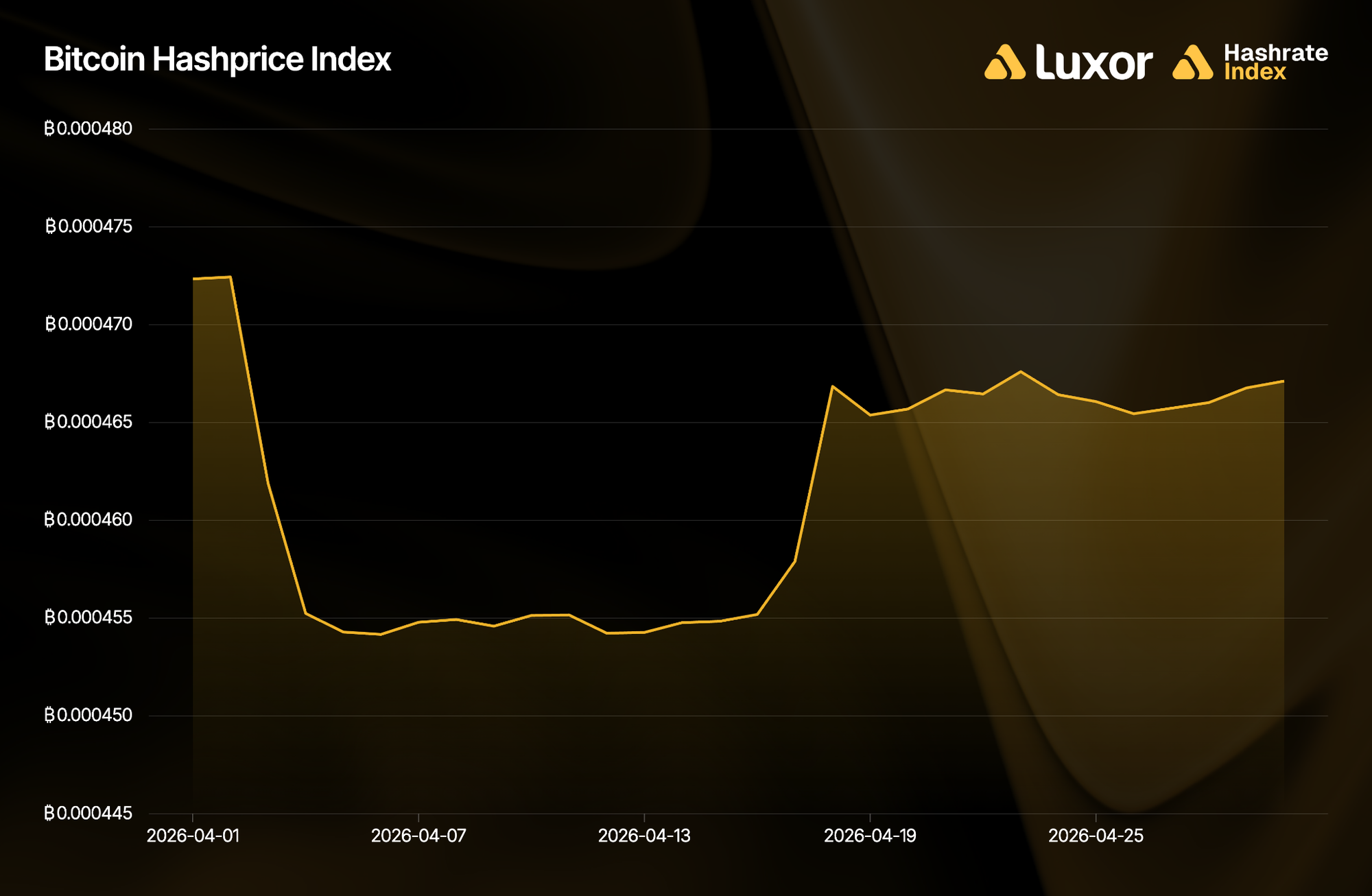

BTC hashprice moved inversely to difficulty, as expected. It opened April at 0.000472 BTC per PH/s/day, declined into the +3.87% adjustment on April 3 to a monthly low of 0.000454 by mid-month, then recovered following the −2.43% adjustment on April 17, closing at 0.000467 BTC per PH/s/day.

Monthly average BTC hashprice rose 2.7% from 0.00044934 to 0.00046128 BTC per PH/s/day — modest but positive, driven by the decline in average difficulty.

April 2026 Hashrate Market Activity

Our analysis of the April 2026 hashrate market focuses on two key points: how the April 2026 hashrate contract traded in previous months and how the forward curve shifted in April, based on pricing for forward hashrate during the month.

