Two Years Into the 2024 Halving: The Hashprice Regime Change

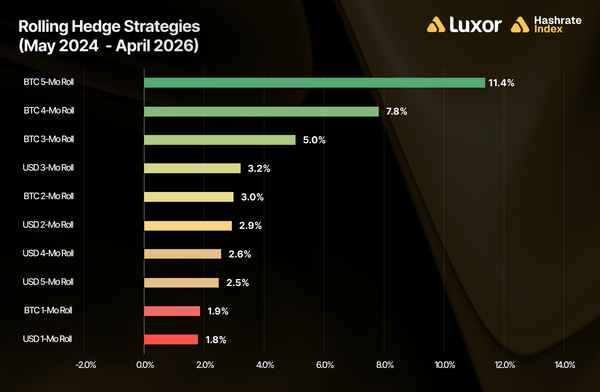

Across both years, every rolling hedge strategy beat spot (FPPS) mining.

TLDR

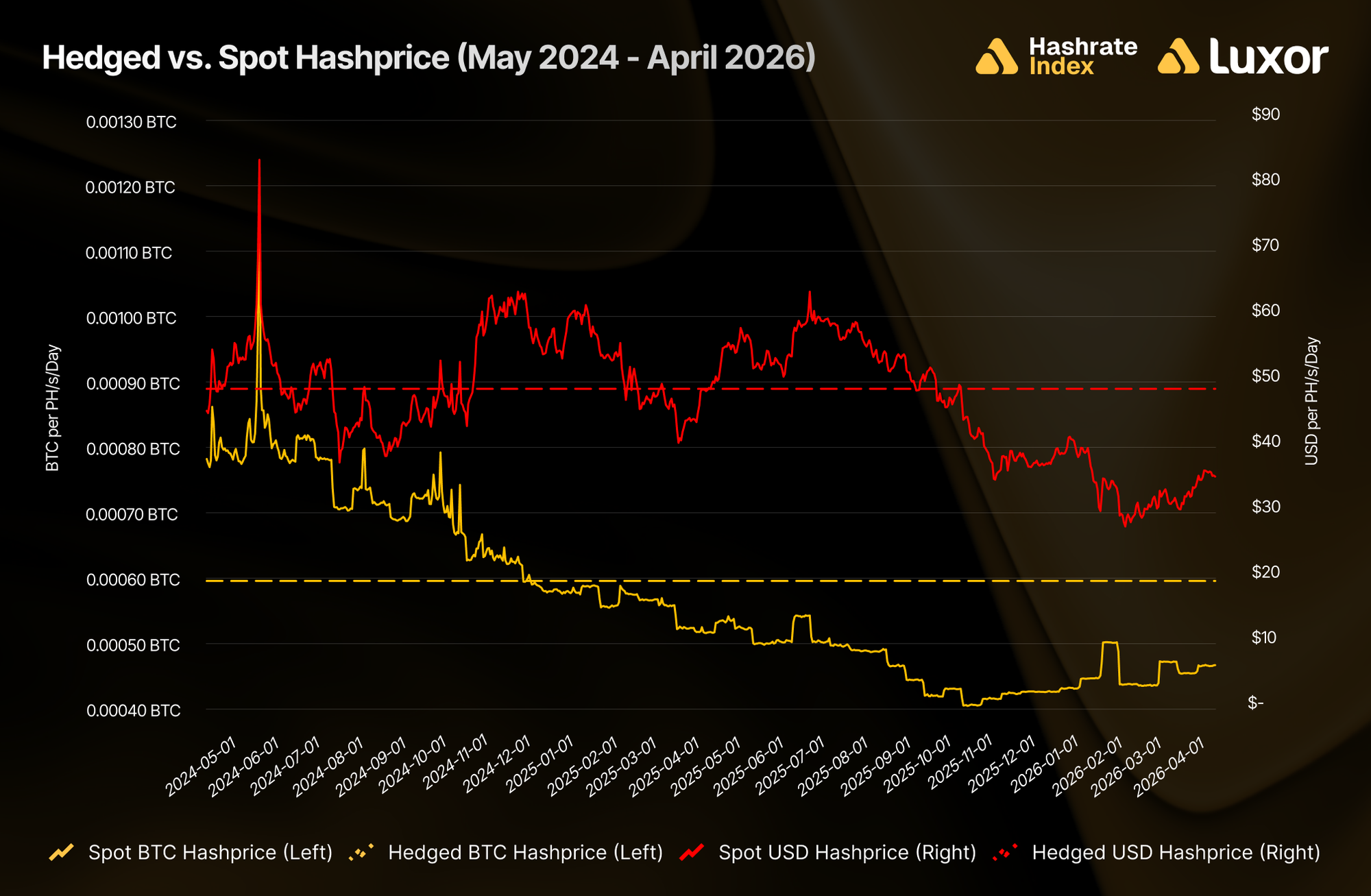

- Two years have elapsed since the April 2024 halving. Looking back on this period reveals two distinct hashprice regimes, and how different rolling hashrate hedging strategies performed across each. Overall, any rolling hedge strategy (regardless of contract duration or denomination) since the 2024 halving outperformed spot (FPPS) mining.

