Halfway Across The Halving, Hedgers Outperform

Block 945,000 has hit. The scorecard says it all on fixed pool payouts and what may come next.

TLDR

- Block 945,000 was crossed: the exact midpoint between the April 2024 and 2028 halvings. 105,000 blocks gone. 105,000 blocks to go.

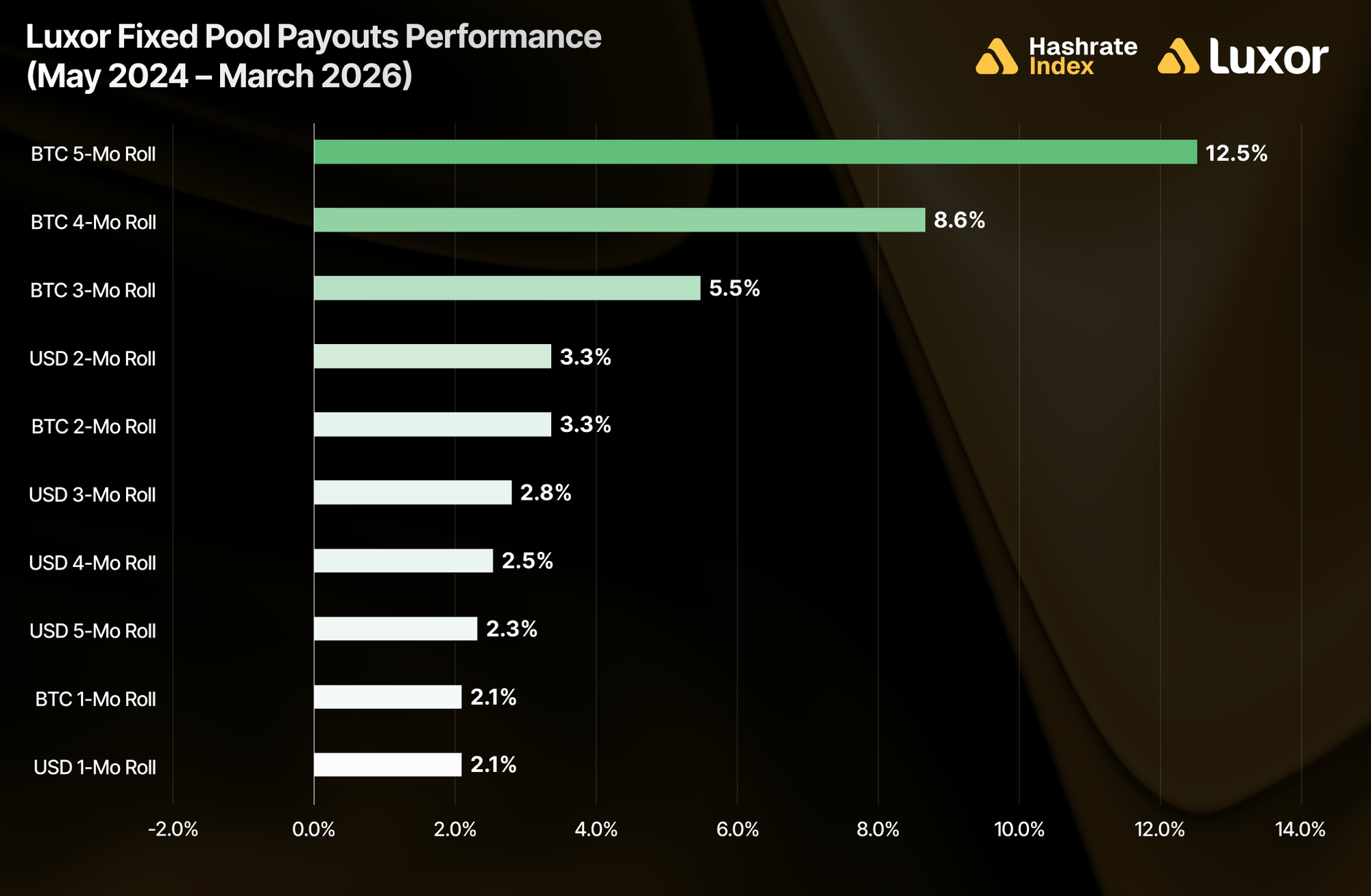

- Fixed pool payouts outperformed spot FPPS mining across the board over the first half of the halving epoch (May 2024 – March 2026), in both BTC and USD denominations.

