Luxor Hashrate Lookback Series - June 2025

June 2025’s hashrate and hashprice trends, forward market participation, trading activity and contract performance.

Luxor’s Monthly Lookback Series is a deep dive into Bitcoin hashrate market activity. In this post, we cover June 2025’s hashrate market and hashprice trends, forward market participation, trading activity and contract performance.

Summary

- Summer Slowdown: Following a recovery in May, mining economics normalized in June. USD hashprice ended down (-2.2%) and BTC hashprice slipped further (-4.4%), despite a late-month rally driven by a significant downward difficulty adjustment.

- Difficulty Bomb: Difficulty went into June at a record high, but two consecutive drops throughout the month — primarily driven by curtailment of mining operations in Texas trying to avoid 4CP charges — provided relief to miner margins. A -7.48% adjustment on June 29 marked the largest negative adjustment in magnitude since the 2021 China mining ban.

- Hashrate Hedging: BTC-denominated hedges outperformed USD hedges, especially on longer time horizons. Forward sellers benefited from maintaining BTC exposure while mitigating hashprice risk.

- Bitcoin’s Breakout: Bitcoin is breaking new ground, having just marked a new all-time high of approximately $122,000. Hashprice is back to the $60’s.

June 2025 Spot Hashprice & Its Constituents

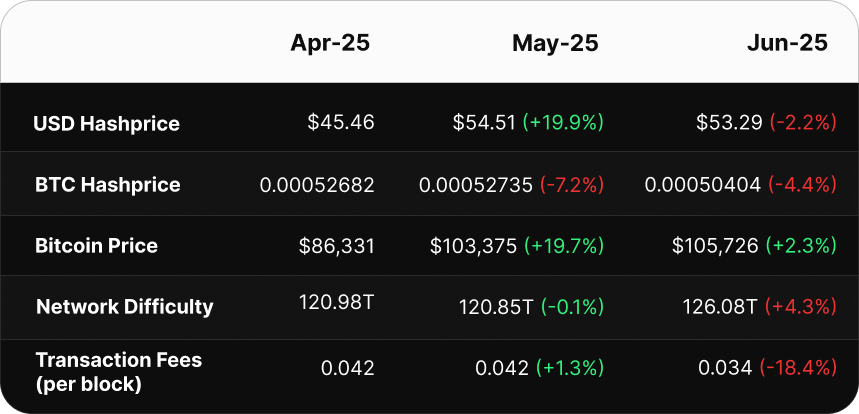

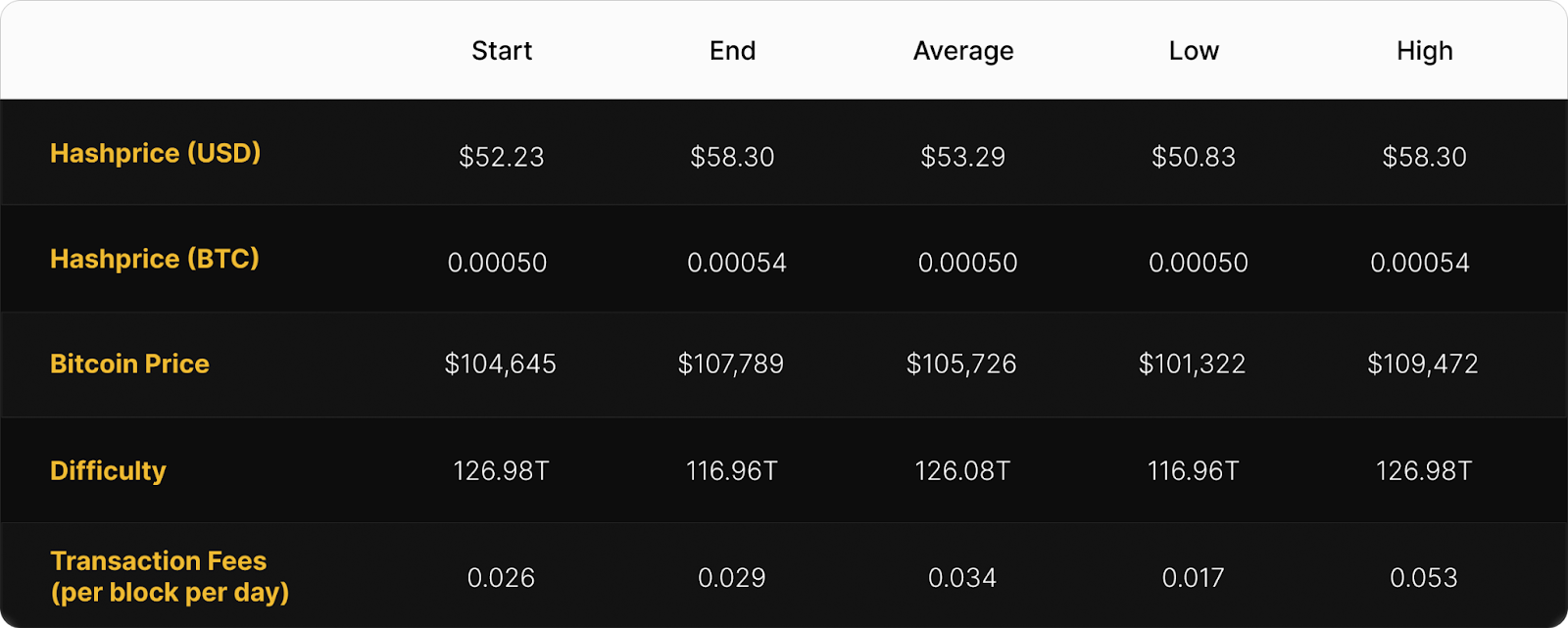

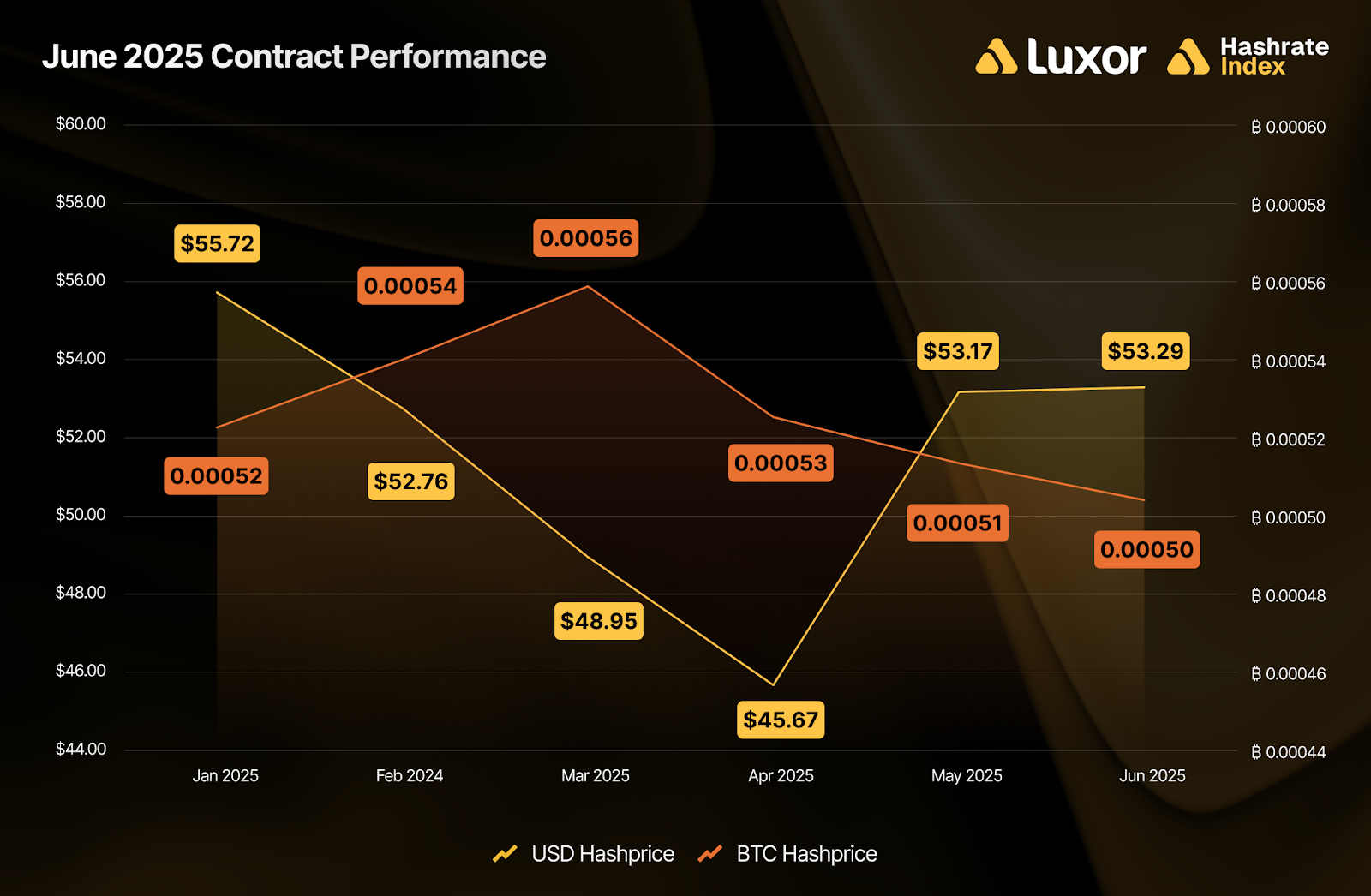

Following a recovery in May, mining economics settled down slightly in June. Bitcoin price rose modestly (+2.3%), but record-high difficulty and a drop in transaction fees (-18.4%) more than offset these gains. Overall, USD-denominated hashprice averaged $53.29 per PH/s/day (down 2.2%), whereas BTC-denominated hashprice averaged 0.00050 per PH/s/day (down 4.4%).