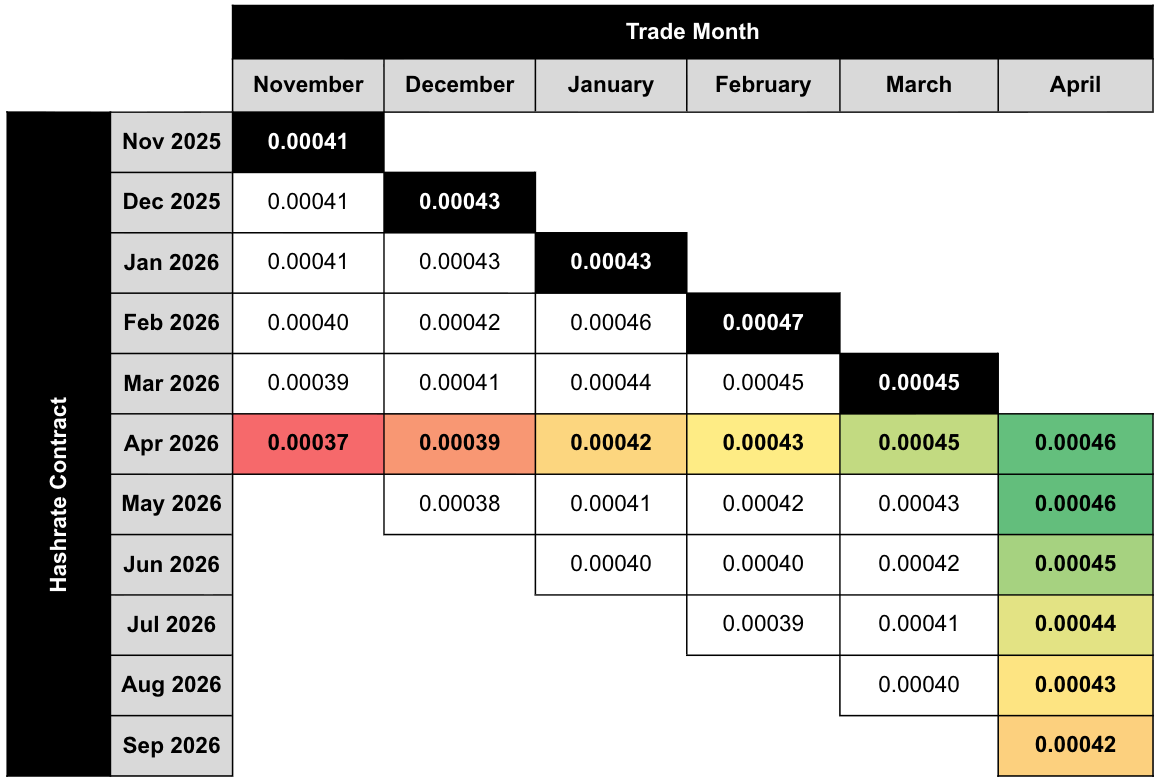

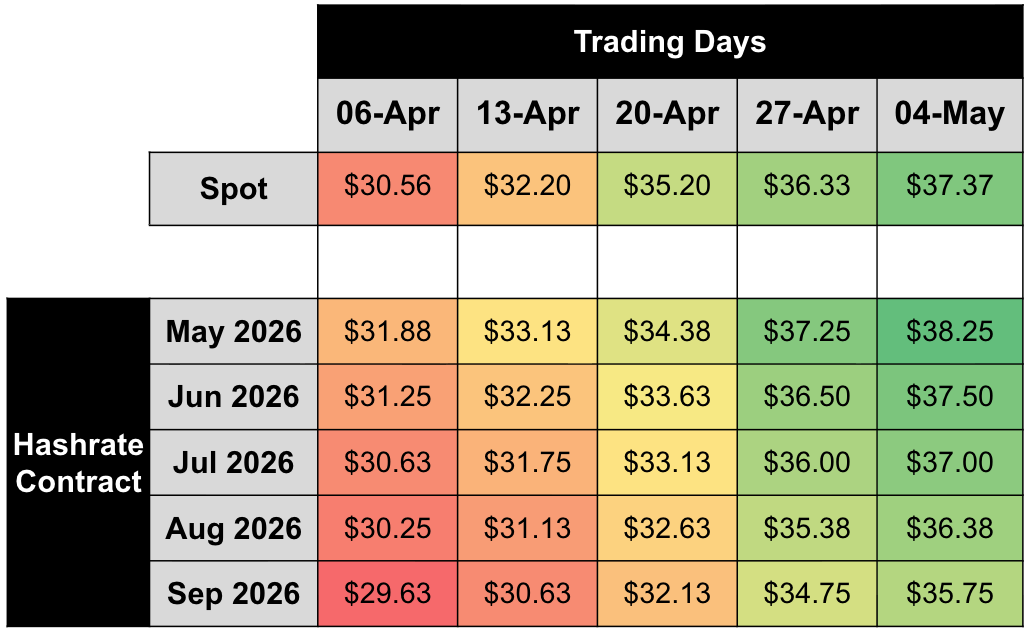

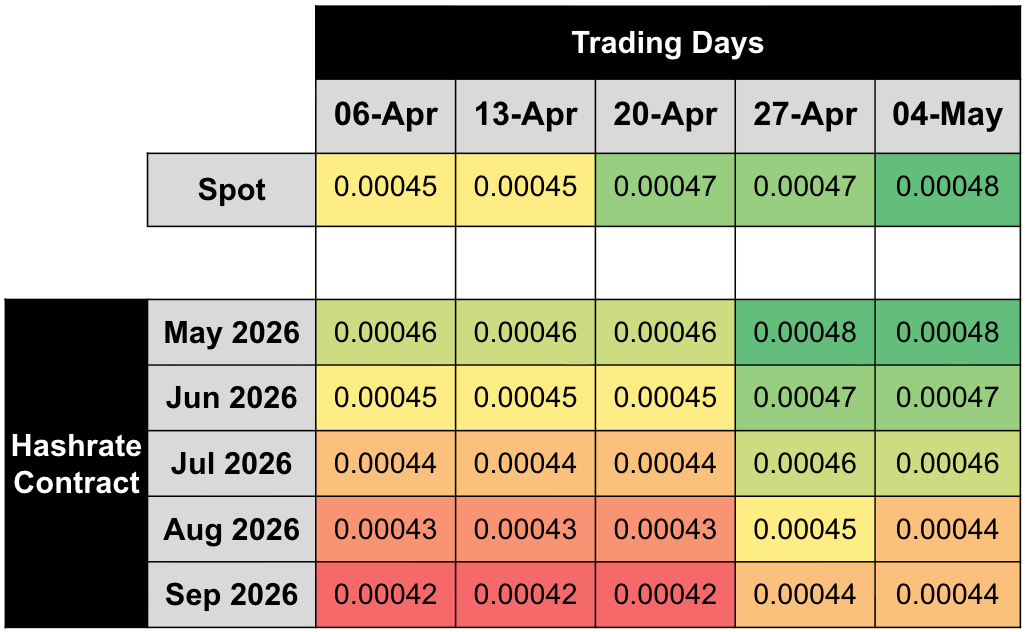

The two tables below show the evolution of Luxor’s USD and BTC-denominated hashrate forward markets from November 2025–April 2026. Rows represent specific monthly contracts, while columns represent each trading month. Cell values indicate the average monthly mid-market hashprice — except for the bold highlighted main diagonal — which shows actual spot hashprice settlement in each month.