- The BTC 5-month hedge led all strategies at +12.5% vs. spot, equivalent to an additional ~50 BTC for a 1 EH/s operation over 23 months.

- USD hashprice averaged $48.52/PH/s/day post-halving — 38% below the $78.43 average in the 21 months prior. In March 2026, it set a new monthly low of $31.27.

- The next 105,000 blocks will reward preparation, not speculation. The tools are available now: fixed and upfront pool payouts, hashrate-backed financing, buying hashrate forward, and discounted hardware.

The Midpoint

The 2024 Bitcoin halving landed at block 840,000 on April 20, 2024, reducing block subsidies from 6.25 BTC to 3.125 BTC. The 2028 halving will arrive at block 1,050,000. On April 13, 2026, the Bitcoin network crossed block 945,000.

This timing creates a natural point to reflect. Looking back, how did different mining revenue strategies perform over the first half of this halving epoch? And looking forward, given where hashprice, difficulty, and the forward market sit today, what will it take to make it through the second half?

The Structural Setup (May 2024 – March 2026)

Post-2024-halving mining economics over the first 23 months were defined by four forces:

- The block subsidy cut. The deterministic 50% cut from 6.25 to 3.125 BTC permanently repriced BTC-denominated hashprice downward.

- A difficulty arc. Difficulty climbed through the first 18 months of the cycle as new-generation hardware came online, compressing spot hashprice steadily. Then in Q4 2025, the trend reversed. BTC fell 45% from its ~$126,000 October peak, winter storms triggered curtailment across North America, and Q1 2026 extended the turbulence as February and March saw Top 10 (modern ASIC era) difficulty drops. The net effect across 23 months: compressed BTC-denominated margins with partial relief.

- BTC price compression. BTC averaged $69,618 in March 2026, roughly 45% off the ~$126,000 cycle peak reached in October 2025. High volatility throughout the post-halving period made spot mining a structurally unpredictable revenue stream.

- Low-to-no transaction fees. Fee revenue has essentially been in steady decline since the halving. In March 2026, fees averaged 0.0183 BTC per block, roughly 0.58% of total block rewards.

Under spot hashprice (FPPS) conditions, miners absorbed all of the negative impacts: every difficulty adjustment, BTC price drawdown, and fee drought. Monthly average USD hashprice across the 23-month period averaged $48.52 per PH/s/day, a 38% decline from the $78.43 average in the 21 months before the halving. By March 2026, it had compressed further, hitting a new all-time monthly low of $31.27.

First Half Scorecard: Fixed Pool Payouts Outperform (May 2024 – March 2026)

Fixed pool payouts change a miner’s risk profile. Rather than absorbing full spot hashprice exposure, miners can lock in agreed-upon hashprices for future production on Luxor Pool — the world's largest and most liquid forward hashrate marketplace, with nearly $300 million in notional volume traded in 2025.

Here is how every rolling hedge strategy performed against spot mining across the first 23 months of the current halving cycle.

Every hedge strategy beat spot mining across the board, regardless of contract denomination or hedge horizon.

The contrast in magnitude is instructive. BTC-denominated strategies outperformed by a wide margin because the forward market underestimated network hashrate growth and over estimated transaction fees. Sellers locked in forward BTC hashprices before unexpected network difficulty growth eroded spot BTC hashprice. USD-denominated strategies outperformed more modestly (+2.1% to +3.3%).

For a 1 EH/s operation: spot miners accumulated approximately ~400 BTC over the 23-month period. Running a BTC 5-month rolling forward program generated approximately ~450 BTC, an additional ~50 BTC on identical hardware, and without additional capital deployment.