- Two-year post-halving period (May 2024–April 2026): BTC-denominated hedges stood out over the past two years. This was due to network difficulty growth and low transaction fees beyond expectations. The BTC-denominated 5-month rolling hedge strategy led since the halving at +11.4% vs. spot. For a 1 EH/s operation, that’s approximately 47.5 additional BTC on identical hardware over 24 months.

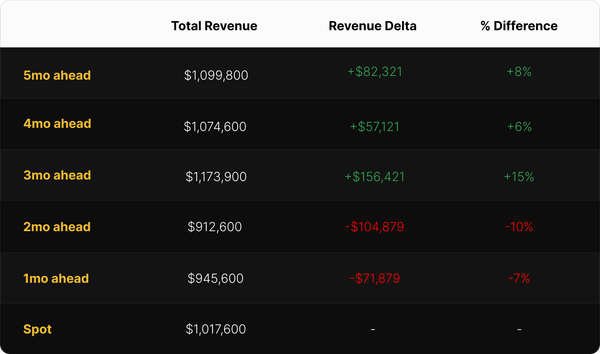

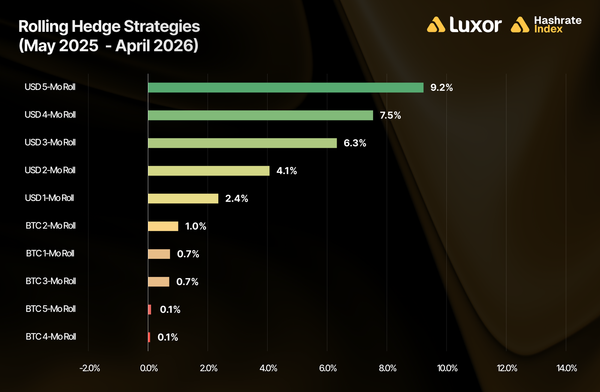

- Trailing-twelve-month period (May 2025–April 2026): The picture looks completely different over the past year. USD-denominated hedges meaningfully outperformed spot mining, whereas BTC-denominated hedges clustered near flat (+0.1% to +1.0%). The USD-denominated 5-month rolling hedge strategy led over the past year at +9.2% vs. spot. For a 1 EH/s operation, that’s approximately $1.5M additional revenue on identical hardware over 12 months.

- The hashprice regime shifted. From May 2024 through approximately Q4 2025, relentless network difficulty growth and low fees made BTC-denominated hedges the winning play. From late 2025 onward, BTC price uncertainty and a decline in difficulty made USD-denominated hedges the winning play.

