Analyzing the Merger Between Hut 8 and US Bitcoin

One of the most significant deals in the history of bitcoin mining is taking place as we speak. Hut 8 and US Bitcoin announced they will merge, creating a North American bitcoin mining giant. The new company will go under the name Hut 8 and will be the largest public bitcoin miner by market cap, as implied by the deal size and power footprint.

This article analyzes the deal. First, we give some background on the two companies and outline the deal structure. Then, we analyze synergies between the two companies and propose a basic model for evaluating whether the deal will be accretive to shareholders.

The biggest M&A deal ever in bitcoin mining

We have seen a ramp-up of the M&A activity in the bitcoin mining industry over the past few months. Examples of recent deals include Hut 8’s acquisition of the data center operator TeraGo, Galaxy Digital’s purchase of Argo’s Helios facility, and CleanSpark’s purchases of Mawson’s Sandersville facility and Waha Technologies’ Washington facility.

All these mentioned deals are sizeable, but they don’t compare to the scale of this merger. With a total implied market cap of $990 million, this merger is the largest M&A deal in the history of bitcoin mining.

It’s a merger-of-equals transaction, meaning Hut 8 and US Bitcoin shareholders will each own approximately 50% of the combined company’s stock. Hut 8 and US Bitcoin will become wholly-owned subsidiaries of a United States-registered company named Hut 8 Corp, which will be listed on the Nasdaq and Toronto Stock Exchange. The transaction is expected to close by the end of Q2 this year.

The new company's leadership will be a mix of executives. The core group of Hut 8 executives, such as Jaime Leverton, Sue Ennis, and Shenif Visram, will remain in their positions and have US Bitcoin’s current CEO Michael Ho transitioning to a Chief Strategy Officer role, while Asher Genoot will continue as President. Later in the article, we discuss the potential advantages of mixing these executive teams.

Let’s take a look at the background of these two companies. Hut 8 is one of the leading publicly traded miners by market cap and the biggest bitcoin miner solely operating in Canada. It owns and operates two bitcoin self-mining facilities with a hashrate of 2.5 EH/s and five high-performance computing data centers it acquired in early 2022.

Just like Hut 8 is a Canada-only miner, US Bitcoin operates only in the United States. It’s one the most reputable private bitcoin mining companies, operating four mining sites through various structures. For being a bitcoin miner, the company has a relatively diverse revenue stream, spanning self-mining, hosting, and infrastructure management. US Bitcoin was a relatively unknown brand until 2022, when they stepped into three new sites previously operated by bankrupt Compute North, putting them onto investors' radars.

The marriage of Hut 8 and US Bitcoin will create one of the biggest bitcoin mining companies in the world. It will boast a total installed self-mining capacity of 5.6 EH/s, 220 MW of hosting infrastructure, and 680 MW of managed infrastructure operations across six sites in the United States and Canada.

Why are Hut 8 and US Bitcoin merging?

The purpose of a merger is to leverage synergies between two companies. These synergies can include reducing costs through economies of scale, reducing risk through diversification, and increasing efficiency due to know-how sharing. This section discusses some of the alleged synergies Hut 8 and US Bitcoin could benefit from by joining forces.

Reducing administrative expenses

Administrative expenses are costs that don’t directly contribute to revenues. It’s a broad category that includes executive compensation, consulting fees, legal fees, insurance costs, etc. In financial statements, you can find these costs under the category SG&A.