This table summarizes both the trading history of the April 2026 USD-denominated contract (colored row) and the forward curve in April (colored column).

This table summarizes both the trading history of the April 2026 BTC-denominated contract (colored row) and the forward curve in April (colored column).

Note: all values (except for the bold highlighted main diagonal) shown in figures represent mid-market rates, the midpoint of the best bid and ask on Luxor's Non-Deliverable Hashrate Forward market. The bold highlighted main diagonal shows actual spot hashprice settlement in each month, measured by Luxor’s Bitcoin Hashprice Index.

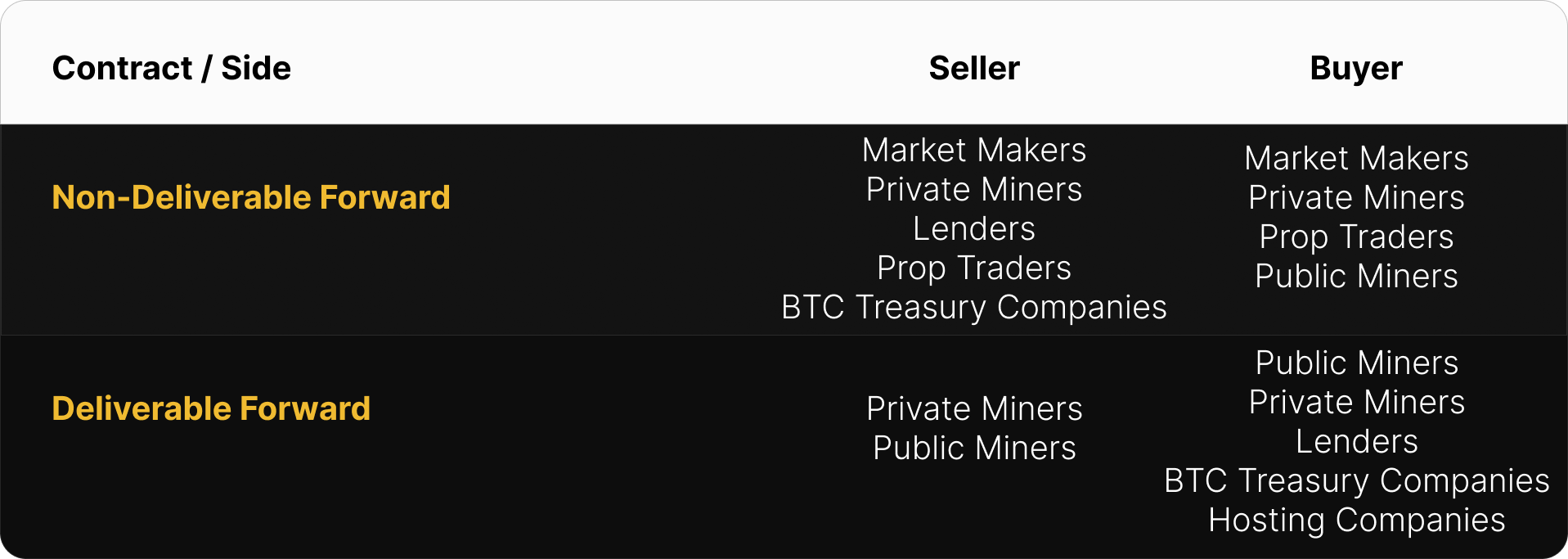

The table below shows the type of market participants on the buy and sell side of Luxor’s deliverable (DF) and non-deliverable hashrate forward (NDF) market. In April, lenders were active on the buy side of the DF market, while public and private miners used the contract to sell forward, receive financing, and expand their fleet.

Since the DF involves upfront payment, it tends to trade at a discount to the NDF, compensating the buyer for the inherent credit risk. We interpret the discount of DFs relative to NDFs as the interest rate in hashrate-based lending markets. Buyers and sellers of the DF with upfront payment can use the NDF to lock-in a fixed yield (cost of capital) instead of having exposure to hashprice uncertainty.

This strategy was used by lenders and Bitcoin treasury companies (buy DF & sell NDF) to earn a BTC-denominated return and by miners (sell DF & buy NDF) to obtain non-dilutive financing. In April 2026, that yield (cost of capital) was 6–13% annualized.

