Hashrate Derivatives Monthly Lookback - September 2024

September 2024’s hashrate and hashprice trends, forward market participation, trading activity and contract performance.

Luxor’s Derivatives Monthly Lookback Series is a deep dive into Bitcoin hashrate forward market activity. In this post, we cover September 2024’s hashrate and hashprice trends, forward market participation, trading activity and contract performance.

Summary

- For a second consecutive month, spot Bitcoin miners faced a challenging Bitcoin hashprice environment.

- The top-performing miners in September were those who hedged early. Miners who hedged USD revenues in April earned 40% more, and those who hedged Bitcoin production earned 27% more.

- A key question for mining companies and investors is why they didn't hedge before hashprice hit record lows. Given Bitcoin mining's capital intensity and revenue volatility, executives and investors should demand answers. In other volatile industries, hedging is standard practice – it reduces volatility, decreases cost of capital, and increases valuations.

September 2024 Hashprice & Constituents

For a second consecutive month, spot Bitcoin miners faced a challenging Bitcoin hashprice environment. Both USD and BTC-denominated monthly average hashprice hit a post-2017 low. Month over month, average USD hashprice fell by 2.7% from $43.54 per PH/s/Day in August to $42.37 per PH/s/Day in September, while average BTC hashprice fell by 2.8% from 0.00072464 BTC per PH/s/Day in August to 0.00070408 BTC per PH/s/Day in September.

However, the environment improved as the month progressed: Bitcoin price rose, network difficulty fell and transaction fees increased (albeit ever so slightly). USD-denominated hashprice started the month at $41.48 per PH/s/Day, bottoming at $38.67 on September 7, peaking at $47.99 on September 28, and closing out the month at $46.26.

While the average month over month Bitcoin price was flat at ~$60,100, the increase in USD hashprice during September largely mirrored the rise in Bitcoin’s price. Bitcoin price began the month at $58,231, bottoming at $54,232 on September 7, peaking at $65,765 on September 28, and closing out the month at $64,022.

Network difficulty oscillated throughout September – beginning at 89.47T, rising by 3.6% to an all time high of 92.67T on September 10, and falling by 4.6% to 88.40T on September 25. In addition to challenging mining economics, there were a couple of reasons for the fall in difficulty during September. First, miners in Texas (~17% of global network hashrate) curtailed energy usage and reduced hashing during peak hours, as they anticipated 4CP for the month of September. As seasons shift from Summer into Fall and we come out of the usual 4CP period in Texas (June-September), we expect to see more hashrate growth in the near term.