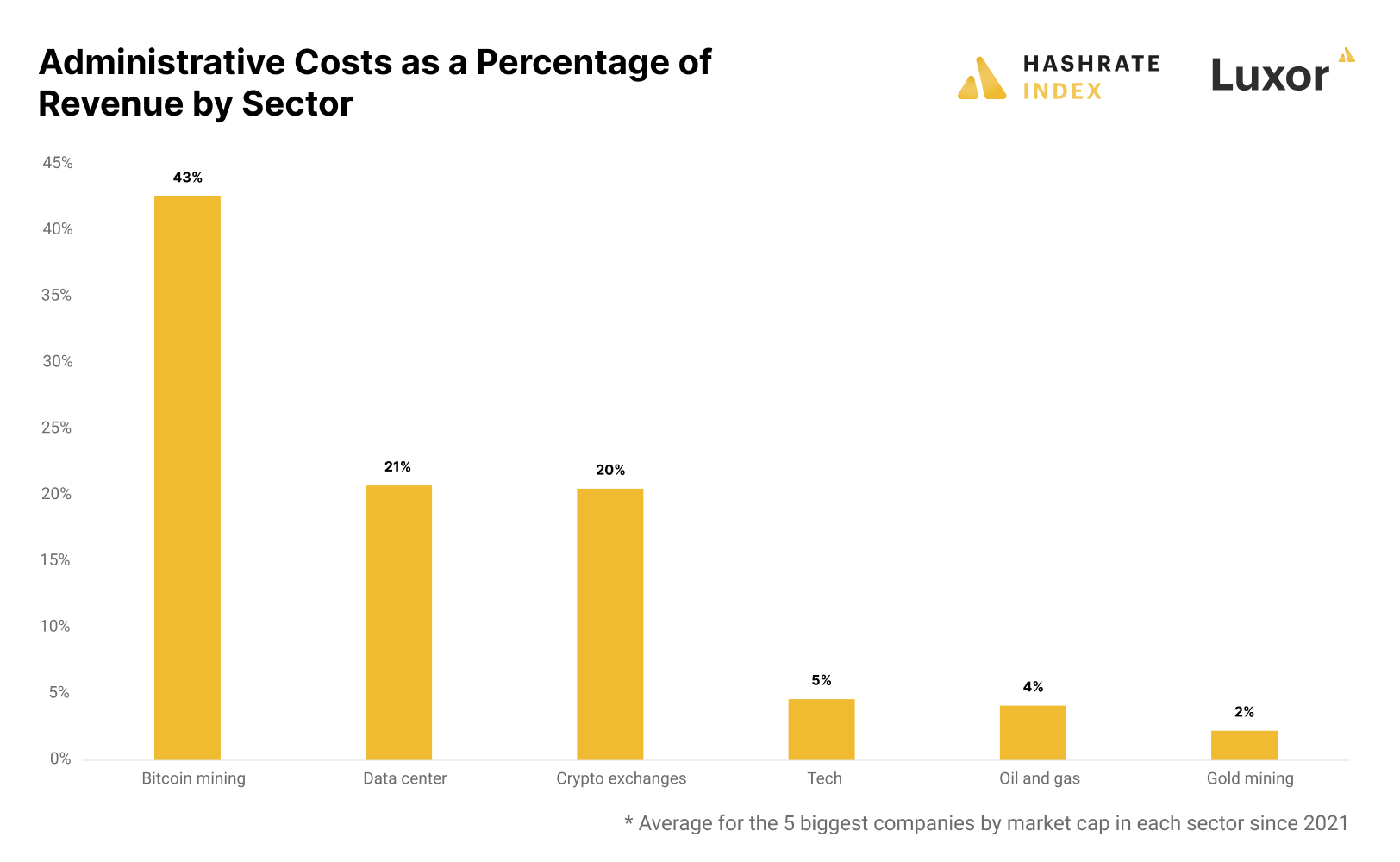

As we revealed in a recent article, administrative costs for public bitcoin mining firms have historically been elevated relative to those of companies from comparable sectors. Since 2021, Hut 8’s administrative costs have made up 25% of its revenues, which is lower than most of its competitors. Still, this number averages between 2% and 4% in more mature industries like gold mining or oil and gas, proving that Hut 8 has significant room for administrative cost-cutting.

By merging two executive teams into one and sharing consulting and legal fees, Hut 8 and US Bitcoin will likely significantly reduce their administrative overload - a classic example of leveraging economies of scale.

This is a tangible and actionable cost-saving synergy that we think is important for many public miners to consider when exploring M&As.

Reducing per-unit equipment costs due to economies of scale

During the first nine months of 2022, Hut 8 invested C$138 million in plant and equipment. These equipment investments include mining rigs, electrical gear, and more. Anyone involved in procurement knows that scale is king, as generally, the more units you purchase - the lower your unit price.

By merging, Hut 8 and US Bitcoin can leverage economies of scale when purchasing equipment, allowing them to secure more favorable procurement deals with their suppliers.

In addition, US Bitcoin can now lower its ASIC repair costs by taking advantage of Hut 8’s in-house MicroBT-certified repair center.

Improving access to capital

Like in any other capital-intensive industry, access to capital is a cornerstone of a successful bitcoin mining business. Several factors determine a company’s access to capital - the most important being the trading volume in the stock and the company’s valuation relative to its cash flow.

A company must have certain liquidity in its stock to attract large institutional investors who want to move in size and must have a specific valuation to be included in indices. Hut 8 currently has a market cap of $400 million and is, per definition, a small cap. In addition, the stock’s average daily trading volume in 2022 has only been $27 million. The stock’s low market cap and trading volume have made it hard for them to attract large investors.

Meanwhile, Marathon has attracted investment from the most prominent investors globally, including BlackRock, Vanguard, and State Street, boosting its market cap and giving it the best access to capital in the bitcoin mining industry. Around 41% of Marathon’s stock is held by institutional investors, compared to only 10% for Hut 8.

With an implied market cap of $960 million, the combined Hut 8 and US Bitcoin will be of similar size as Marathon. The higher market cap will likely make the company more attractive to institutional investors, significantly improving its access to capital. In addition, the merger will effectively take the private company US Bitcoin public.