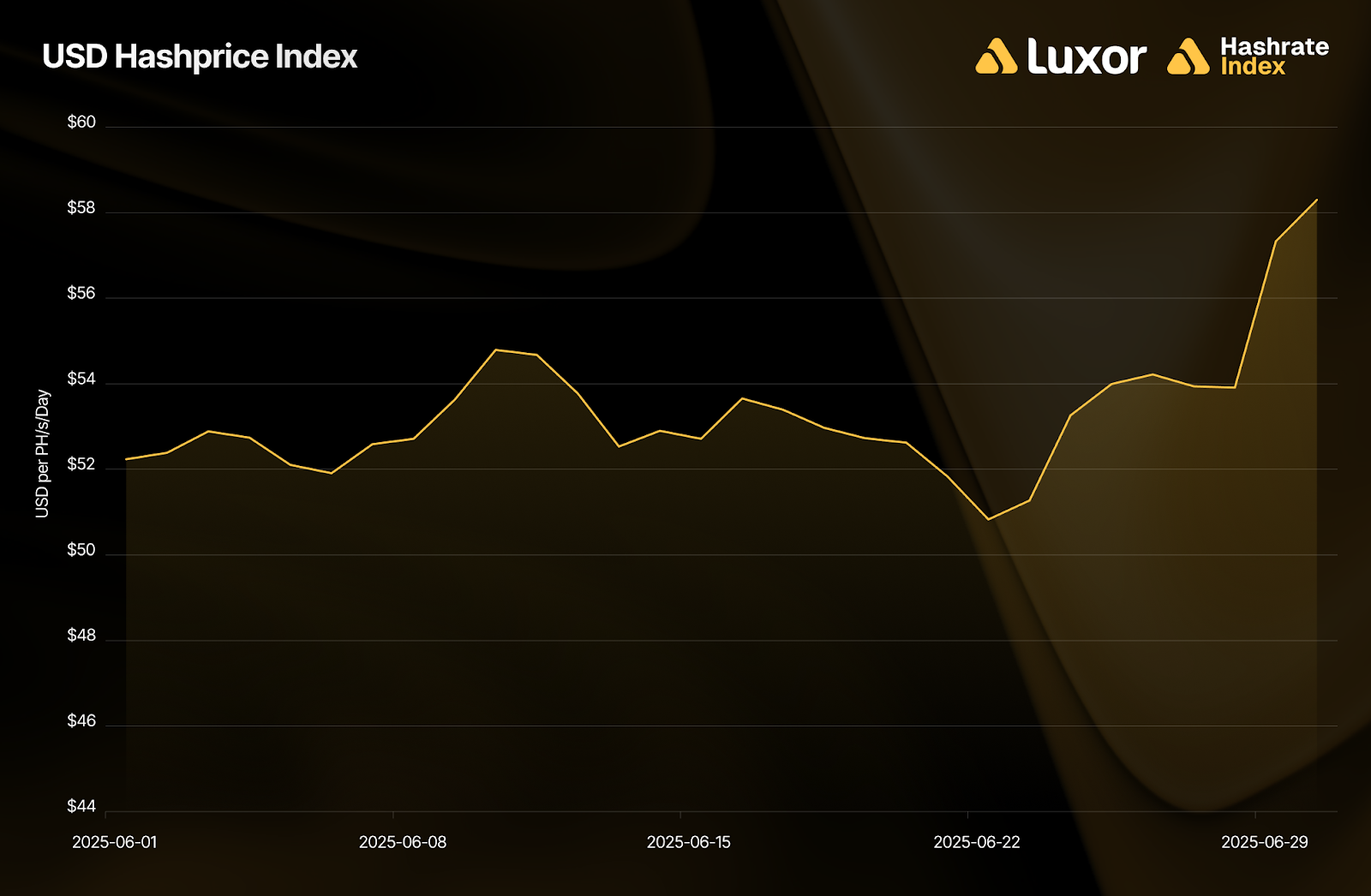

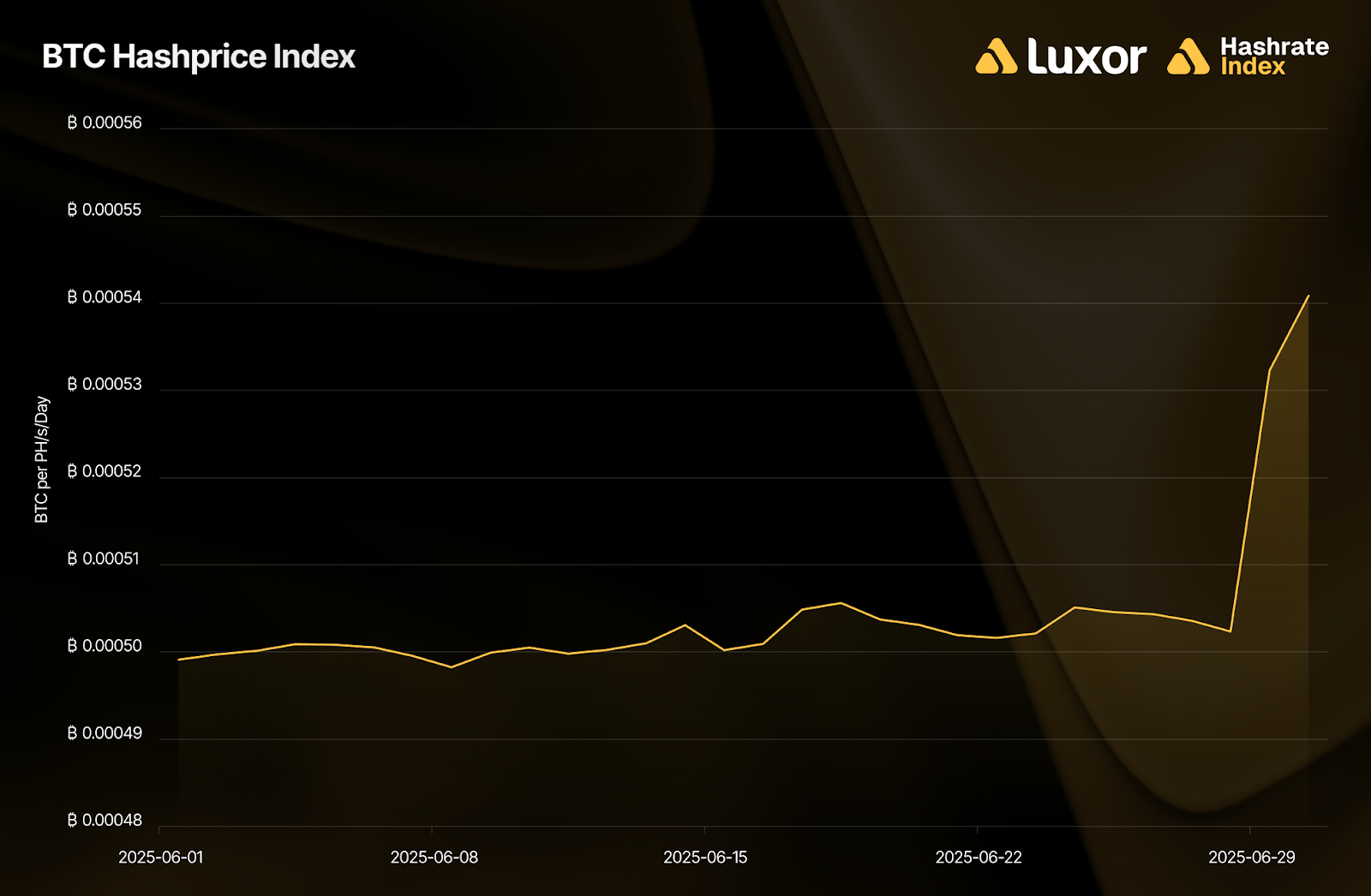

Hashprice began June at $52.23 per /PH/s/day, dipped as low as $50.83, and rallied to close the month at $58.30, following a significant downward difficulty adjustment and sustained BTC price strength.