The Two-Year Trend

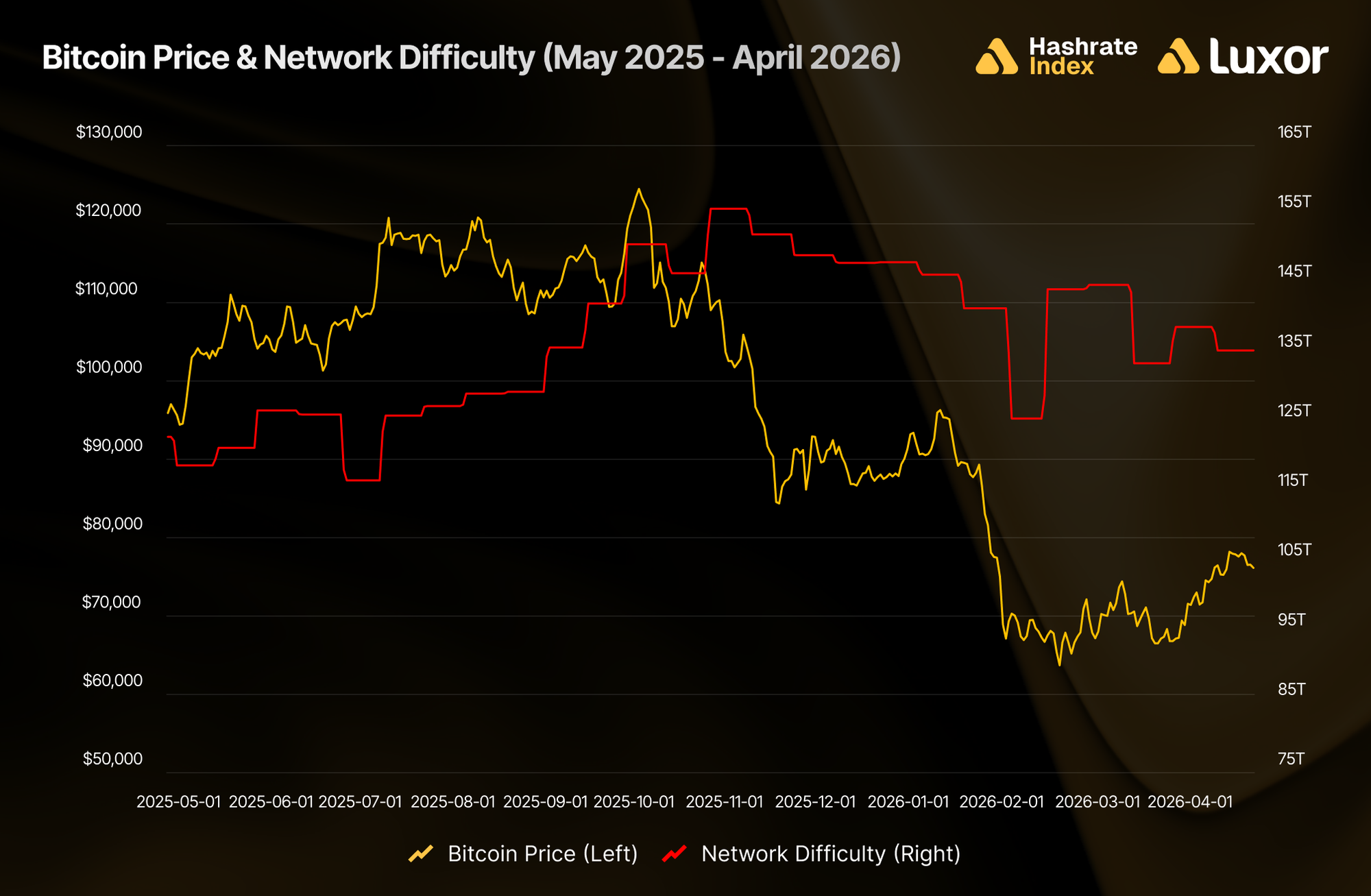

The April 2024 halving landed at block 840,000, reducing Bitcoin block subsidies from 6.25 BTC to 3.125 BTC and permanently compressing BTC-denominated hashprice. Two years on by the end of April 2026, mining economics look different than when the subsidy shock was initially absorbed.

There is a useful coincidence at this time. The trailing twelve months (May 2025–April 2026) cover Year 2 of the halving epoch, while “since the halving” (May 2024–April 2026) covers the full 24-month period. This means we can directly compare Year 1 vs. Year 2. The contrast is telling.

Year 1 (May 2024–April 2025) of the post-halving period was defined by relentless difficulty growth, low transaction fees, and a rising BTC price. Year 2 (May 2025–April 2026) was defined by BTC’s ~45% drawdown from its October 2025 cycle peak of ~$126,000, difficulty stagnation (then contraction), and historically compressed USD hashprice. Each period posed a different hashprice environment, but hedgers came out on top regardless.

Note: The hedged hashprices shown are illustrative, and based on the average mid-market rate from forward contracts listed on Luxor’s order book between May 1, 2024 and April 30, 2026 (excluding intra-month contracts).