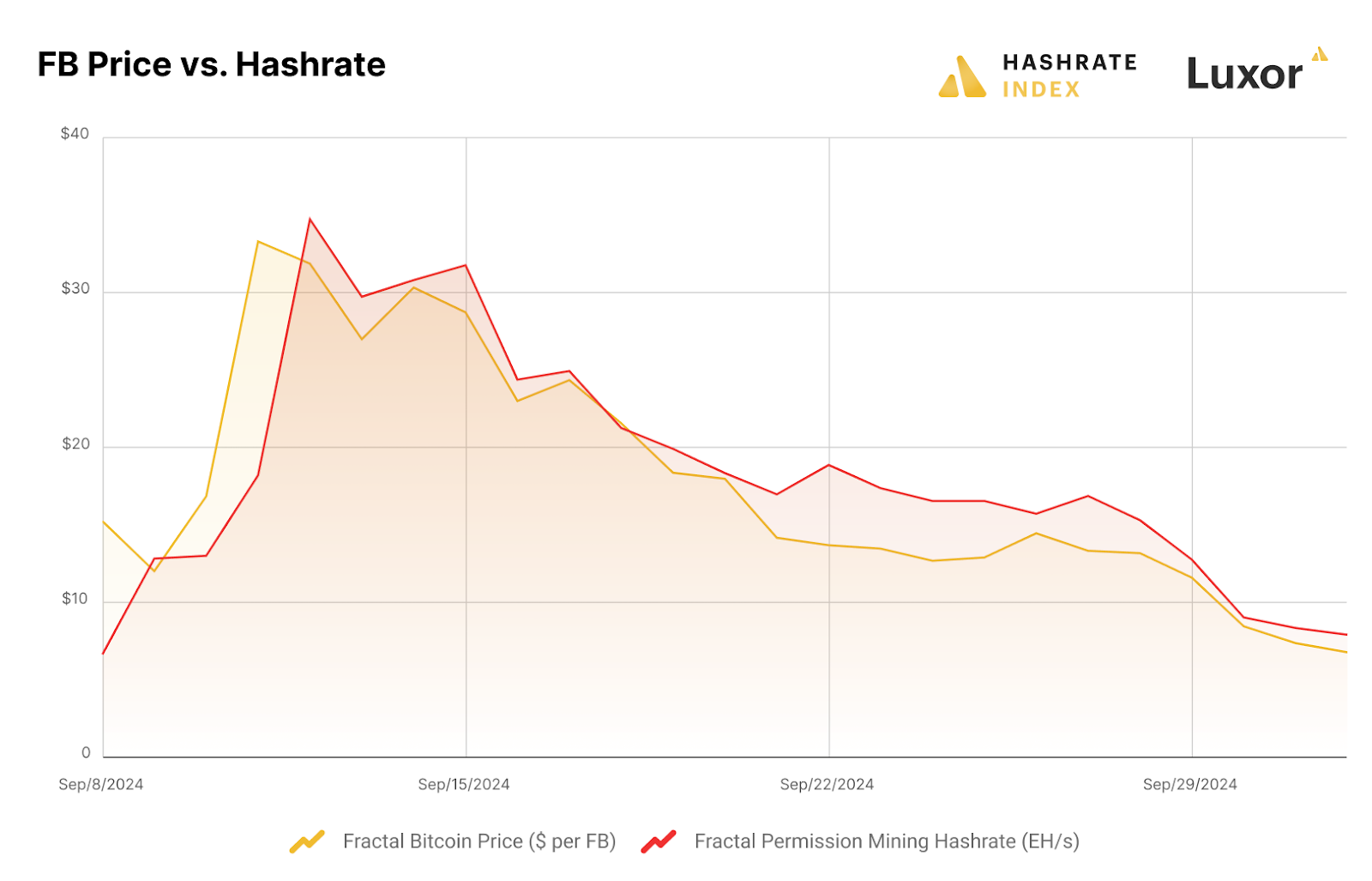

More interestingly, Fractal – a new Bitcoin sidechain – temporarily offered miners higher revenue for SHA-256 hashrate after its launch on September 9. The difference in revenue quickly closed as approximately 35 EH of Bitcoin miners moved over to Fractal mining by September 12.

The chart below shows Fractal Bitcoin (FB) price versus Fractal mining hashrate. We can observe a clear relationship between Fractal price and hashrate, wherein network hashrate follows price. During the Bitcoin difficulty epoch between September 10 - 25, an average of ~22 EH was mining on Fractal, which contributed to the downward difficulty adjustment on September 25. Since launch, Fractal has demonstrated the usual altcoin pattern of a quick spike followed by price deterioration, falling to ~$8 in price and 8 EH in hashrate on October 2. If Fractal Bitcoin price and hashrate remain at these levels, we estimate that ~12 EH of SHA-256 miners moving back to Bitcoin would have a ~1.8% positive (i.e., upward) impact on the next difficulty adjustment.

