Evaluating Bitcoin Mining Stocks with Enterprise Value / ASIC Value Ratio

Introducing the Enterprise Value / ASIC Value ratio, a new metric for more accurately evaluating public mining stock values.

The entire Bitcoin mining market–and the wider crypto industry–has experienced significant selloffs over the past few weeks. The liquidation spirals from Terra Luna, Celsius Network, and 3AC rekt many investors. Bitcoin miners are now liquidating coins and machines to free up capital as the bear market claws its path.

As the market sells off, investors are concerned about potential credit risks and over extended Bitcoin miner balance sheets. Recently, on Luxor’s Twitter Spaces, I spoke about the risks of collateralization on Bitcoin loans during large Bitcoin price drawdowns.

The conversation raised a question: How can investors use active mining fleet values and total debt balance on sheet debt to compare risk?

Introducing the Enterprise Value vs. ASIC Value Ratio for Bitcoin Mining Stocks

Enter the Enterprise Value vs. ASIC Value ratio (EV / ASIC Value ratio), this metric measures the value of a public bitcoin miner’s active rig fleet compared to that company’s enterprise value. The benefit of using a public miner’s enterprise value (instead of just the miner’s marketcap) is that it adjusts cash and total debt from the total market capitalization value of the company.

*To understand more about valuations using public miners’ marketcaps and ASIC values, read How to Estimate Public Bitcoin Miner Value using Price to Total ASIC ratio*

If a company is less leveraged with debt, the enterprise value will be less than their market capitalization. If the company is highly leveraged, the enterprise value will be higher, as the debt will be larger than the cash on hand.

Highly leveraged Bitcoin miners are less desirable as compared to their lower leveraged peers. Mining economics have destabilized and profitability is dropping, so investors should generally favor miners with lower leverage. A low EV-ASIC Value ratio is more desirable than a high ratio.

How to Calculate Public Mining Stock Enterprise Value and ASIC Value Ratio

To calculate the enterprise value of a public bitcoin mining stock, use the following Enterprise Value Formula:

EV = MC + Total Debt − C

Where:

MC = Market capitalization

Total debt = short-term and long-term debt

C = Cash and cash equivalents (the liquid assets of a company)