Market Dynamics

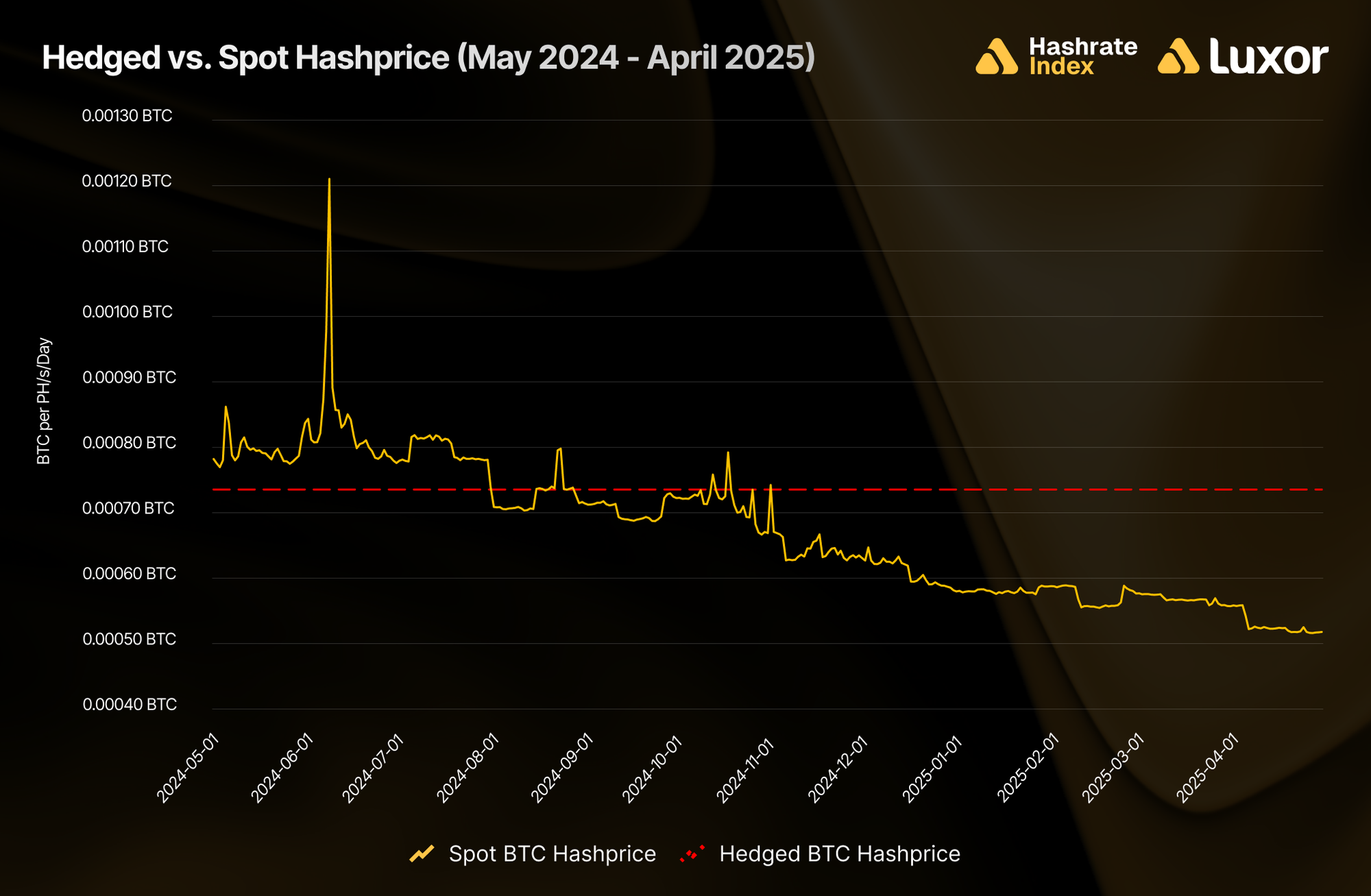

Year 1: May 2024 – April 2025 — The Difficulty Grind

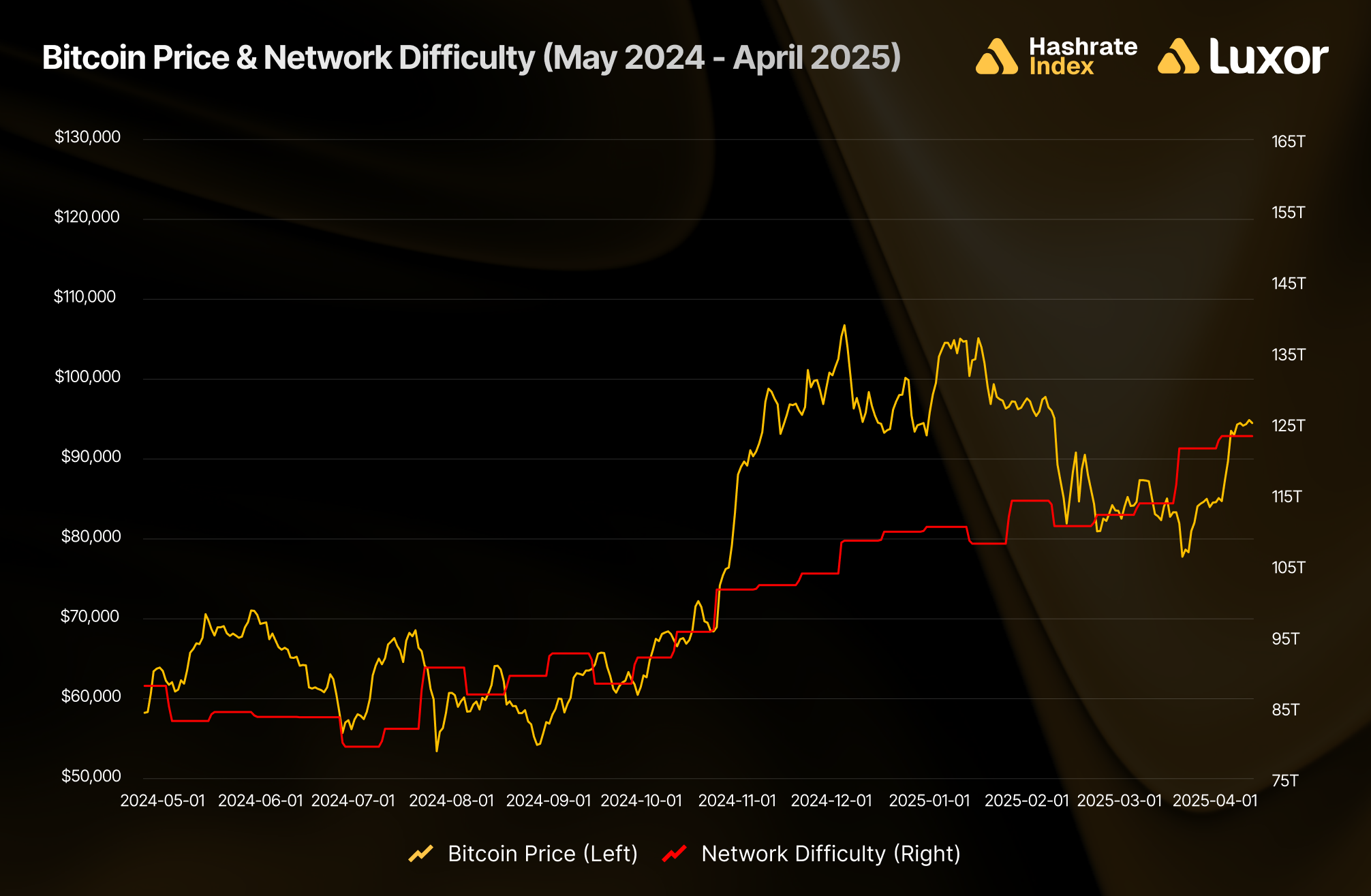

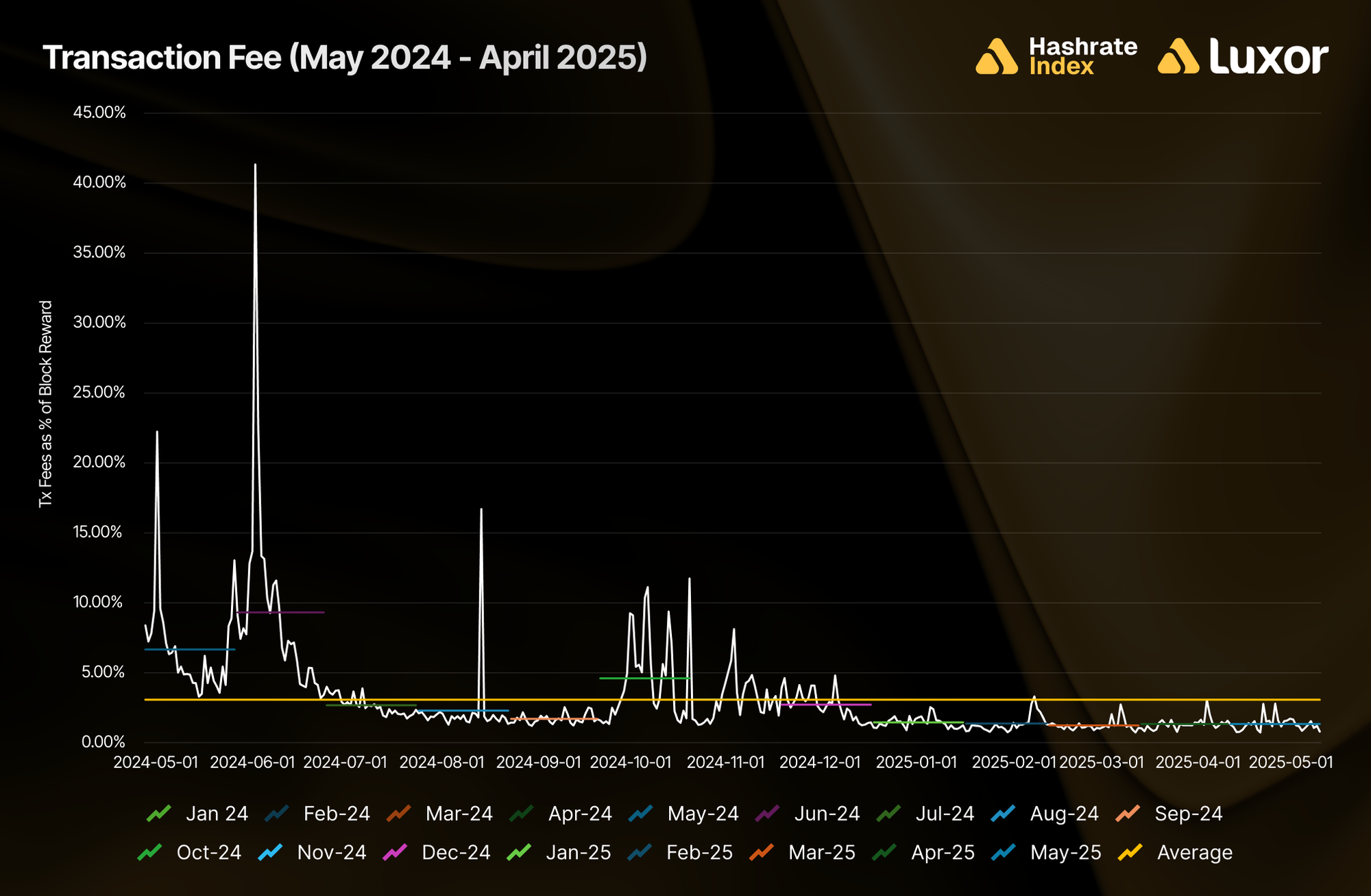

The first year after the halving was a difficulty surge beyond expectations. New-generation hardware was deployed at scale, network hashrate climbed steadily, and difficulty rose faster than most forward hashrate contracts had priced in. BTC price was broadly supportive through this period, though volatile. Transaction fees, briefly elevated around the halving, quickly faded back below 1% of block rewards and stayed there.