How April 2026 Hashrate Traded

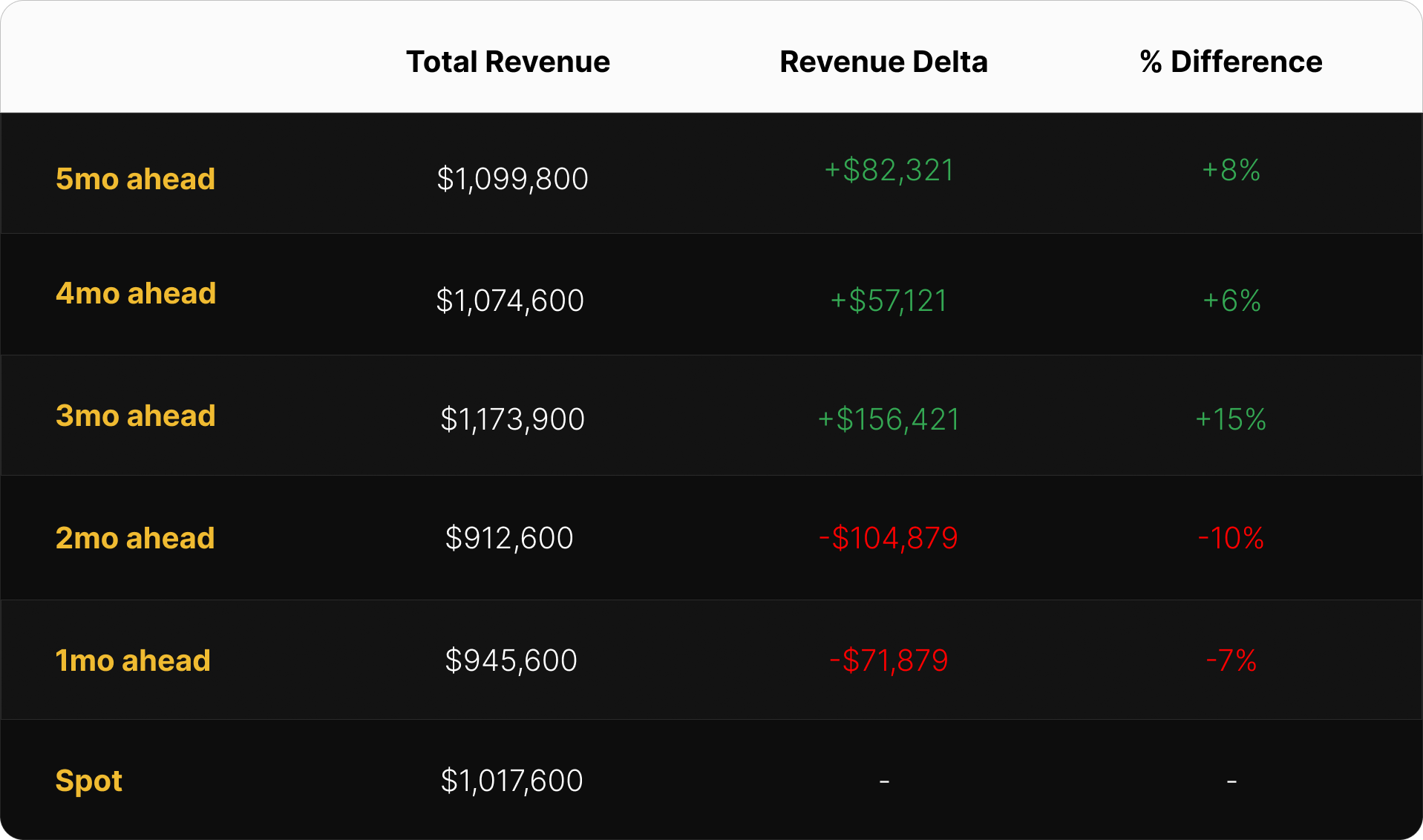

April delivered split results in hashrate hedging, driven by two distinct forces.

In USD-denominated contracts, results depended on hedge horizon: 5/4/3-month sellers won, 2/1-month sellers lost. Forward sellers locked in between $30.42 and $39.13 per PH/s/day versus spot settlement at $33.92. The longer-dated lock-ins (set in Nov 2025–Jan 2026, when BTC was still trading $90,000+) priced spot hashprice expectations far above what materialized. The shorter-dated lock-ins (set in Feb–Mar 2026, at the depths of the all-time low period) priced spot hashprice expectations below what April actually delivered. The optimal USD hedge was a three-month forward sale in January 2026 at $39.13 per PH/s/day (+15.4% vs. spot). The driver of this split was BTC price recovering faster than the forward market had priced in over the prior 30–60 days.