Note: figures exclude fees and bid/ask spreads. Hedging is a cost of business, not a revenue generation method. Hedgers willingly pay a premium for predictable cash flows, which increases valuation, reduces cost of capital, and attracts investment.

What the Second Half May Look Like

The conditions heading into the second half of this halving epoch are among the most challenging the industry has faced.

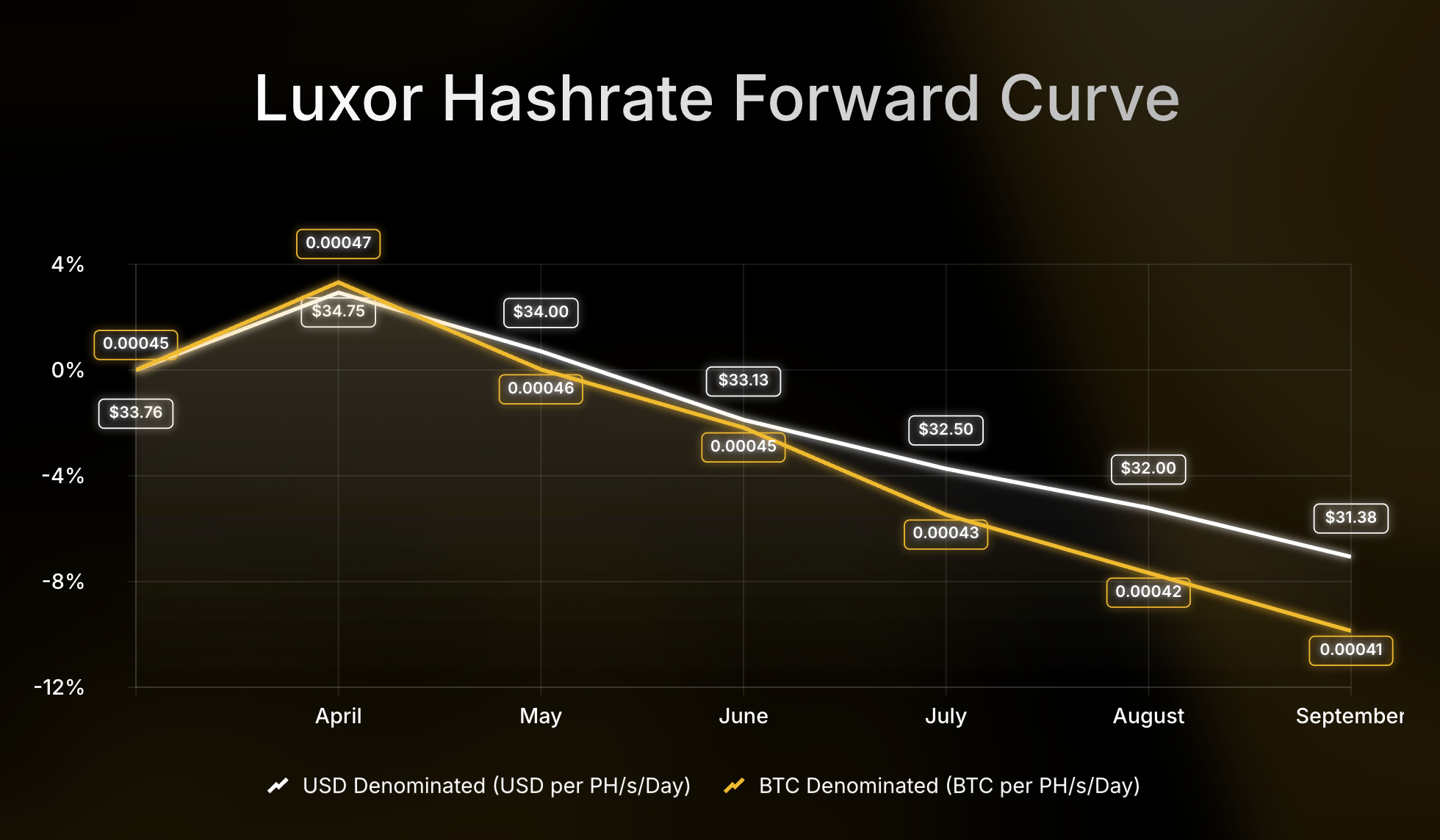

- USD hashprice near an all-time monthly low. March 2026 closed at $31.27 per PH/s/day. As of early April, the market is hovering near $32. The forward curve for April–September 2026 is pricing approximately $32 per PH/s/day or 0.00044 BTC per PH/s/day on average.