For spot (FPPS) miners, this dynamic was punishing. Difficulty rising faster than expected meant that for every PH/s of hashrate, BTC earnings were being systematically compressed by the network. The forward hashrate curve was too optimistic in forward BTC hashprice expectations; difficulty growth kept compressing spot hashprice below forward contract hashprice rates by the time they settled.

BTC-denominated hedges captured exactly this spread: sellers locked in forward BTC hashprice rates before incoming difficulty growth eroded spot BTC hashprice below those rates. Sellers got paid a BTC hashprice which the forward market thought was fair at the time, then watched actual spot hashprice settlement come in below that level as difficulty kept rising.

Note: The hedged hashprice shown is illustrative, and based on the average mid-market rate from BTC-denominated forward contracts listed on Luxor’s order book between May 1, 2024 and April 30, 2025 (excluding intra-month contracts).

Year 2: May 2025 – April 2026 — The BTC Price Collapse and Difficulty Decline

The second year opened with bitcoin near its October 2025 cycle peak of approximately $126,000. It closed with BTC averaging $73,057 in April 2026, following a trough where the monthly average hit $69,034 in February (a ~45% drawdown from peak). The dynamic driving hashprice compression shifted.

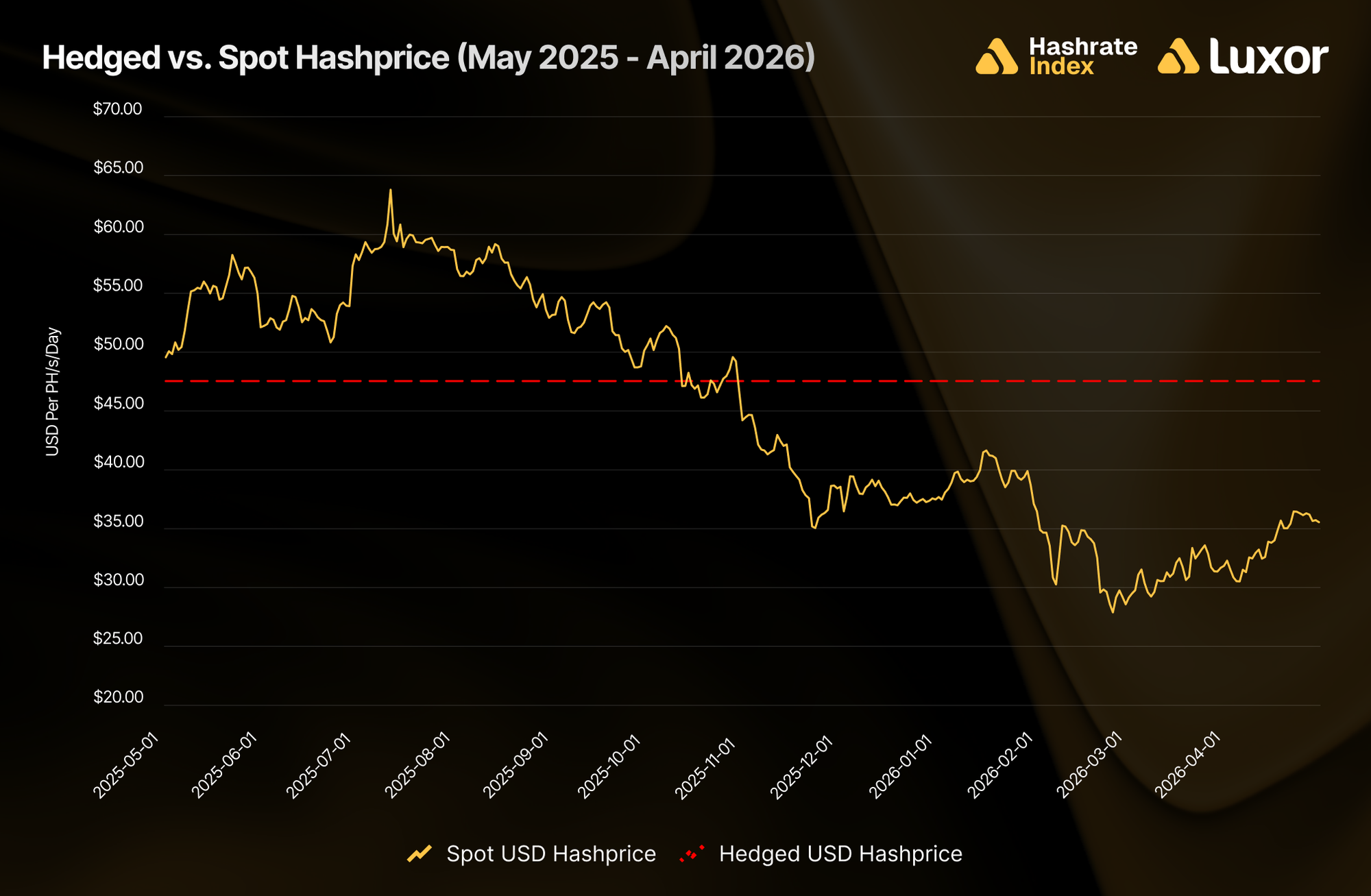

Network difficulty peaked at 155.97T in late October 2025. From there, six consecutive months of net difficulty contraction followed, driven by a combination of curtailed operations, winter weather impacts, and sustained pressure from USD hashprice all-time lows. By February 2026, monthly average USD hashprice hit an all-time low of $32.31 per PH/s/day. March extended the streak at $31.27. April broke it with an 8.5% rebound to $33.92.

In this environment, the calculus for hedging denomination flipped. BTC hashprice was actually recovering as difficulty declined; BTC-denominated forward sellers were locking in hashprice rates below where spot (FPPS) ultimately settled. But spot USD hashprice was down well below hashprice rates where forward contracts in prior months had locked in. Miners who had sold USD-denominated forwards in the November 2025–January 2026 window (when BTC was still trading above $90,000) captured premiums of 5% to 15% with hashprice rates between $35.82 and $39.13 per PH/s/day versus April 2026’s actual spot settlement of $33.92.

Note: The fixed hashprice shown is illustrative, and based on the average mid-market rate from USD-denominated forward contracts listed on Luxor’s order book between May 1, 2025 and April 30, 2026 (excluding intra-month contracts).

Hashrate Hedging Results

Since the 2024 Halving (May 2024 – April 2026)