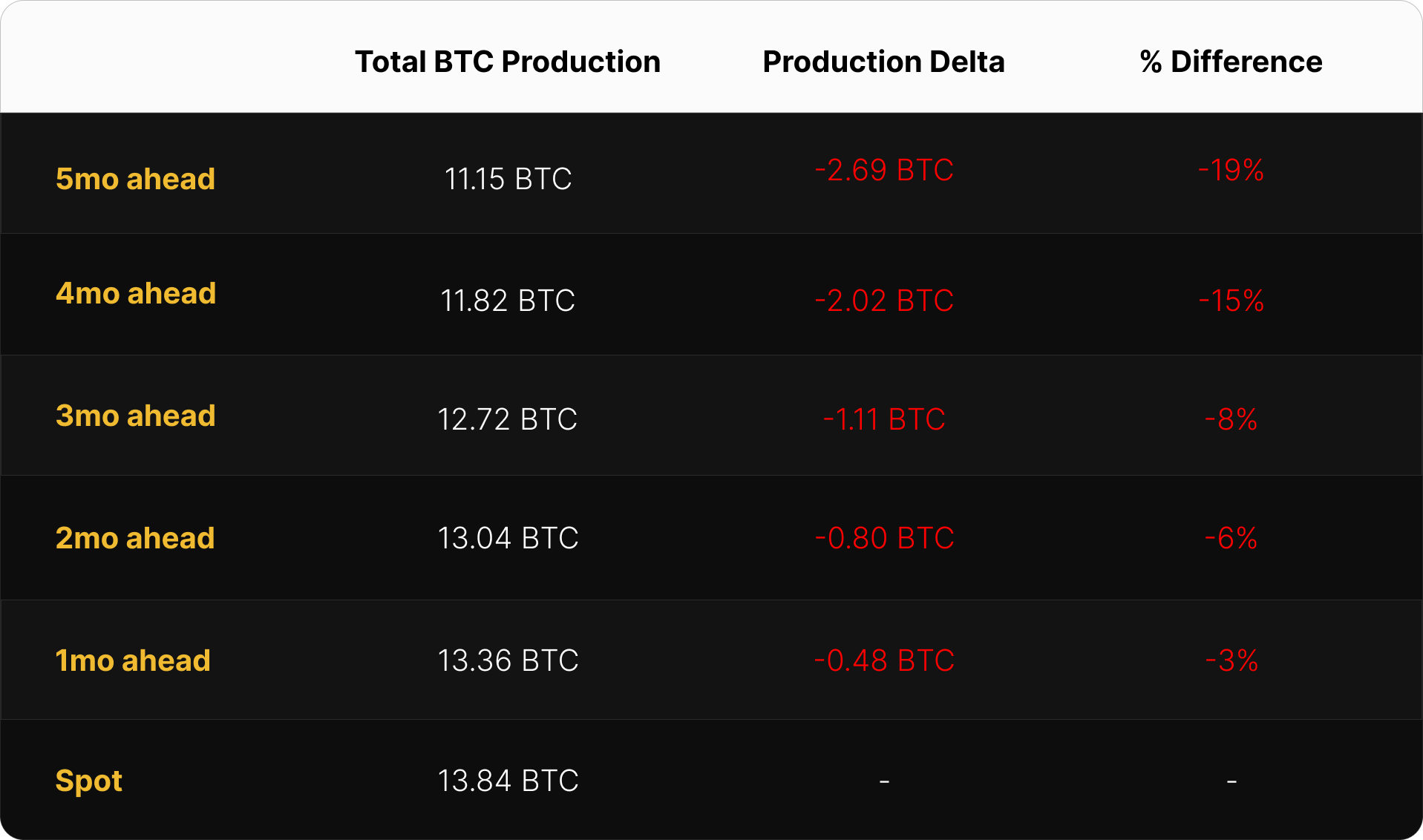

In BTC-denominated contracts, buyers won across the board. Forward sellers received between 0.000372 and 0.000445 BTC per PH/s/day, all below spot settlement of 0.000461. Six straight months of contracting network difficulty (unexpected coming out of 2025's secular growth narrative) kept BTC hashprice settling above forward lock-in rates. This spread compressed sharply at the front of the curve: 5-month BTC sellers (locked in November 2025) gave up 19% versus spot, while 1-month sellers (locked in March 2026) gave up just 3% as the forward market accurately priced April’s BTC hashprice over 30 days.

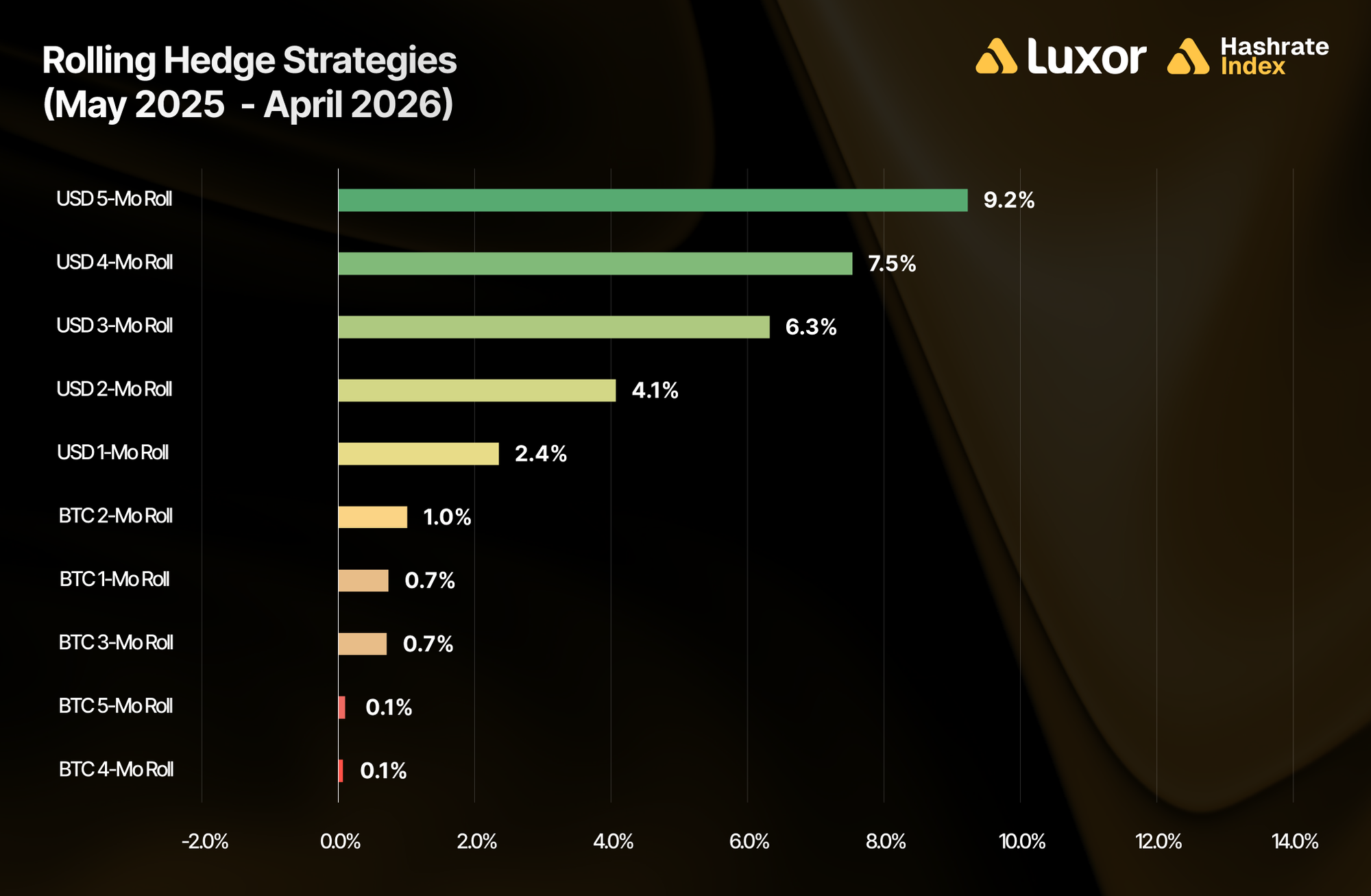

Zooming out, we examine rolling hedge performance across two windows: the trailing twelve months (May 2025–April 2026) and since the April 2024 halving.