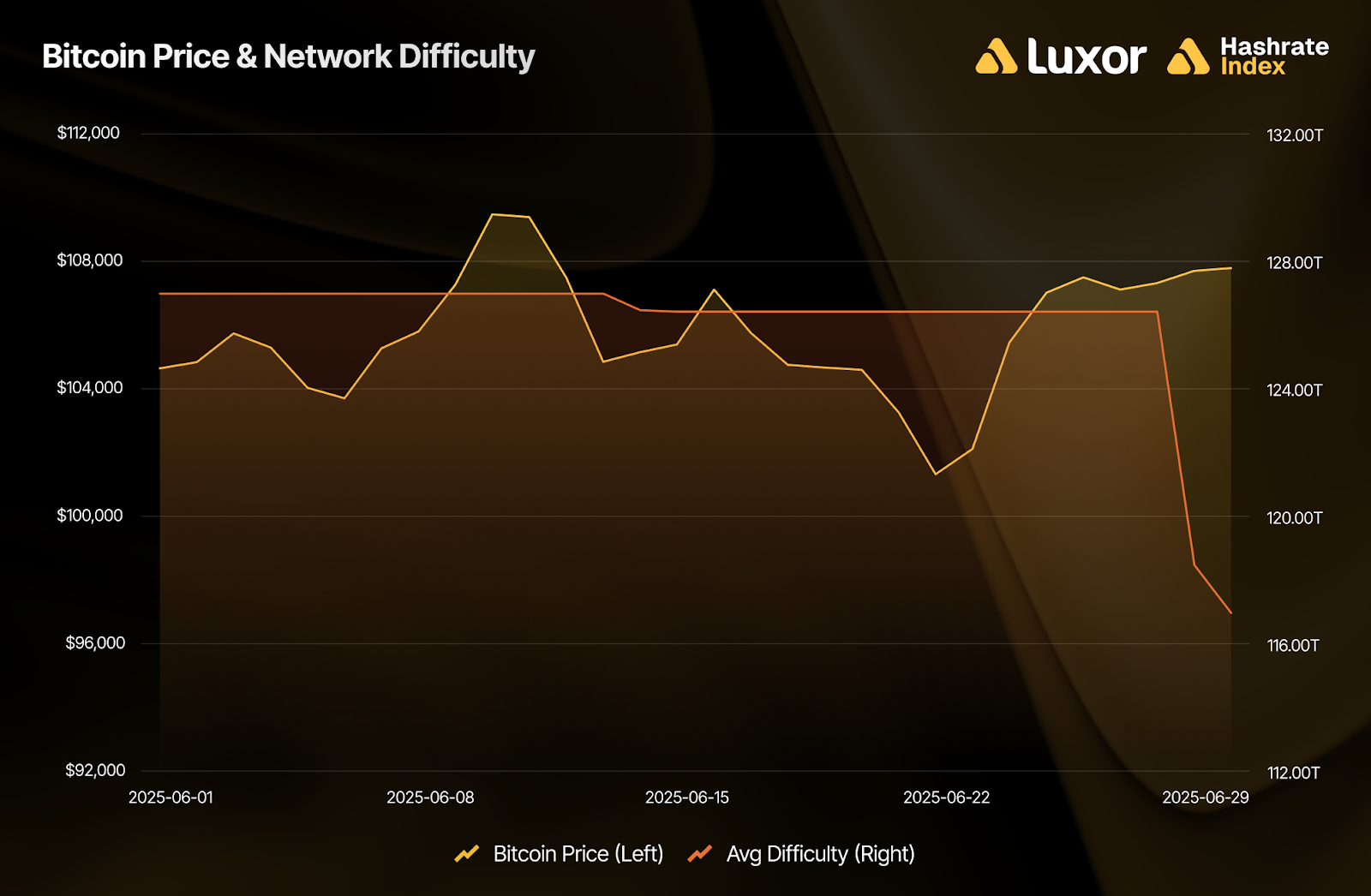

Bitcoin price averaged $105,726 throughout June. Starting at $104,645, it oscillated between $101,322 and $109,472, with a 6% rally over the final week to close the month at $107,789.

Network difficulty was the main driver of hashprice in June. A positive adjustment of +4.38% on May 30 marked a new all-time high of 126.98T heading into the month, however, seasonal hashrate fluctuations throughout the second half led to two consecutive downward adjustments — 0.45% on the 14th and a whopping 7.48% on the 29th — marking the first back-to-back negative adjustment since July 2024 and the largest negative adjustment in magnitude since the 2021 China mining ban. All in all, difficulty fell down to 116.96T by month-end.

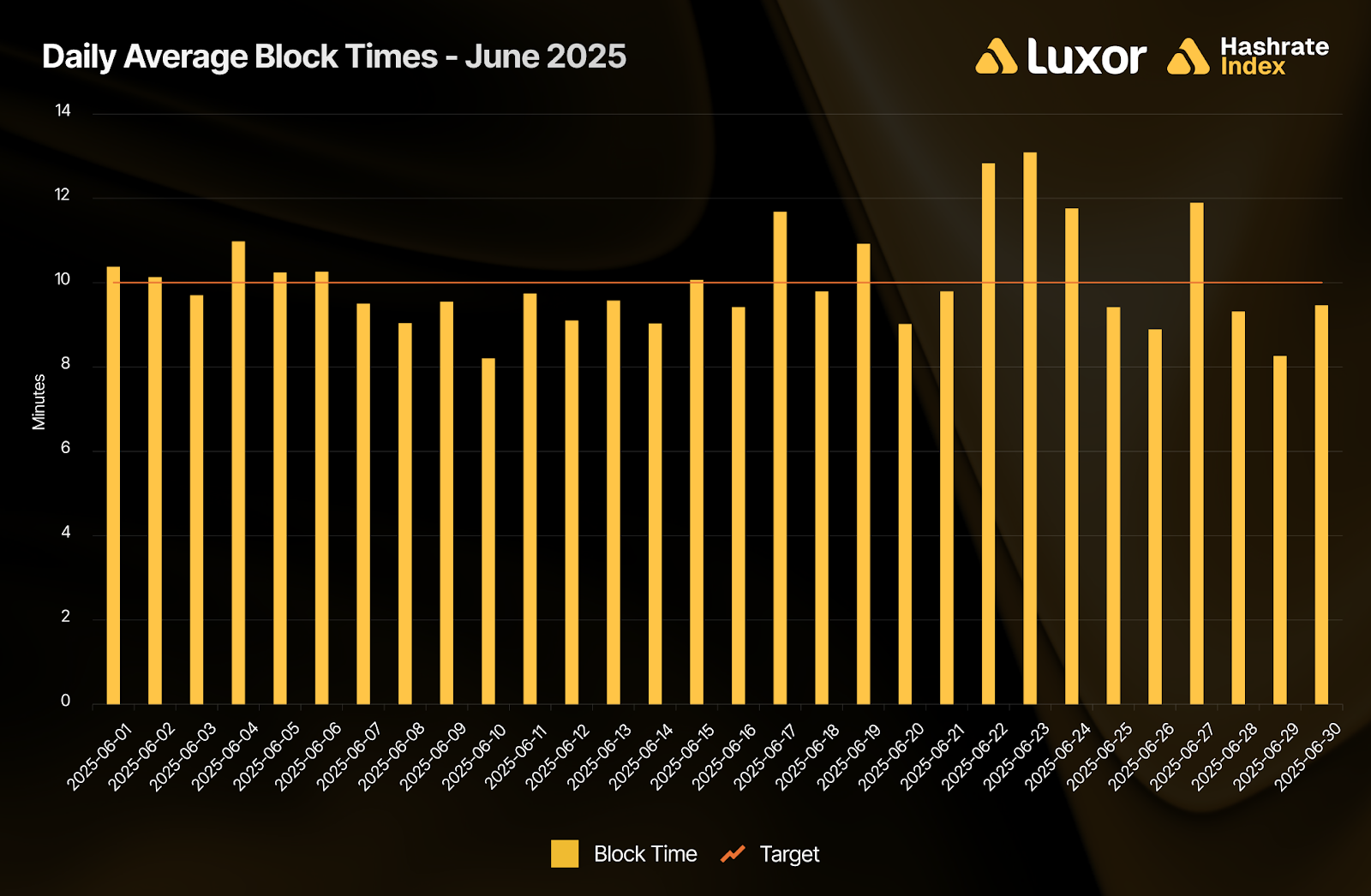

The negative adjustments were caused by multi-day stretches of elevated average block time intervals, primarily driven curtailment of mining operations in Texas trying to avoid 4CP charges (alongside a heat wave across the U.S). In fact, 12 out of 30 days for the month of June 2025 averaged block discovery times above the 10 minute target, and during our estimation of likely 4CP hours (i.e., between the hours of 18:00 - 02:00 UTC), block times averaged roughly 51 seconds slower than during non-4CP periods (as of June 30, 2025 UTC 21:00):