Across the full 24-month post-halving period, BTC-denominated rolling hedges led the field. The BTC 5-month rolling hedge strategy outperformed spot by +11.4%. For a 1 EH/s operation, spot (FPPS) miners received approximately 415 BTC over 24 months; running a BTC 5-month rolling forward sale program generated approximately 463 BTC (an additional ~47.5 BTC on identical hardware, without additional capital deployed).

Trailing Twelve Months (May 2025 – April 2026)

The TTM picture is the mirror image. USD-denominated strategies led. The USD 5-month roll outperformed spot by +9.2%, while BTC 5-month and 4-month strategies barely cleared breakeven at +0.1% each.

Note: rolling hedge figures exclude fees and bid/ask spreads. Hedging is a cost of business, not a revenue generation method. Hedgers willingly pay a premium for certainty and more predictable cash flows, which increases valuation, reduces cost of capital, and attracts investment.

Understanding The Hashprice Regime Shift

The contrast between the two timeframes tells us that there has been a shift in hashprice regimes, and it points to a framework for understanding when each forward contract’s denomination outperforms.

BTC-denominated forward sales outperform when network difficulty grows faster (and/or transaction fees come in lower) than the forward market expected at the time. That’s what happened from May 2024 through Q4 2025: hashrate expanded aggressively, difficulty followed, fees fell, and spot BTC hashprice settled below forward hashprice rates across the curve. Sellers of BTC forward contracts were able to lock in a forward BTC hashprice before the network diluted it. The forward market consistently underestimated the pace of hashrate growth (and/or the dearth of fees).

USD-denominated forward sales outperform when BTC price drops faster than the forward market expected at the time. That’s what happened across Year 2: BTC fell ~45% from its cycle peak while forward USD hashprice contracts (set when BTC was trading at $90,000+) locked in hashprice rates that turned out to be well above where spot USD hashprice eventually settled.

The full 24-month window since the 2024 halving still favors BTC strategies because Year 1's difficulty-growth regime was so dominant, but Year 2 tells a different story. The narrowing spread between the two timeframes reveals the hashprice regime change in real time.

Current industry trends amplify this. With the AI/HPC transition in full swing as large publicly traded miners swap out mining hardware for GPUs, the secondary ASIC market has seen significant supply come in from operations scaling down. This structural shift in who is mining and what they’re doing with capital changes the outlook on Bitcoin’s network difficulty trajectory. The forward hashrate market is an important signal for understanding where hashprice is headed, and it has already adapted: by the end of April 2026, implied difficulty expectations in the forward curve had been revised ~4% downward for the May–September 2026 period.