Sharing intellectual property and know-how

Intellectual property and know-how are critical factors for the long-term success of a bitcoin mining company. Like in any industry, some bitcoin mining companies have great know-how in certain areas while being weaker in others.

The Hut 8 and US Bitcoin teams have complementary experience and expertise in different areas. Hut 8 has been a public company since 2018 and has tremendous experience in public markets and corporate governance, while US Bitcoin has been highly focused on energy and software development. Hut 8 can now implement US Bitcoin’s proprietary energy and miner management systems, while US Bitcoin can leverage Hut 8’s capital markets expertise.

Reducing revenue risk by diversification

Long-term successful companies are not only focused on growing their revenues but also on lowering their revenues' volatility. Companies reduce their revenue risk by striving to get multiple sources of revenue.

Both Hut 8 and US Bitcoin have diversified revenue streams. Most of Hut 8’s revenues come from self-mining bitcoin, but it also has a rapidly growing high-performance computing division. US Bitcoin has self-mining, hosting, and managed infrastructure segments. The merged company will have the most diversified revenue stream in the bitcoin mining industry, with a significant share of the revenue less tied to ongoing capital expenditure. This could make the company even more attractive to traditionally risk-averse, institutional investors.

Reducing jurisdictional risk by diversification

During the past few years, specific US states, Canadian provinces, and even countries have expressed opposition to the bitcoin mining industry by increasing power taxes, imposing moratoriums, or even outright banning mining. After seeing these developments, bitcoin miners are becoming increasingly aware of the importance of minimizing jurisdictional risk.

“Don’t put all your ASICs in one basket” is a proverb we often hear during conversations with bitcoin miners. Spreading out a mining operation in various countries is the only way to reduce jurisdictional risk, and we expect it to become an important theme in the coming years.

Both these companies are currently exposed to significant jurisdictional risk by only being located in one country. As a Canada-only miner, Hut 8’s jurisdictional risk is particularly high as the Canadian government has grown increasingly hostile toward the industry. US Bitcoin operates in the more benign United States but still has problems in New York on the state and municipal levels.

The merged company will be more geographically diversified, with operations spread across two countries and six provinces and states. We think it's important for mining companies to geographically diversify as much as possible, including overseas, such as Bitfarms in Latin America and Hive in Northern Europe.

How can we determine whether a merger is accretive to shareholders?

In the previous section, we outlined some of the proposed synergies between Hut 8 and US Bitcoin. Synergies are important, but other considerations also play a role when determining whether an M&A transaction is desirable for shareholders.

An accretive M&A transaction refers to an incremental benefit that occurs to the post-deal company. We typically consider a deal accretive if the earnings per share (EPS) increase after the transaction, although we sometimes use other industry-specific metrics. Given the mining industry trades on valuation multiples higher up on the P&L, a EV/EBITDA or similar metric could also be used. In contrast, a transaction is dilutive if it leads to a decline in the EPS.

Building an accretion-dilution model requires the standalone financials of both companies, an assumption of financial synergies, and information on the capital structure. Ideally, it also incorporates a forward-looking estimate. At the basic level, if (Company A Profit + Company B Profit + Profit from Synergies - Transaction Expenses) / (Post-transaction share count) is higher than the EPS, the deal is accretive.

In other words, for the deal to be accretive to both the shareholders of Hut 8 and US Bitcoin, the merged company’s EPS must be higher than that of the individual companies pre-merger. This model is very quantitative, and it’s critical to remember that sometimes qualitative aspects make or break an M&A transaction.

We have outlined the model here, and we look forward until US Bitcoin discloses their financials so we can quantify whether this deal is accretive to shareholders or not.

Conclusion

Hut 8 and US Bitcoin are merging into one of the largest bitcoin mining companies in the world. This M&A deal is the biggest in the history of bitcoin mining, and follows a series of smaller deals throughout 2022 and early 2023.

By joining forces, Hut 8 and US Bitcoin can leverage several synergies, including reducing costs through economies of scale, reducing risk through revenue and jurisdictional diversification, and increasing efficiency due to know-how sharing.

After doing this back-of-the-napkin analysis, we believe the deal makes a lot of sense for both companies. Still, to quantifically evaluate whether the deal is accretive to shareholders or not, we must do an accretion-dilution analysis. We outlined the recipe for making such a model, while we are waiting patiently for US Bitcoin to disclose their financials.

We believe we will see several sizeable M&A transactions in the bitcoin mining industry in 2023. Many companies could leverage significant economies of scale by merging with or acquiring competitors, particularly on the administrative cost side. Also, many bitcoin mining companies will likely want to diversify their revenues by segments or geographies. The easiest way to achieve this is to buy a competitor operating in a different segment or jurisdiction.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}