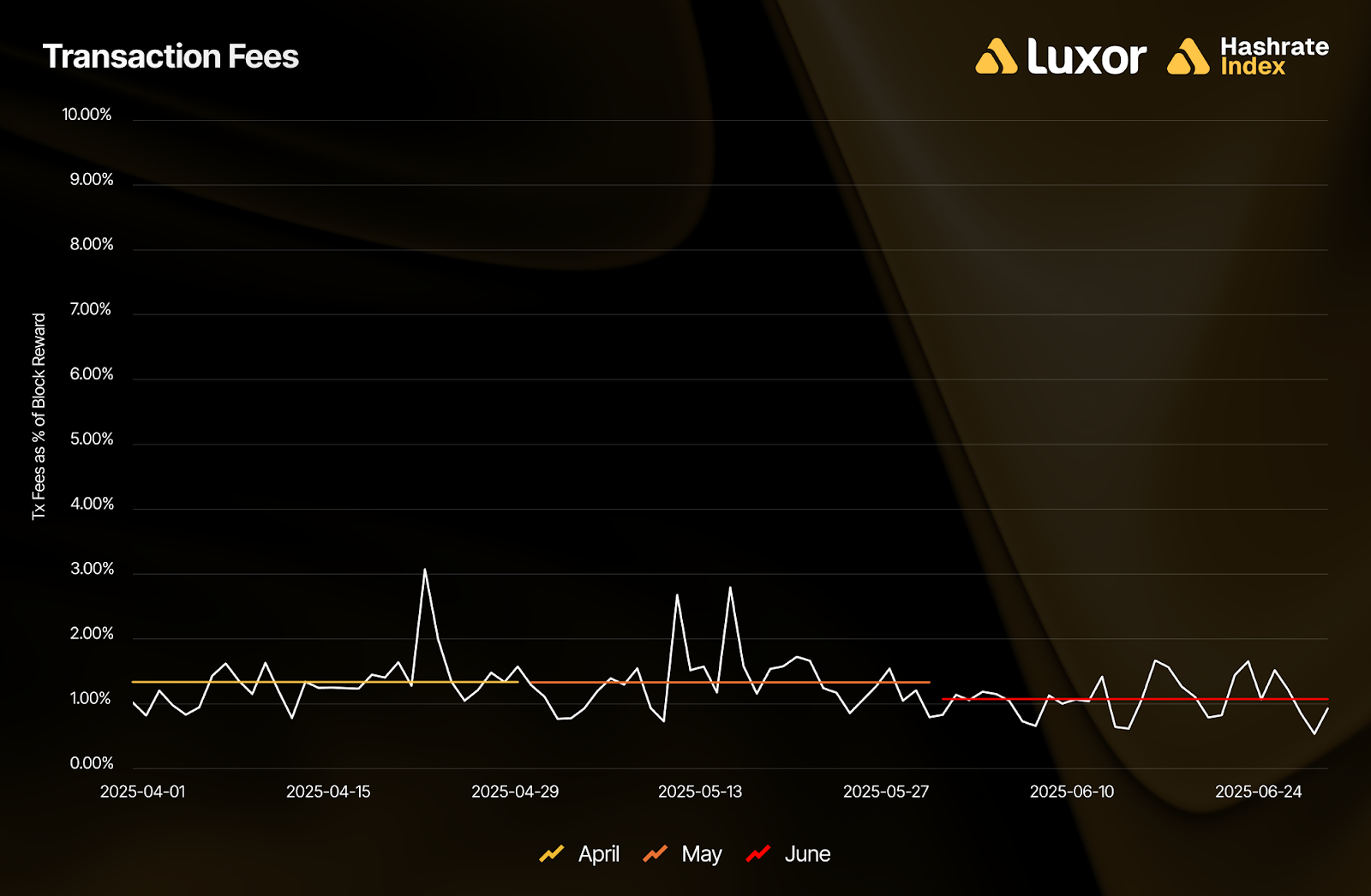

Transaction fees continued their downtrend in June, with minimal on-chain activity. On a BTC-denominated basis, miners collected an average of 0.034 BTC (per block per day), an 18.4% decline from May and the lowest since March 2012. This picture was relatively less disappointing on a USD-denominated basis, with average fee collection coming out to $3,588 versus $4,384 in May. This marks the third-lowest month in USD terms since the 2023 Ordinals surge, behind September 2024 and March 2025. Zooming out, monthly average USD-denominated fee collection has been higher than June 2025’s in 57 months and lower in 45 months since 2017; June’s average fee collection was ~62% lower than the since-2017 average.

With ever-drying fees, BTC-denominated hashprice primarily reflected network difficulty adjustments in June. It began at 0.00050 BTC per PH/s/day, edged up to 0.00051 BTC (following the initial difficulty drop), and then spiked up to end the month at 0.00054 BTC (on the back of the second difficulty drop). Despite this late uptick, BTC hashprice averaged 0.00050 BTC per PH/s/day, declining 4.4% month-over-month.

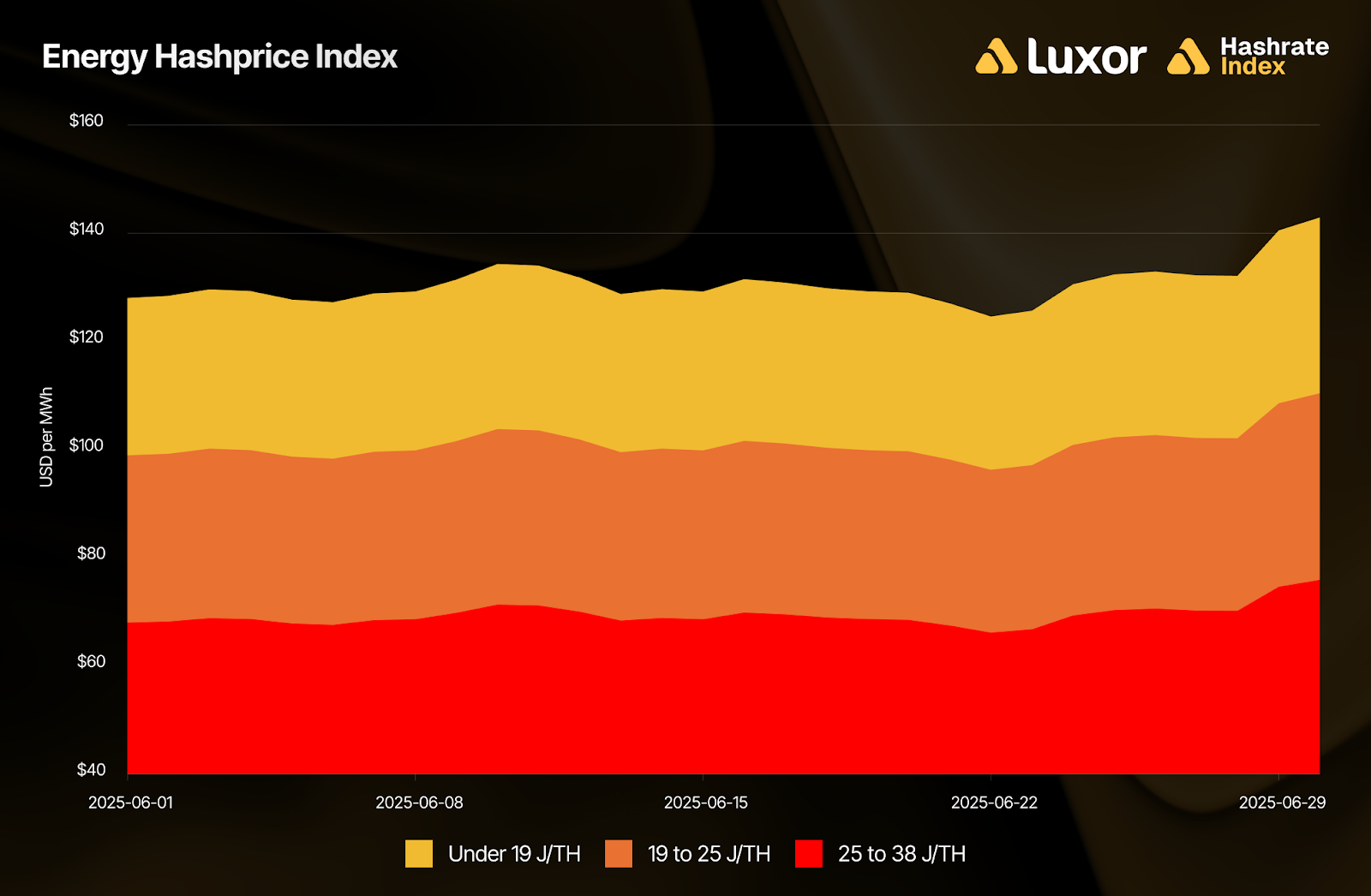

Given the tail-end uptick in hashprice, energy-adjusted mining revenues also increased toward the end of June. On a monthly average basis, operations with sub-19 J/TH fleets earned approximately $131 per MWh, whereas miners in the 19-25 J/TH and 25-38 J/TH efficiency tiers earned around $101 and $69 per MWh, respectively.