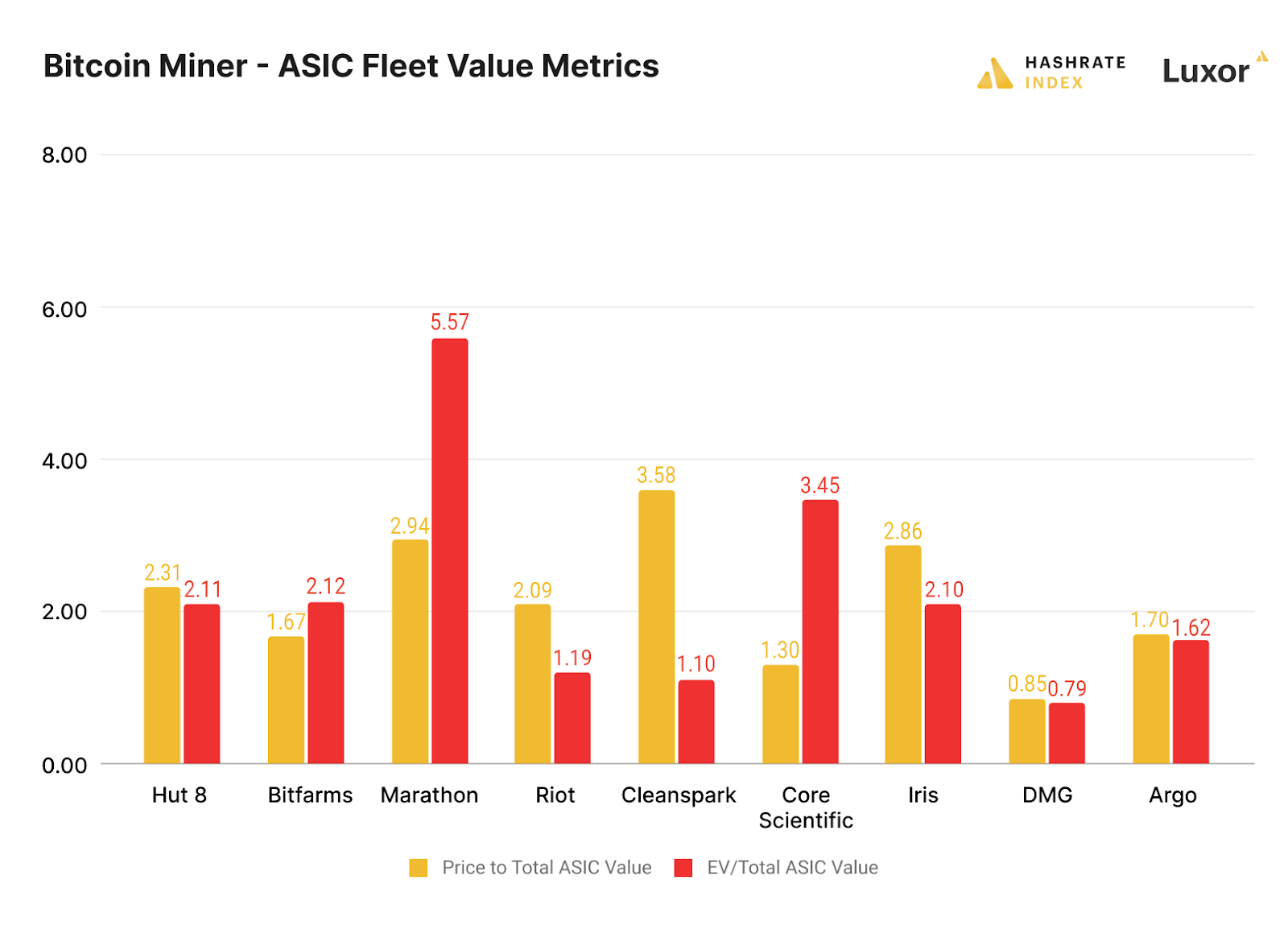

If we alter our Price / ASIC value ratio to EV / ASIC value ratio, we get a better picture of which Bitcoin mining stocks have excess debt on their balance sheets. Per the chart below, DMG Blockchain has one of the lowest ratios. As such, it looks like a bargain compared to its peers because the total value of DMG's active rig fleet is selling for cents on the dollar! Put another way, DMG has low leverage, so investors are less exposed to debt risk compared to DMG's productive hashrate (active machines).

Evaluating miners with this metric, we can see that Cleanspark, Riot, and DMG Blockchain are leading the pack in terms of EV/ASIC value. All three miners are far less levered than their Bitcoin mining stock peers. On an EV/Total ASIC ratio basis, they range within the 1.20 to 0.80 multiple factor. Investors are exposed to less potential leverage risk within these ranges. Conversely, highly leveraged mining plays like Core Scientific and Marathon Digital track to the 3.45-5.6 multiple range.

One point to add here: Marathon Digital and Core Scientific have tremendous capacity on future orders or in storage that has yet to come online. Investors are expecting an explosion in hashrate growth to benefit these miners’ EV/Total ASIC value ratio.

Benefits of using EV / ASIC Value Ratio to Evaluated Bitcoin Mining Stocks

Why use the EV/ ASIC Value ratio instead of the Price / Total ASIC Value ratio?

- Investors can glean a clearer picture of the total debt profile of a Bitcoin mining stock while also looking at public miner's active ASIC fleet (in other words, they can look at how much debt they have vs. productive assets)

- Public mining stocks that maintain a low EV / ASIC value ratio AND a low Price / ASIC value ratio means that these miners are (probably) cash heavy; they have the capital and financial wiggle room to run their businesses during bear markets and/or can be opportunistic acquiring assets at a discount

- Bitcoin miners with very high EV / Total ASIC value ratios (especially compared to their Price / ASIC value ratios) likely have less flexibility to expand or acquire assets during down markets.

Looking at the red bars for the EV / ASIC value ratio in the chart above, Marathon Digital and Core Scientific have the highest EV/Total ASIC value ratio. Both of these companies carry a sizable amount of total debt on their balance sheets; Marathon and Core Scientific raised hefty sums of capital during the bull run in their quest to expand.

Hut 8 and Bitfarms are less leveraged, as you can see in their EV / Total ASIC values, but their EV / ASIC value ratios are not quite as lean as Cleanspark, DMG and Riot. With the recent Bitcoin price drop, investors are now pricing active mining fleets under 3 times their enterprise value.

Historical Perspective on Hut 8, Riot, and Marathon with Price / ASIC Value

The benefit of history is that we can analyze the current performances of Marathon Digital, Riot, and Hut 8 mining in this bear market compared to the last one. Specifically, we can look at ASIC fleet market values starting in 2018 up until the present. Below is a chart showing the various movements in active hashrate market spot values.

* Chart shows historical ASIC fleet values based on the Price / Total ASIC Ratio, not EV / ASIC Value ratio.

During the 2019 to 2020 time period, Hut 8 owned the most Bitcoin among their peers. As you can see during the crypto winter, Hut 8 (yellow line), had the lowest ratio until the run up to bitcoin's May 2020 halving. Riot and Marathon upgraded their mining fleets during spring 2020, so the market value of their fleet went up (which lowered their Price / ASIC Value ratios), while Hut 8 was not able to upgrade their fleet (leading to a higher ratio in Q2-2020).

Fast forward to present day: you can see all three companies are neck-in-neck in valuation, as they all carry large stacks of Bitcoin in treasury and largely own new generation rig fleets.

Markets are selling away stocks en masse. As the above charts illustrate, Bitcoin miners hold great value on a relative historical basis, even when you take into consideration the Crypto Winter of 2018-2020. Nearly every publicly traded miner has a stronger balance sheet, including better operating margins than during the previous bear markets.

Rational investors who can see through the bloodbath (and keep dry powder on hand) will have the opportunity to accumulate well run Bitcoin miners at historically low valuations.

Bottom Line for the EV / ASIC Value Ratio

Investors are being given insanely low historic valuations to own public Bitcoin mining companies. Current valuations are even better than during the 2018-2020 Crypto Winter. Even when comparing current value metrics to the Q1 2020 halving bear, they seem very oversold. As long as these public miners can execute their expansions, and be stewards of their corporate treasuries; their stakeholders will be able to stick with them through a prolonged bear market within this halving cycle.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}