What This Means for Your Mining Operation

1. Hedge Hashprice With Forward Sales

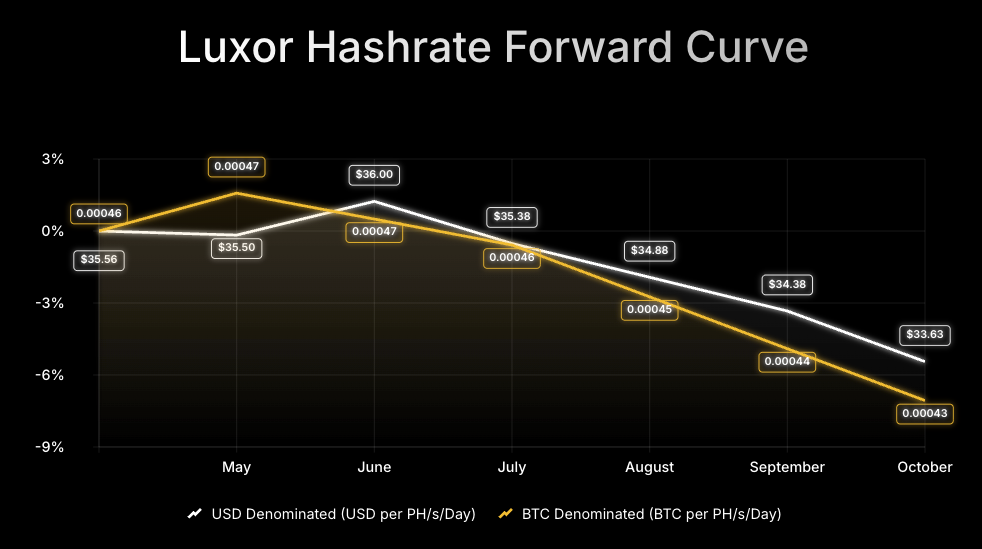

The forward curve is currently pricing May–October 2026 hashprice at an average of approximately $34.96 or 0.00045 BTC per PH/s/day. With USD hashprice having rebounded ~8.5% in April 2026 from all-time monthly lows, and BTC option markets putting roughly 6-in-10 odds on BTC being at or below current levels by March 2027, the case for locking in revenue certainty at current forward levels is clear. Selling hashrate forward on Luxor Pool converts uncertain spot hashprice exposure into predictable cash flow through your contract period.

2. Finance Fleet Upgrades With Deliverable Forwards

The cost of capital in hashrate lending markets ran at 6–13% annualized in April 2026. Miners running legacy hardware above $35 per PH/s/day in hashcost (e.g., S19j Pro operators at $0.05/kWh) can sell the Deliverable Forward (DF), receive upfront capital, and upgrade to next-generation hardware. An upgrade from the Antminer S19j Pro to the S21 cuts direct hashcost from $35.40 to $21.00 at the same power cost, an immediate $14.40/PH/s/day improvement. The deliverable forward finances the upgrade.

3. Buy Hardware While Supply Is High

The AI/HPC transition has accelerated the release of used ASICs into the secondary market at cycle-low prices. As public miners scale down bitcoin mining (SHA-256) operations in favor of AI/HPC infrastructure, the secondary market has absorbed this incoming supply. Historically, operators who bought discounted hardware at the bottom of prior cycles have obtained outsized returns. Luxor’s hardware desk is actively moving machines from $0.80/TH (used S19-series) to $11.50/TH (new S21 XP Hyd, US-landed).

*Bonus*: Lower Your Hashcost With LuxOS

At hashprice levels near all-time lows, every dollar of hashcost improvement is a dollar of margin preserved. LuxOS’ AutoTuner continuously adjusts ASIC chip frequency and voltage to minimize power consumption without sacrificing hashrate. On S21 XP hardware at $0.05/kWh, LuxOS improves hashcost by -11.4%. On S19j Pro hardware, the improvement reaches -16.9%.

Looking Ahead

The key variables for the next six months are BTC price, network difficulty, and transaction fees. The forward hashrate market is signalling on all three. As of mid-May 2026, implied BTC prices in the hashrate forward curve were in mild contango, with May–October 2026 contracts implying BTC price expectations of $79,000–$82,000. Implied difficulty expectations have been revised ~4% downward for the same period.

Looking forward, Luxor’s Hashrate Forward Market is pricing in an average hashprice of $34.96 or 0.00045 BTC per PH/s/day over the next six months. Sellers can currently secure this hashprice while buyers have the opportunity to lock in the same hashcost through October 2026.

If you’d like to learn more about Luxor’s Bitcoin mining derivatives, please reach out to [email protected] or visit luxor.tech/derivatives.

About Luxor Technology Corporation

Luxor delivers hardware, software, and financial services that power the global compute and energy industry. Its product suite spans Bitcoin Mining Pools, ASIC Firmware, Hardware trading, Hashrate Derivatives, Energy services, a Miner Management software, Commander, and a bitcoin mining data platform, Hashrate Index.

Disclaimer

This content is for informational purposes only; you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss; loss of principal is possible.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}