What the Infrastructure Bill Means for Bitcoin Miners

A bi-partisan infrastructure bill includes provisions that define crypto "brokers" for taxation purposes, and miners might fit the bill's vague language if it stands.

UPDATE 8/9/21: The amended provisions did not receive unanimous consent and so the original text defining crypto brokers (in the body of the article below) was included in the final version of the senate bill. The compromise amendment was shot down when Senator Richard Shelby from Alabama objected to the compromise after Bernie Sanders (among others) rejected Shelby’s own amendment to add $50 billion in military spending to the bill. Still, the bill needs to go through the House for its own revisions (and both versions must be reconciled) before the bill becomes law, and members of the House's Blockchain Caucus have made it clear that they intend to reshape the language to make the broker definition less broad.

UPDATE 8/4/21: Senators Cynthia Lummis (R-WY), Pat Toomey (R-PA), and Ron Wyman (D-OR) have proposed an amendment to the bill's crypto provisions that could preclude miners, software and hardware developers, and protocol developers from the broker definition. The new language exempts "any person solely engaged in the business of ... validating distributed ledger transactions," a definition which would ostensibly include miners.

I’m thrilled to say that @RonWyden @CynthiaMLummis and @SenToomey have introduced an amendment to explicitly exclude validators, hardware and software wallet makers, and protocol devs from the tax reporting provisions. Bravo! Now we have to get this thing passed. pic.twitter.com/0mpyNzxXee

— Jerry Brito (@jerrybrito) August 4, 2021

UPDATE 8/6/21: Senators Warner and Portman put forth a last-minute amendment to the bill which seems to exclude miners, software developers, and hardware developers, but none of the other actors protected by the Wyden-Lummis-Toomey provision.

Wow. Sen. Warner and Portman are proposing a last minute amendment competing with the Wyden-Lummis-Toomey amendment. It is a disastrous. It only excludes proof-of-work mining. And it does nothing for software devs. Ridiculous!

— Jerry Brito (@jerrybrito) August 5, 2021

Here is all it excludes: pic.twitter.com/FA7K6NU2s0

The U.S. Congress is pushing through an infrastructure bill, and if you haven’t heard about it, it spends a few words on the cryptocurrency industry, particularly redefining the word "Broker" in the tax code to encompass Bitcoin companies in a bid to capture crypto tax revenue.

The language itself, vague and widely-encompassing, could be seen as a bit of a catch-all to include the entire Bitcoin industry--from exchanges, to wallets, to miners, and even node operators--in its scope.

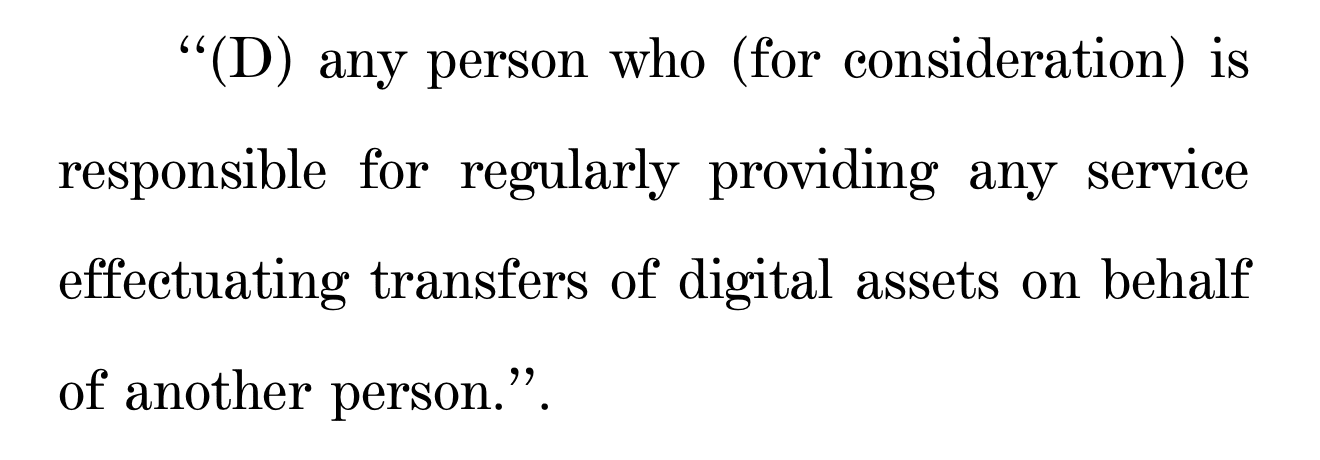

Of primary focus for the Bitcoin industry’s many players is the bill’s definition of ‘broker,’ which it deems “any person who (for consideration) is responsible for regularly providing any service effectuating the transfer of digital assets on behalf of another person.”