- Difficulty is adjusting. The next adjustment — estimated at around -3% on April 17 — will be the fourth downward move in five epochs, pushing difficulty further below the 145T+ levels that defined late 2025. But the mechanism driving these drops is self-correcting: each downward adjustment lifts hashprice, attracting marginal machines back in whenever above breakeven, which restores hashrate within days. For spot miners, that oscillation means short windows of relief interrupted by renewed compression each time marginal miners return.

- BTC price action remains uncertain. BTC is still ~45% below its October 2025 peak of ~$126,000, averaging $69,618 in March 2026. The forward hashrate market's implied BTC price curve fell ~5% in March and is currently sitting in mild contango; the market expects a modest recovery, but isn't pricing one with conviction.

- Fees remain structurally low. Absent a significant fee catalyst, the subsidy remains the dominant revenue input.

The second half of this cycle runs from block 945,000 to block 1,050,000. It will be defined by miners who make the moves to improve operations, reduce their cost base, and lock in revenue certainty.

The Time to Move Is Now

The first 23 months show: miners who treated SHA-256 hashrate as a risk-managed compute commodity outperformed. The tools to do this are available today.

1. Hedge Hashprice with Fixed Payouts

For operations with thin margins, the core risk is that hashprice goes lower before it recovers. Selling forward now converts uncertain revenue into predictable cash flow. Forward hashrate sales on Luxor Pool let miners monetize future production at agreed-upon hashprices today. Locking in revenue certainty now converts uncertain spot hashprice exposure into predictable cash flow for the duration of the downturn, and the upfront capital can be deployed into discounted hardware.