June 2025 Hashrate Market Activity

Our analysis of the June hashrate market focuses on two key points: how the June 2025 hashrate contract traded in previous months and how the forward curve shifted in June, based on pricing for forward hashrate during the month.

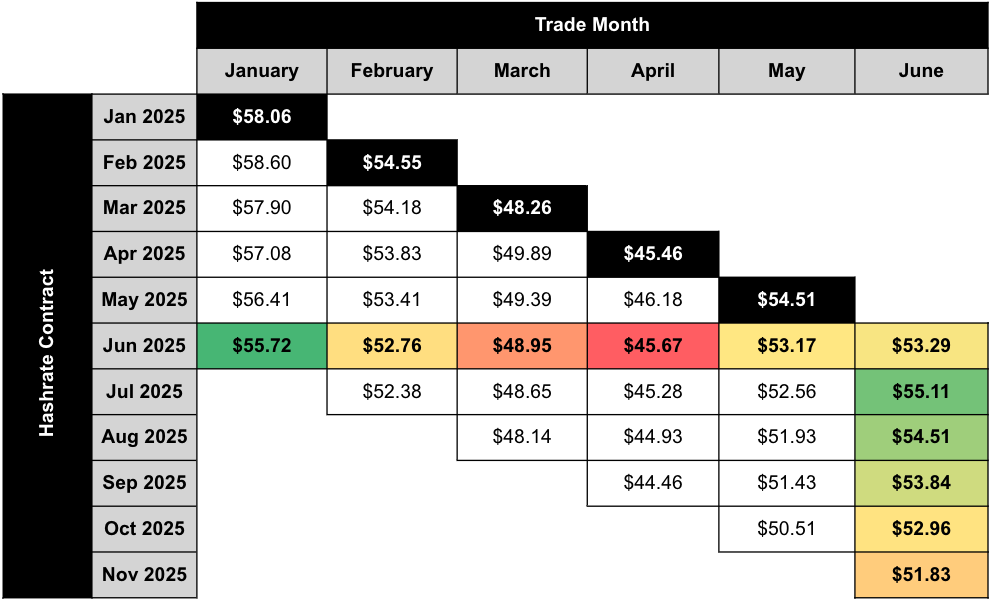

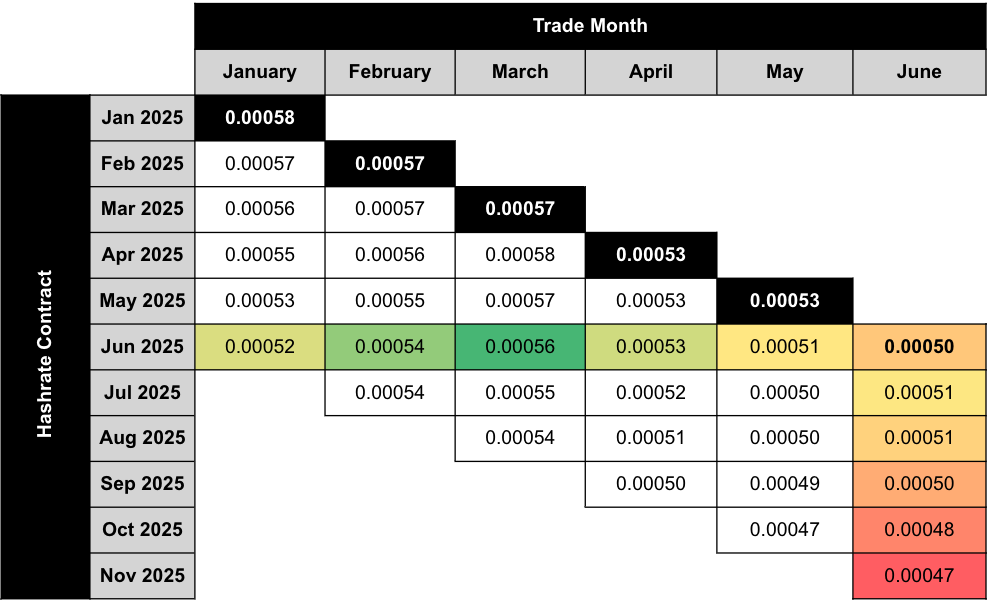

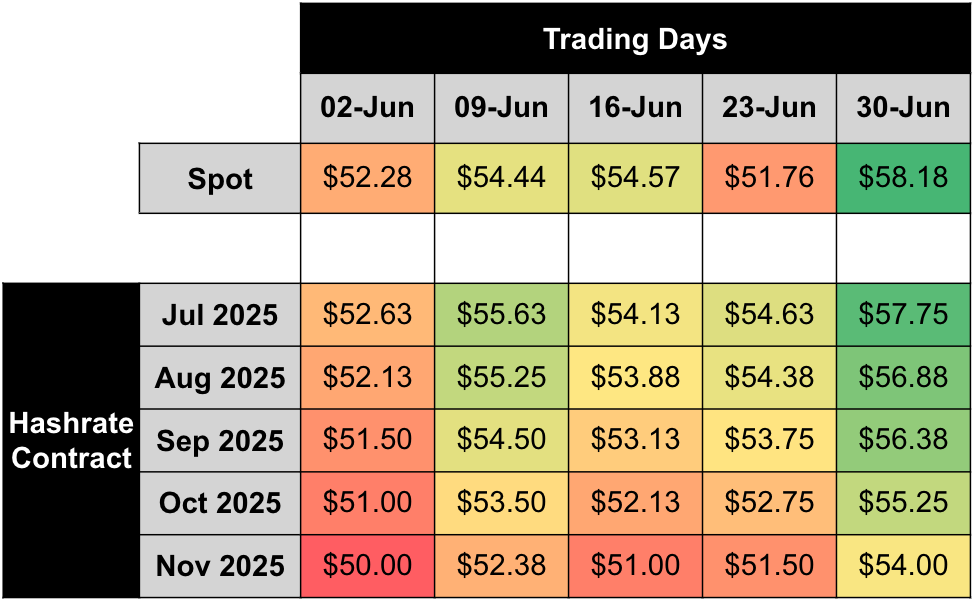

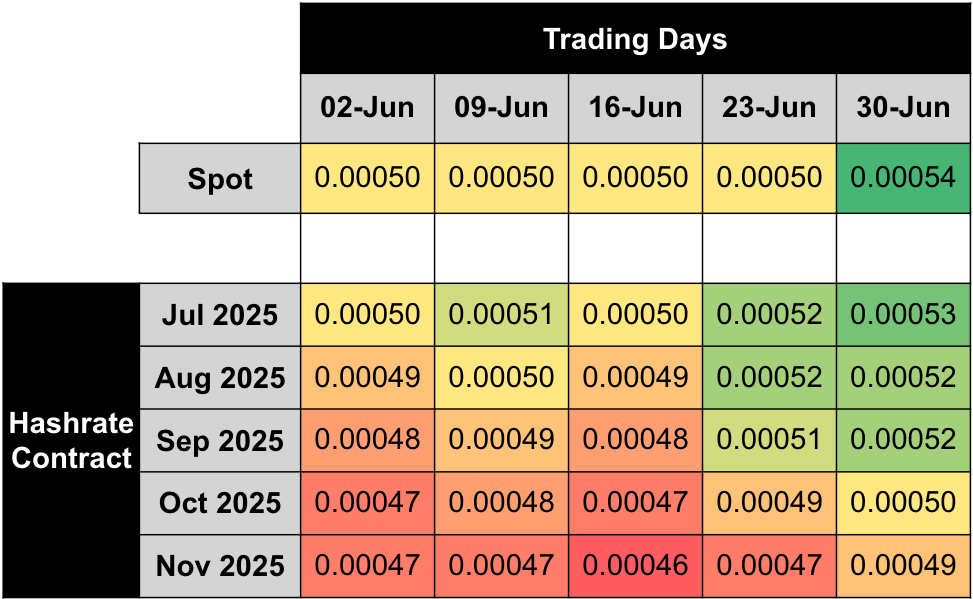

The two tables below show the evolution of USD and BTC denominated Bitcoin hashrate forward markets from January 2025 – June 2025. Rows represent specific monthly contracts, while columns represent each trading month. Cell values indicate the average monthly mid-market price — except for the bold highlighted main diagonal — which shows actual spot hashprice settlement in each month.

This table summarizes both the trading history of the June 2025 contract (colored row) and the forward curve in June (colored column).

Note: all values shown in figures represent the midpoint of the best bid and ask on Luxor's Non-Deliverable Hashprice Forward market.