Over the past year, rolling USD-denominated hedging strategies outperformed spot mining across the board. The strongest results came from 5-month (+9.2%) and 4-month (+7.5%) USD-denominated forward sales, which generally benefited from locking in a hashprice ahead of compressed spot conditions in early 2026. BTC strategies clustered near flat (+0.07% to +1.02%) — a notable change from the post-halving period, where rolling BTC hedges dominated. With network difficulty essentially flat over the trailing twelve months, what drove that prior outperformance for sellers has faded.

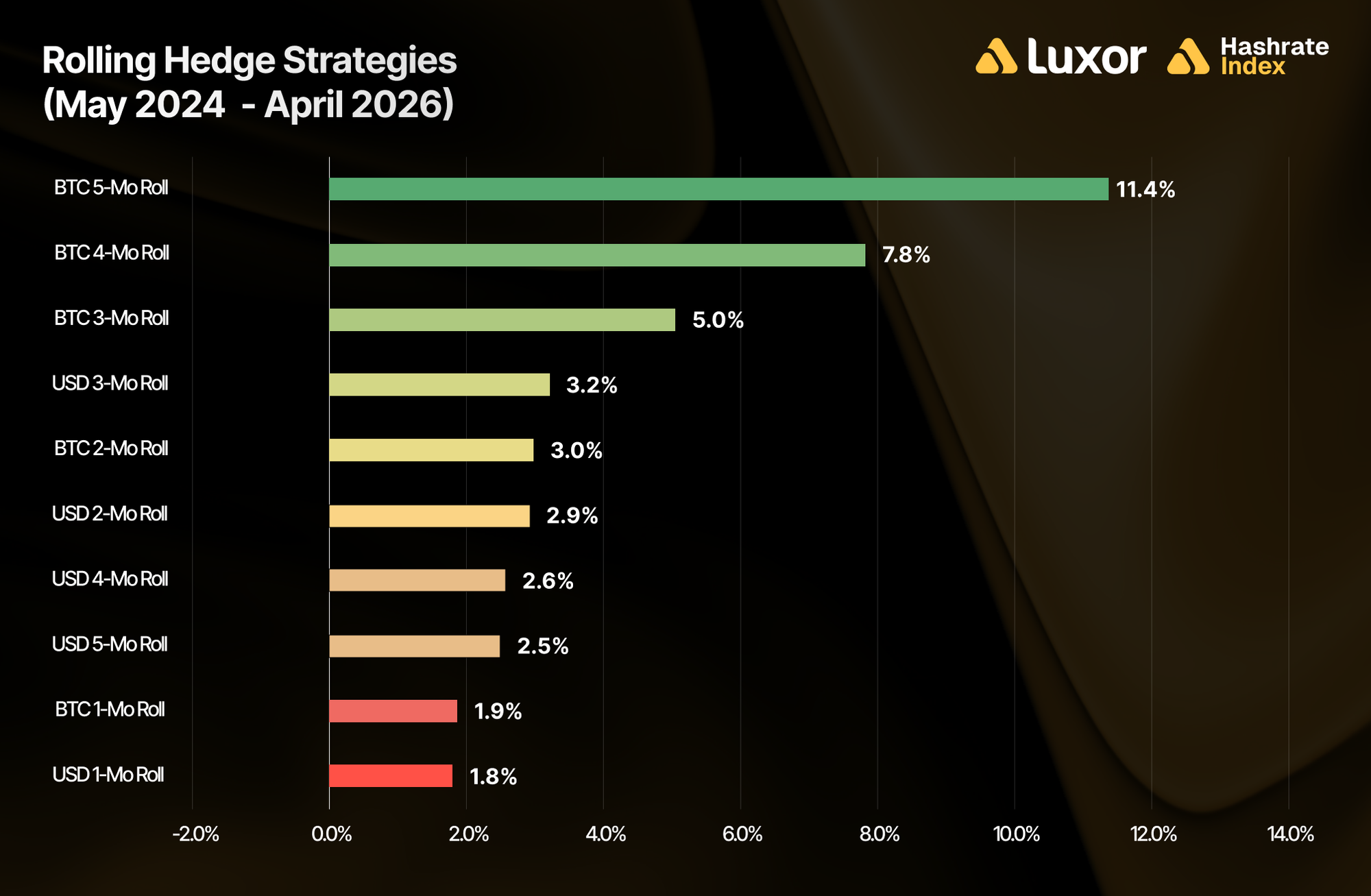

Extending the window back to the 2024 halving still favors BTC-denominated strategies, though the spread continues to narrow. The BTC 5-month roll led all strategies at +11.4% vs. spot, followed by BTC 4-month (+7.8%), BTC 3-month (+5.0%), USD 3-month (+3.2%), BTC 2-month (+3.0%), USD 2-month (+2.9%), USD 4-month (+2.6%), USD 5-month (+2.5%), BTC 1-month (+1.9%), and USD 1-month (+1.8%).

The contrast between the two timeframes is instructive. Which contract denomination outperforms in any given window depends on whether BTC price or network difficulty and transaction fees move faster and further than the forward market anticipated at the time of hedging.

From May 2024 through late 2025, network difficulty expanded faster than forward markets priced in, and BTC-denominated sellers captured the spread. From late-2025 onward, difficulty growth stalled while BTC price weakness compressed USD hashprice below forward expectations; USD-denominated sellers captured the spread instead. The narrowing spread between the two windows reveals that Q4/2025–2026 has been a regime where BTC-denominated hedging programs have lost their edge (due to difficulty growth stalling) as USD-denominated hedging programs now stand out (due to volatile and uncertain BTC price action). Regardless of regime, forward sellers came out meaningfully ahead of operations mining at spot (FPPS) since the halving.