The excerpt in question, which vaguely defines "broker" for taxation purposes.

Put another way: any entity that oversees the transfer of cryptocurrencies from one party to another may be deemed a broker.

This obviously includes exchanges, though little surprise there. It also may include wallets (even though the wallet provider is not signing transactions for users, the software is, so the logic may go).

It also could very well include miners and mining pools themselves; seeing as they are the parties involved in ordering transactions into blocks, this could be construed as a “service effectuating the transfer of digital assets on behalf of another person.”

For its part, crypto policy think tank Coin Center is lobbying to alter the wording “on behalf of another person” to “on behalf of a customer," a small but salient change that would shift the burden of reporting only on those entities which have established a financial, fiduciary relationship with a client.

What Does the Infrastructure Bill Mean for Miners?

If the current language does apply to miners, it means they may have to report to the IRS with their customer’s KYC information, including name, address, and phone number, among other information. For mining pools, this could mean any participant in their pool; for colocation hosts, this could mean anyone hosting a rig in their facility; for brokers, this could mean anyone purchasing machines.

It remains to be seen whether or not the bill would treat mining pools with different payout methods (PPLNS vs FPPS, for e.g.) as similar or different for reporting purposes.

1/ 🚨 Here's the deal with the US infrastructure bill:

— Jake Chervinsky (@jchervinsky) July 30, 2021

A new provision has been added that expands the Tax Code's definition of "broker" to capture nearly everyone in crypto, including non-custodial actors like miners, forcing them all to KYC users.

This is not a drill 👇

It’s worth noting that a spokesperson for Senator Rob Portman (R-Ohio) told CoinDesk that the bill’s language should not extend to miners and software developers--just those entities facilitating the actual trading of cryptoassets.

“This legislative language does not redefine digital assets or cryptocurrency as a ‘security’ for tax purposes, impugn on the privacy of individual crypto holders, or force non-brokers, such as software developers and crypto miners, to comply with [Internal Revenue Service] reporting obligations. It simply clarifies that any person or entity acting as a broker by facilitating trades for clients and receiving cash, must comply with a standard information reporting obligation,” the spokesperson, Drew Nirenberg, told CoinDesk’s Nikhilesh De.

Still, it remains to be seen whether or not this expectation will hold when and if the bill passes and comes into effect. It's also worth noting that, while Congress sets the language, it's up to the Department of the Treasury to interpret it and to carry it out.

What’s the Point of Adding Crypto to the Infrastructure Bill?

The short answer: Congress needs a way to fund what is going into the rest of the bill, which they expect to cost a whopping trillion dollars (or more), so they want to milk a burgeoning crypto industry for taxation incomes.

A congressional aid delivers the 2,700 page tome to the office the Senate Amendments Desk.

Congress has estimated that crypto-specific taxation from the bill could bring in $28-30 billion over the decade, a frankly absurd figure when you consider that Coinbase, the largest exchange in the U.S., [only drummed up $1.14 billion](https://www.cnbc.com/2021/02/25/coinbase-files-for-direct-listing-after-revenue-more-than-doubles-in-2020.html#:~:text=doubled last year.-,According to the filing%2C Coinbase had net revenue of %241.14,posting a loss in 2019.) in revenue last year.

Will the Bill Pass? And If It Does, When Will It Take Effect?

The Bill is largely bipartisan and is expected to make it through the House and the Senate, but even if it does, its provisions likely won’t take effect until 2023.

It also could change still. An amendment process in the Senate began on Monday, August 2 to lobby for changes to the bill, during which period cryptocurrency advocacy groups like CoinCenter are pushing for changes.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}