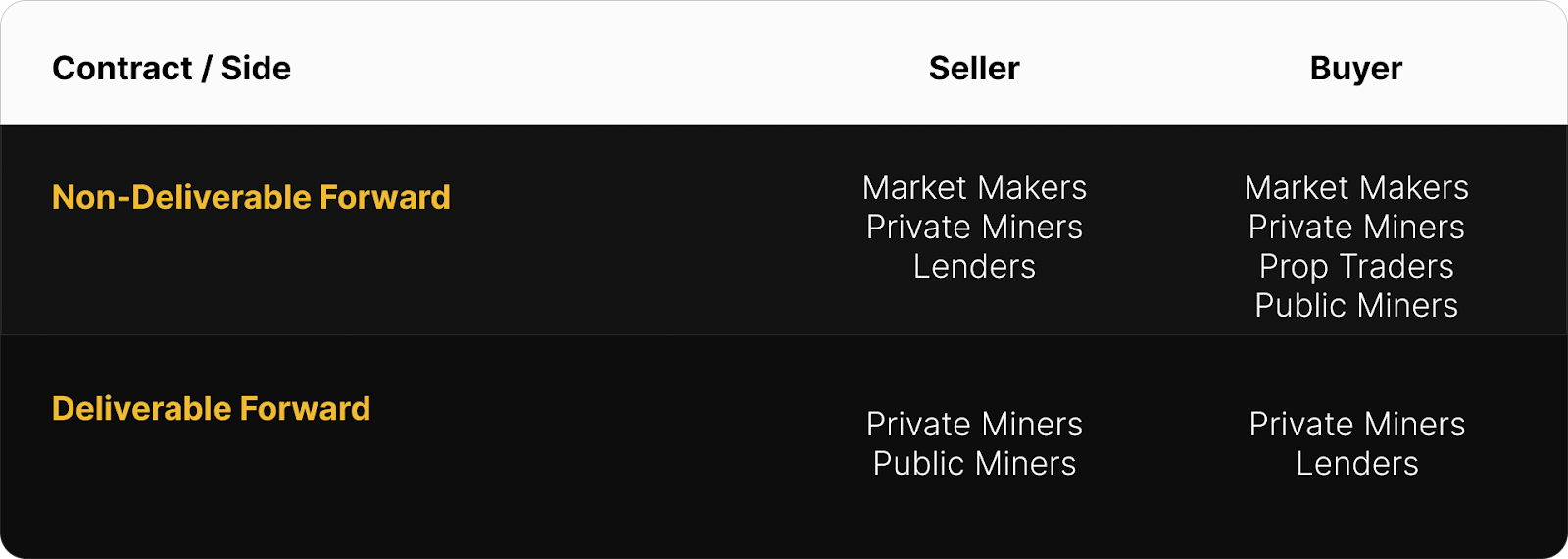

The table below shows the type of market participants on the buy and sell side of Luxor’s deliverable (DF) and non-deliverable hashrate forward (NDF) market. In June, lenders were active on the buy side of the DF market, while public and private miners used the contract to sell forward, receive financing, and expand their fleet.

Since the DF involves upfront payment, it tends to trade at a discount to the NDF (compensating the buyer for the inherent credit risk). We see the discount of DF’s relative to NDF’s as the interest rate in hashrate-based lending markets. Buyers and sellers of the DF with upfront payment can use the NDF to lock-in a fixed yield or cost of capital instead of having exposure to hashprice uncertainty.

This strategy was used by lenders (i.e., buy the DF & sell the NDF) to earn a return and by miners (i.e., sell the DF & buy the NDF) to obtain non-dilutive financing. In June 2025, that yield or cost of capital was in the 8-13% (annualized) range.

How June 2025 Hashrate Traded

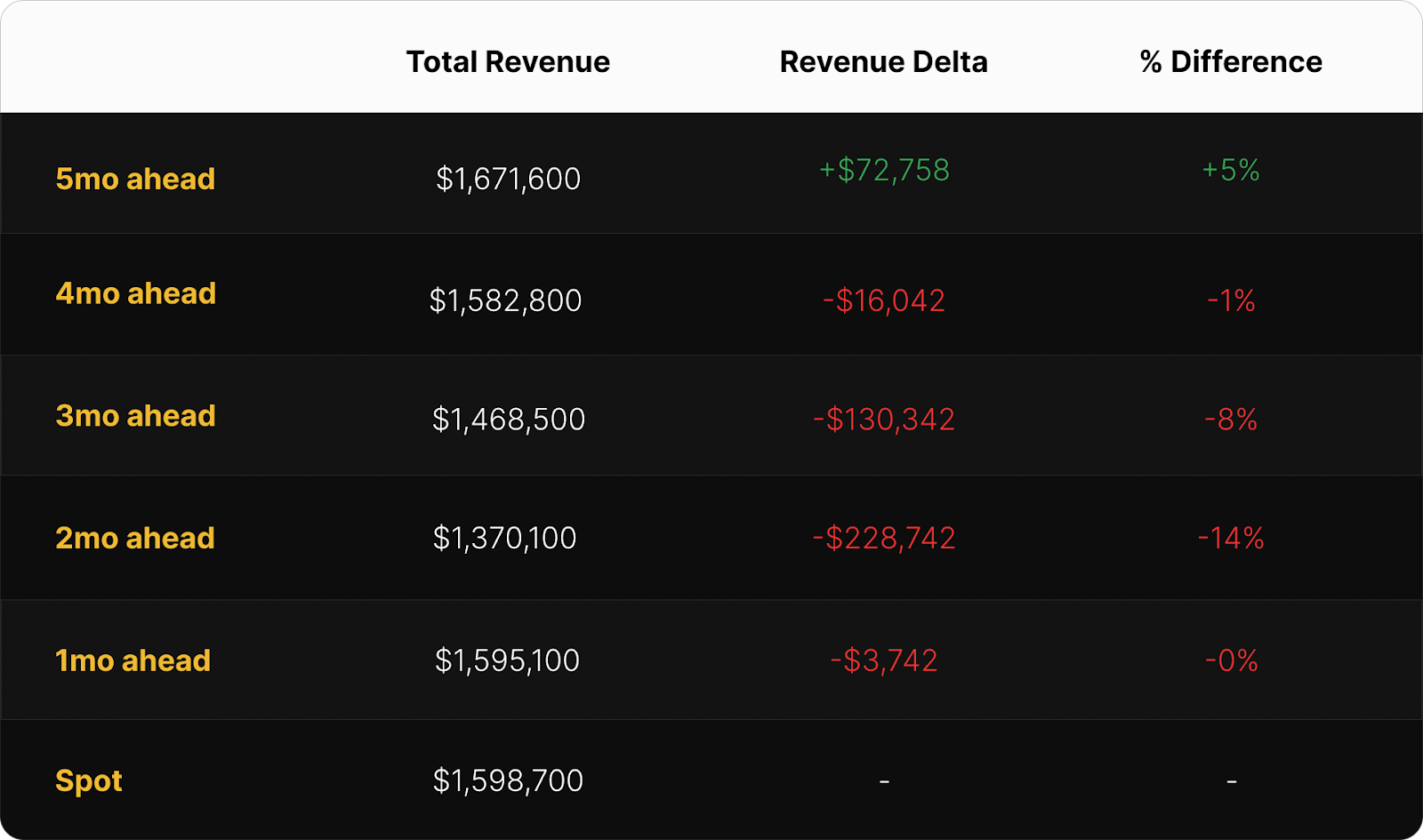

In USD terms, the June 2025 contract was a mixed bag. Only sellers who hedged very early (in January) outperformed spot FPPS payouts, locking in a fixed hashprice of $55.72 per PH/s/day before the downtrend toward $45.67 in April. As the hashrate market rebounded, buyers who entered in March or April saw the highest gains, with spot FPPS revenues reaching $53.29 per PH/s/day — well above their fixed hashcosts of $45.67–$48.95 per PH/s/day.