Note: two important caveats apply to both windows. First, figures exclude fees and bid/ask spreads. Second, hedging is a cost of business rather than a revenue generation strategy. Hedgers willingly buy the certainty of predictable cash flows, which increases valuations, reduces capital costs, and ultimately attracts investments.

How Future Hashrate Traded in April 2026

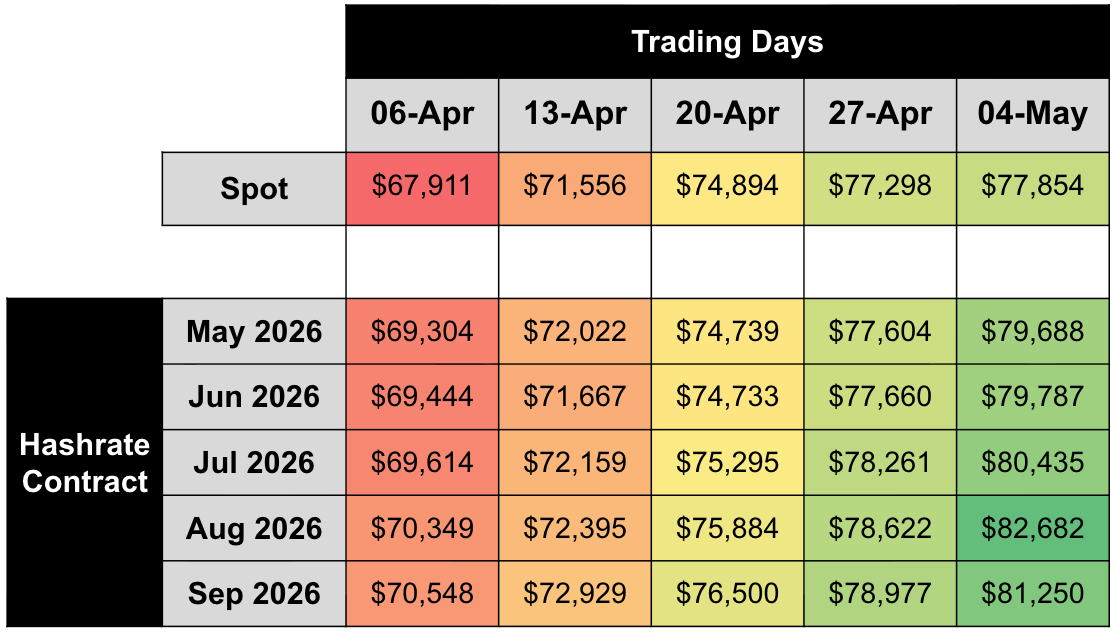

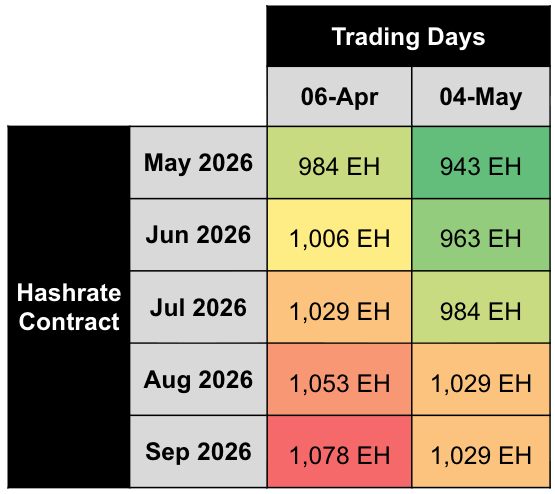

The two tables below summarize the evolution of hashrate forward markets during April 2026, for the subsequent five months from May 2026–September 2026. Rows represent specific monthly hashrate contracts, while columns represent specific trading days. Cell values indicate the average daily mid-market price, except for spot.

In April, the USD forward curve moved up substantially while the BTC curve moved up more modestly. May–September 2026 USD contracts rose ~17% within the trading month and ~20% through May 4. BTC contracts rose ~4% across the curve. Both curves traded predominantly in backwardation through April (spot hashprice above forward contract values going out on the curve), except for front-month contracts (May 2026) frequently trading in contango. The magnitude of the USD contract repricing (~20% in 30 days) was driven almost entirely by BTC price strength feeding into USD hashprice expectations.

Dividing USD contract values by BTC contract values reveals implied BTC price expectations embedded in the forward hashrate market. Implied BTC price expectations rose ~16% on average in April, tracking spot's recovery. This forward curve traded in mild contango (implied BTC prices rising further out), suggesting the market expects continued BTC recovery through September 2026.

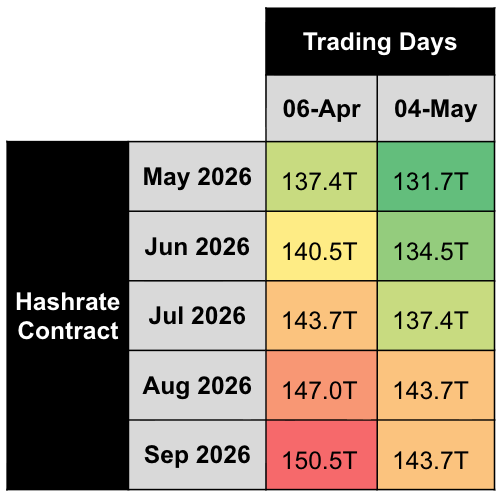

Assuming 0.018 BTC per block in transaction fees, we can also back out implied difficulty and network hashrate expectations:

Note: figures assume 0.018 BTC per block transaction fee collection on April 6 and May 4, 2026.

Based on this analysis, the forward market priced in an average ~4% decrease in difficulty and hashrate expectations for the May–September 2026 period during April 2026. The combination of upward-revised implied BTC price and downward-revised implied difficulty is informative: the forward market is treating April's BTC rally as a hashprice tailwind without expecting it to immediately bring marginal hashrate capacity back online.