2. Finance Fleet Upgrades with Upfront Payouts

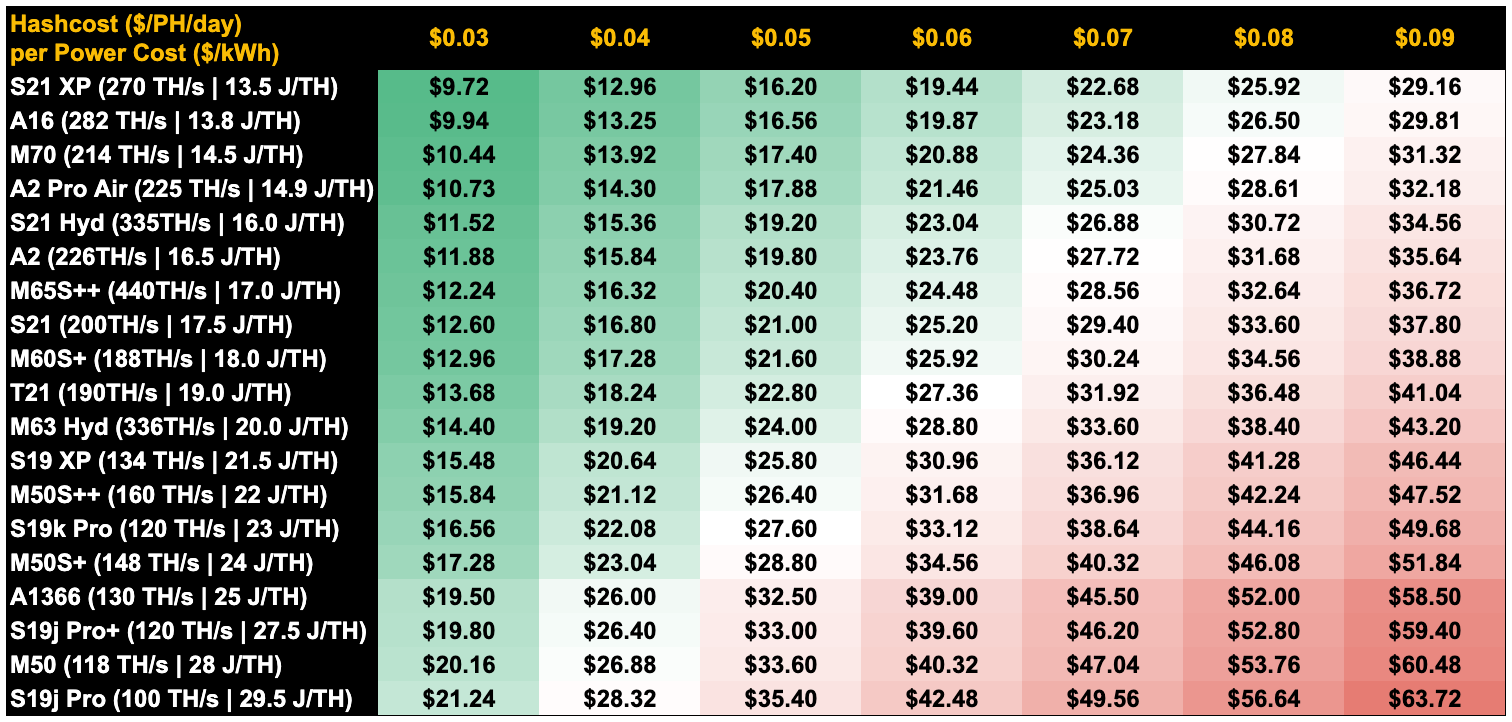

At $0.05/kWh, an S21 operator has a hashcost of $21.00, whereas an S19j Pro faces a hashcost of $35.40, well above spot and forward hashprice. Upgrading from the S19j Pro to the S21 would cut hashcost by $14.40, a significant improvement. This upgrade pays for itself quickly; the upfront pool payout provides the non-dilutive capital to execute it.

The cost of capital in hashrate lending markets ran at 6–13% (annualized) in March 2026.

3. Lower Your Hashcost By Buying Hashrate

For operators running legacy hardware above $35 per PH/s/day in hashcost, the case is clear: buy hashrate instead, directly from the forward market. At hashprice levels near all-time lows, every dollar of breakeven improvement is a dollar of margin preserved.

*Bonus* Buy Hardware While Everyone Else Is Selling

Secondary market ASIC prices track hashprice, and they're at cycle lows now. Luxor's hardware desk is currently moving the S21 XP at $8.60/TH (US-landed, OEM warranty through May 2026), as well as S19-series machines from $0.80/TH to $2.40/TH. Operators who acquire discounted hardware at the bottom of prior cycles tend to drive outsized returns, and that window for cycle-low acquisition is currently open. It won't be indefinitely.

Compounding Competitive Advantage

These strategies are not mutually exclusive — they compound.

Consider the operator who sells forward existing hashrate to fund new hardware. That operation enters the second half of this halving epoch with better efficiency, wider margins, and revenue certainty throughout the contract period. Taking a step further and turning this into a routine hedge program can then set off a flywheel effect for the miner to keep growing.

The first 105,000 blocks told the story: hashprice hedgers outperformed. The next 105,000 blocks will be written by the miners that make it through. The ones who act now.

Looking forward, Luxor's Hashrate Forward Market is pricing an average hashprice of approximately $32.96 per PH/s/day or 0.00044 BTC per PH/s/day over the next six months. Sellers can secure this hashprice today. Buyers can lock in that same hashcost through September 2026.

If you'd like to learn more about Luxor's Bitcoin mining derivatives, reach out to [email protected] or visit luxor.tech/derivatives.

About Luxor Technology Corporation

Luxor delivers hardware, software, and financial services that power the global compute and energy industry. Its product suite spans Bitcoin Mining Pools, ASIC Firmware, Hardware trading, Hashrate Derivatives, Energy services, a Miner Management software, Commander, and a bitcoin mining data platform, Hashrate Index.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}