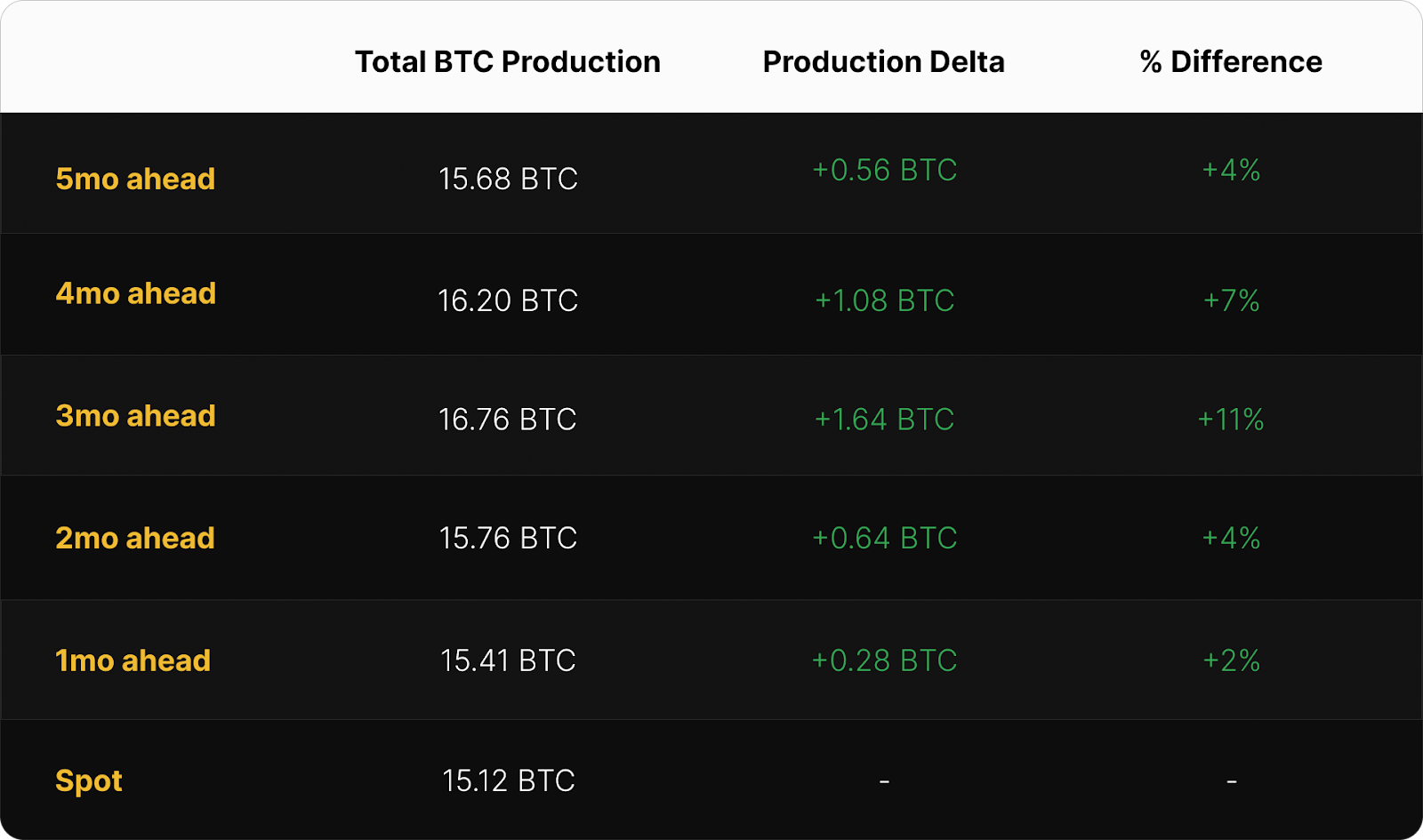

On the BTC-settled side, sellers came out ahead across the board. Late forward sales (in April or May) outperformed spot FPPS by 2-4%, while earlier hedges in January and February earned gains of ~4% and ~7%, respectively. The best performance was marked by a 3-month forward sale in March, which would have earned an additional 11% in BTC production by locking in fixed pool payouts at 0.00056 BTC per PH/s/day versus spot FPPS rates at 0.00050 BTC throughout June. Those who used upfront payouts even received immediate, non-dilutive capital in exchange for a fixed commitment to deliver hashrate over time.

The tables below summarize how a 1 EH mining operation would have performed by selling June 2025 hashrate forward — one showing USD revenue outcomes, the other showing total bitcoin production — compared to spot mining via FPPS.

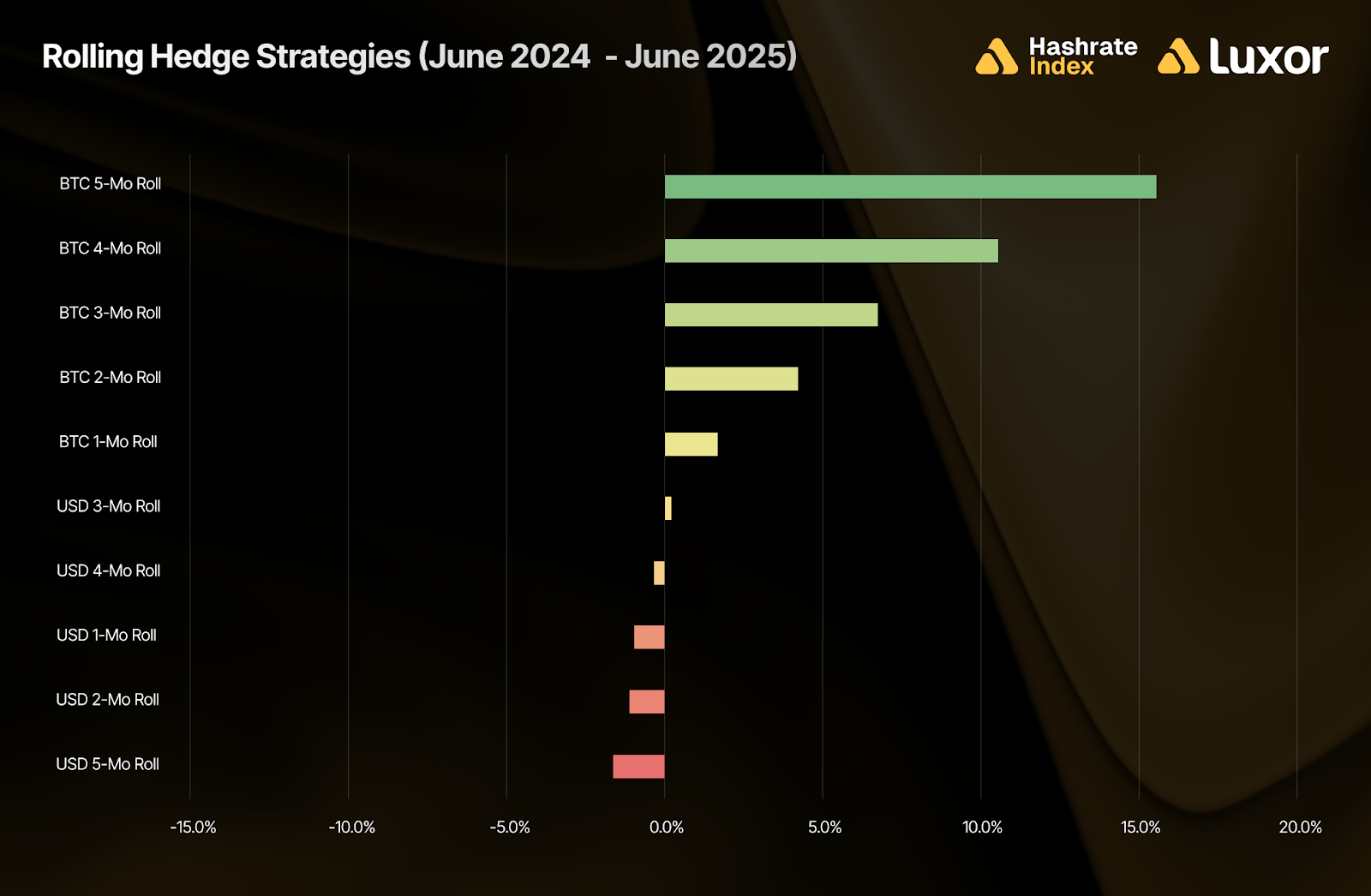

Zooming out, the following chart reveals how different rolling hedge strategies performed relative to spot mining, segmented by contract denomination and hedge horizon over the past year, from June 2024 – June 2025:

This comparison clearly shows that rolling BTC-denominated hedging strategies outperformed between June 2024 and June 2025, with the strongest results coming from 5 and 4-month forward sales. These longer-duration contracts were typically priced ahead of rising network difficulty and low fee environments, while still preserving Bitcoin price exposure. In contrast, USD-denominated hedging underperformed spot FPPS by an average of -0.8%.

Miners who locked in fixed payouts between June 2024 and June 2025 were better insulated from the hashprice decline driven by difficulty increases and weak fee activity. Those who used upfront payouts went a step further by front-loading revenue.

Note: these figures are strictly for demonstration purposes and exclude fees and bid/ask spreads associated with entering into hashrate forward contracts.

A second caveat: although selling forward proved to be favorable during timeframes shown above, it is critical to recognize that hedging is typically a cost of business rather than a revenue generation method. Hedgers willingly pay a price to buy certainty and obtain more predictable cash flows, which increases valuation, reduces cost of capital, and ultimately attracts investments.

How Future Hashrate Traded in June 2025

The two tables below summarize the evolution of hashrate forward markets during June 2025, for the subsequent five months from July 2025 – November 2025. Rows represent specific monthly hashrate contracts, while columns represent specific trading days. Cell values indicate the average daily mid-market price, except for spot prices.