Concluding Thoughts and Looking Ahead

As of early May, BTC has held around $80,000 and USD hashprice is hovering around ~$39 per PH/s/day. After two months of all-time lows, mining economics have rebounded modestly, but the key characteristic of the coming months will be uncertainty across BTC price, network difficulty, and transaction fees.

On BTC price: April 2026 was one of the strongest months for U.S. equities in nearly six years, and BTC participated. Was April a dead-cat bounce within a developing bear market? A new leg up reclaiming the cycle? Or the start of a range-bound consolidation between $65,000 and $85,000? Each scenario has different implications for hashprice. The Deribit option chain at the longest-dated quarterly expiry (March 26, 2027) puts risk-neutral odds at roughly 38% bear (BTC < $65K), 23% consolidation ($65K–$85K), 28% partial recovery ($85K–$126K), and 11% new all-time high. This implies roughly 6-in-10 odds that BTC is at or below current levels by next March.

On network difficulty: the May 2 adjustment (−2.30%) just put difficulty back near the March 20 epoch at 132.47T, extending the sub-1-ZH streak to four consecutive epochs across 43 days. Marginal hashrate that came offline at $30 hashprice hasn't returned even with hashprice now back near $40. The next adjustment, expected mid-May, will tell us whether more marginal hashrate is still rolling off (and whether the network is finding equilibrium below 1 ZH/s) or whether new-gen deployments will reassert difficulty growth into Q3.

On transaction fees: fees have remained subdued, ranging from 0.017–0.031 BTC per block and contributing less than 1% of total block rewards for ten consecutive months since July 2025. A meaningful revival in mempool activity would change miner economics.

Against this uncertainty, hashrate market participants can look to the forward market.

The Case for Hedging Hashrate

USD hashprice has rebounded from all-time lows, but for miners with thin margins, the core risk is a reversal: BTC price retreating and the recent recovery proving to be a dead-cat bounce. Selling forward now converts uncertain revenue into predictable cash flow at meaningfully higher hashprice levels. Hashrate Index’s latest mining economics projections base case scenario (Q2 2026) estimates USD hashprice sensitivity to BTC prices as follows:

Note: figures reflect equilibrium hashprice levels after the network's marginal hashrate has adjusted to each BTC price scenario. Short-term hashprice readings during a price move can deviate meaningfully from these equilibrium values until difficulty resets bring the network into a new steady state.

The Case for Financing With Hashrate

The same forward market that protects sellers can serve as financing for fleet upgrades. By selling hashrate and receiving upfront payment, miners can fund capital expenditure without equity dilution or debt.

An S21 operator at $0.05/kWh has a hashcost of $21.00, below current spot. An S19j Pro operator at the same power cost faces a hashcost of $35.40, at the upper end of the forward curve and pushing into negative-margin territory if hashprice retraces. Upgrading from the S19j Pro to the S21 cuts hashcost from $35.40 to $21.00 — an immediate $14.40 per PH/s/day improvement.

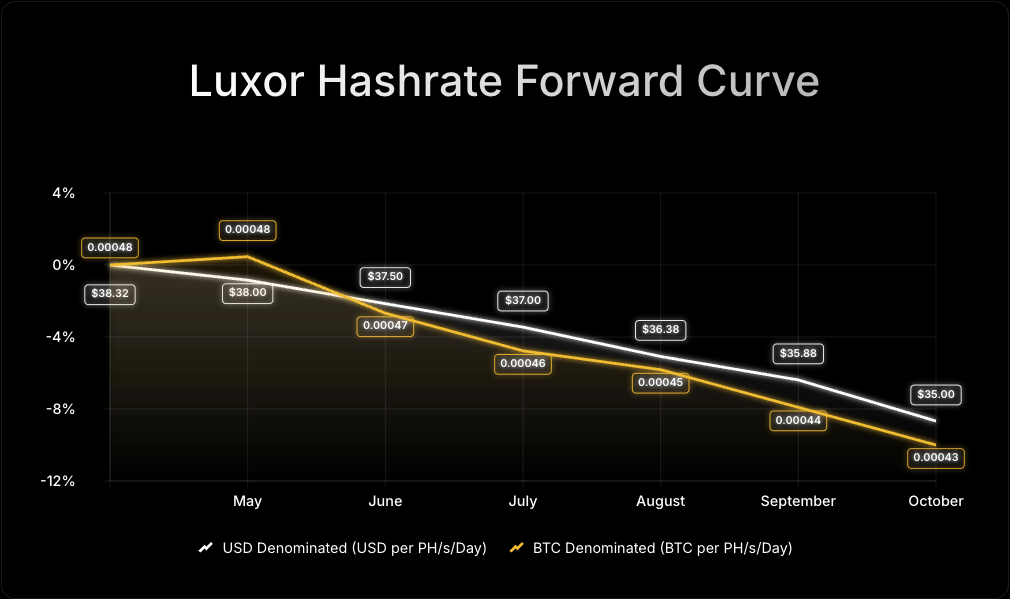

Looking Ahead

Looking forward, Luxor's Hashrate Forward Market is pricing in an average hashprice of $36.63 or 0.00045 BTC per PH/s/day over the next six months. Sellers can currently secure this hashprice while buyers have the opportunity to lock in the same hashcost through October 2026.

If you’d like to learn more about Luxor’s Bitcoin mining derivatives, please reach out to [email protected] or visit https://www.luxor.tech/derivatives.

About Luxor Technology Corporation

Luxor delivers hardware, software, and financial services that power the global compute and energy industry. Its product suite spans Bitcoin Mining Pools, ASIC Firmware, Hardware trading, Hashrate Derivatives, Energy services, a Miner Management software, Commander, and a bitcoin mining data platform, Hashrate Index.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}