Between June 2 and June 30, July to November USD-denominated hashrate forward contracts rose 8–10% as Bitcoin price strengthened and spot hashprice recovered. Similarly, BTC-settled contracts rose 4–8%, reflecting the difficulty-driven hashprice spike. Most monthly contracts traded in backwardation throughout the period, though June and July contracts showed a slight contango as the market priced in the Summer Slowdown due to 4CP season in Texas.

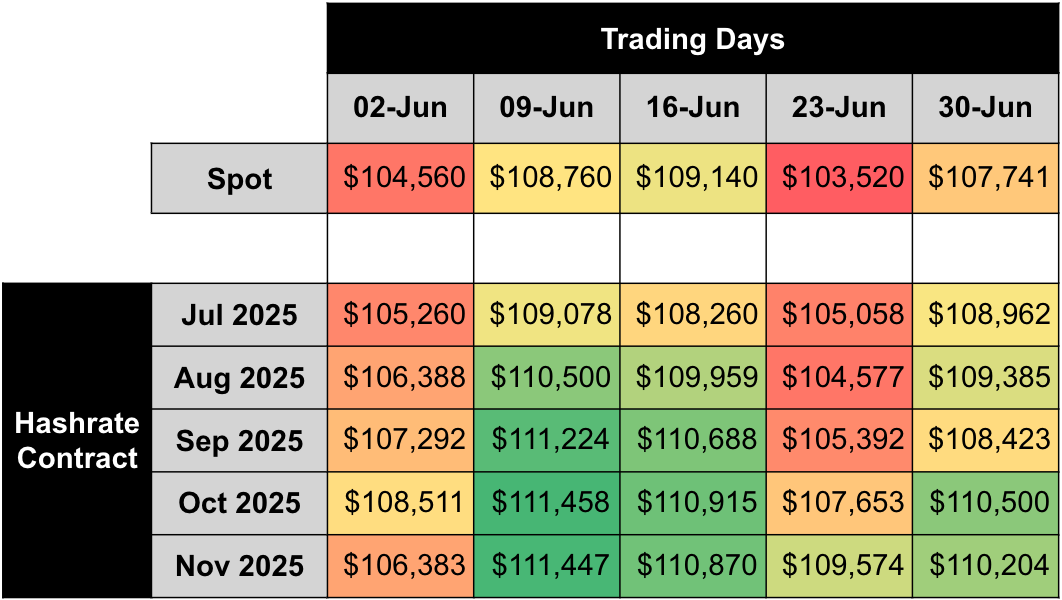

By dividing USD contract values with BTC contract values, we can use the two contracts to back out implied Bitcoin price expectations expressed by the forward market. Throughout June, implied Bitcoin price expectations traded mostly in contango and rose 1–4%, mirroring price action in spot BTC markets and indicating near-term bullish sentiment.

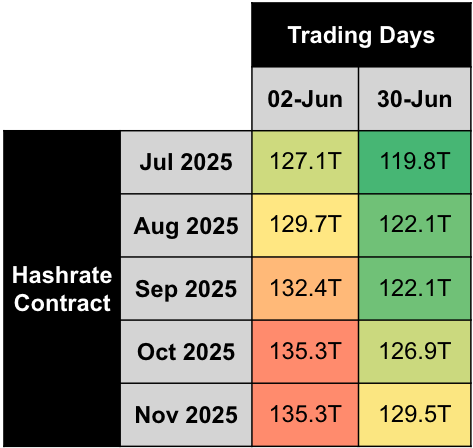

If we make an assumption around transaction fees, we can also calculate the changes in implied difficulty and network hashrate expectations expressed by the forward market. In the tables below, we assume a 0.035 BTC and 0.03 BTC per block transaction fee collection on June 02 and June 30, respectively:

Note: figures assume 0.035 BTC and 0.03 BTC per block transaction fee collection on June 02 and June 30, 2025.

Based on this simplified analysis, we estimate that future hashrate expectations slowed during the month of June, falling in the 4-8% range for the July 2025 – November 2025 contracts.

Concluding Thoughts and Looking Ahead

Since June, Bitcoin has been breaking new ground, having just marked a new all-time high price of ~$122,000 as of this morning. Consequently, hashprice is back to the $60’s for the first time since U.S. tariffs were announced. A +7.96% difficulty adjustment occurred on July 12, pushing difficulty back up to a near-all-time high level of 126.27T. Hashprice dipped from $64 per PH/s/Day to $59, and is currently hovering around $61.30.

We mentioned in last month’s Lookback that June marked the beginning of ERCOT’s Four Coincidence Peaks (4CP) program, and the impact of this behavior has already been visible. As Bitcoin miners become increasingly sophisticated power market participants, their ability to manage energy costs becomes a competitive edge.

If you are interested in learning more about mining and energy, check out our recently launched series: Energy Markets for Bitcoin Miners.

In the first post of this series, we explored how Bitcoin miners manage market exposure through spot and fixed-price power contracts. These hedging profiles offer different trade-offs: spot provides flexibility, while fixed-price power introduces cost certainty and the potential to monetize volatility through grid resale.

In the second post, we dug into a more advanced strategy: fixed-price power contracts overlaid with financial instruments, specifically short call options on power and fixed Bitcoin mining pool payouts. Together, these tools allow miners to lock-in and grow stable operating margins.

In the next few posts for this series, we’ll explore advanced strategies miners are using to deepen their exposure to power markets — and how to create value beyond producing Bitcoin.

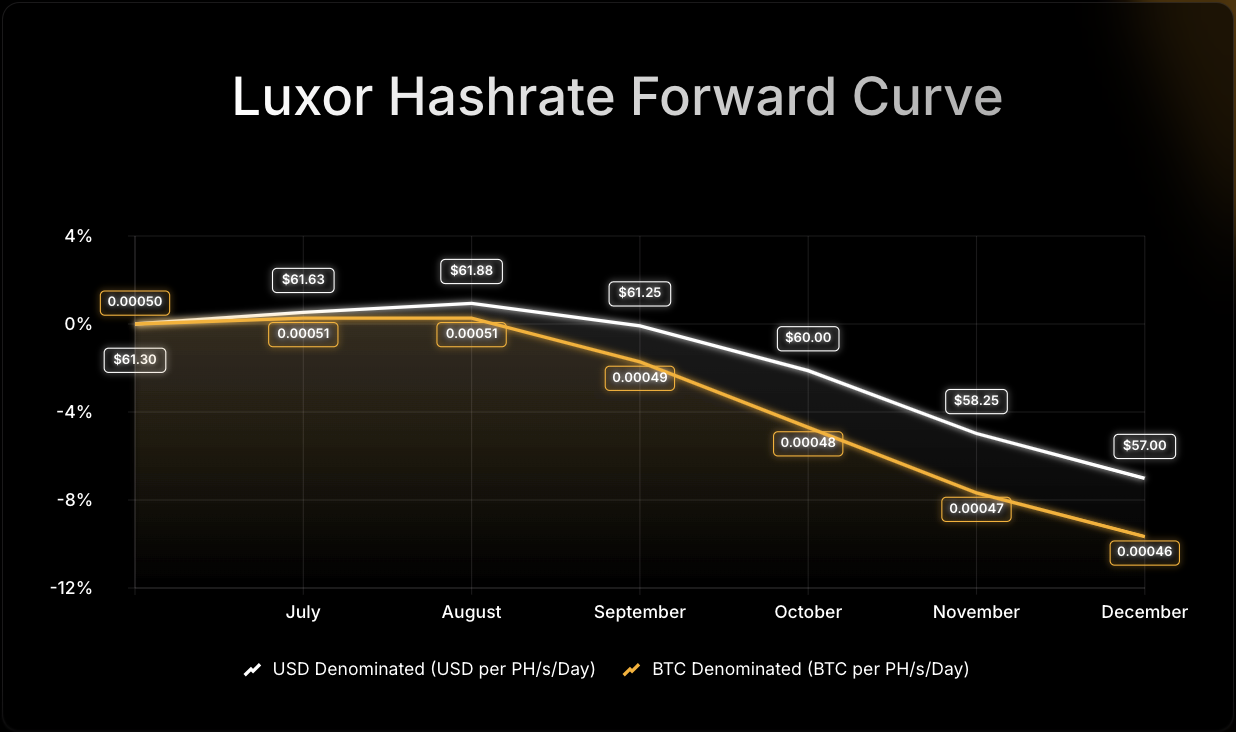

Looking forward, Luxor’s Hashrate Forward Market is pricing in an average hashprice of $60.00 or 0.00049 BTC per PH/s/day over the next six months. Sellers can currently secure this hashprice while buyers have the opportunity to lock in the same hashcost through to December 2025.

If you’d like to learn more about Luxor’s Bitcoin mining derivatives, please reach out to [email protected] or visit https://www.luxor.tech/derivatives.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}