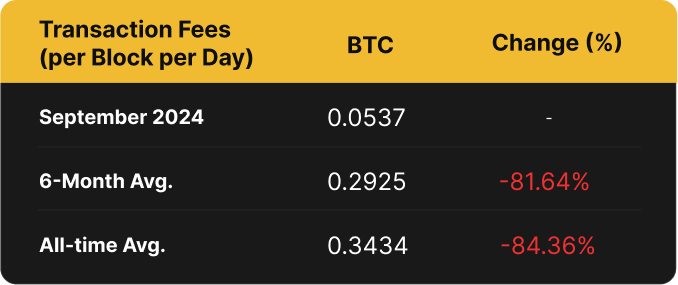

Throughout September, the transaction fee bear market continued to grind lower. Average transaction fees per block per day were 0.054 BTC – a 30% decline from the previous month and the lowest monthly average since 2012. In fact, transaction fees collected throughout the month of September were ~84% lower than the all-time historical average since Bitcoin’s Genesis block.

But there is some hope: the second cap of Babylon Bitcoin staking mainnet Phase-1 is scheduled to open on 9 October 2024, starting at block height #864790, which may create volatility in transaction fees.

As a result of oscillating difficulty and relatively flat transaction fees, we observed oscillating BTC-denominated hashprice throughout the month of September. BTC-denominated hashprice started at 0.00071238 BTC per PH/s/Day, fell by 3.52% to 0.00068732 BTC per PH/s/Day, and recovered to 0.00072253 BTC per PH/s/Day.

September 2024 Forward Market Activity

Our analysis of the September forward hashrate market focuses on two key points: how the September 2024 hashrate contract traded in previous months and how the forward curve shifted in September based on trades for forward hashrate during the month.

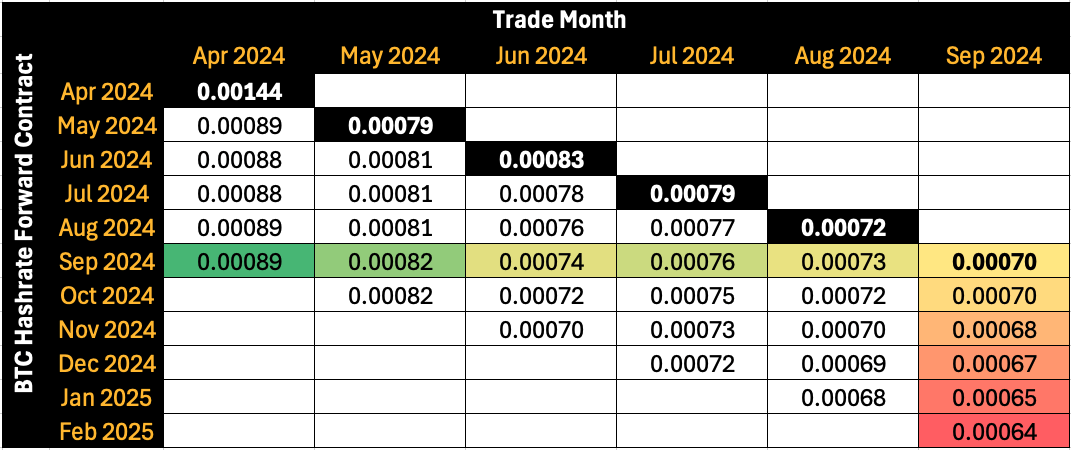

The two tables below show the evolution of USD and BTC-denominated Bitcoin hashrate forward markets throughout April - September 2024. Rows represent specific monthly contracts, while columns represent each trading month. Cell values indicate the average monthly mid-market price, except for the bold highlighted main diagonal, which shows actual hashprice settlement in each month. This table summarizes both the trading history of the September 2024 contract (colored row) and the forward curve in September (colored column).

Observing the colored row in the first table (USD) above, we can see how the September 2024 contract traded in each month compared to the actual $42.37 per PH/s/Day settlement. Given these values, we can make observations around how a specific contract would have performed relative to when it was traded, in addition to how a specific strategy of trading contracts (e.g., a 6-month rolling vs. 1-month rolling) would have performed versus spot hashprice. Finally, the colored column shows the shape of the forward curve during the month of September (i.e., trading in backwardation for this instance).

How September 2024 Hashrate Traded

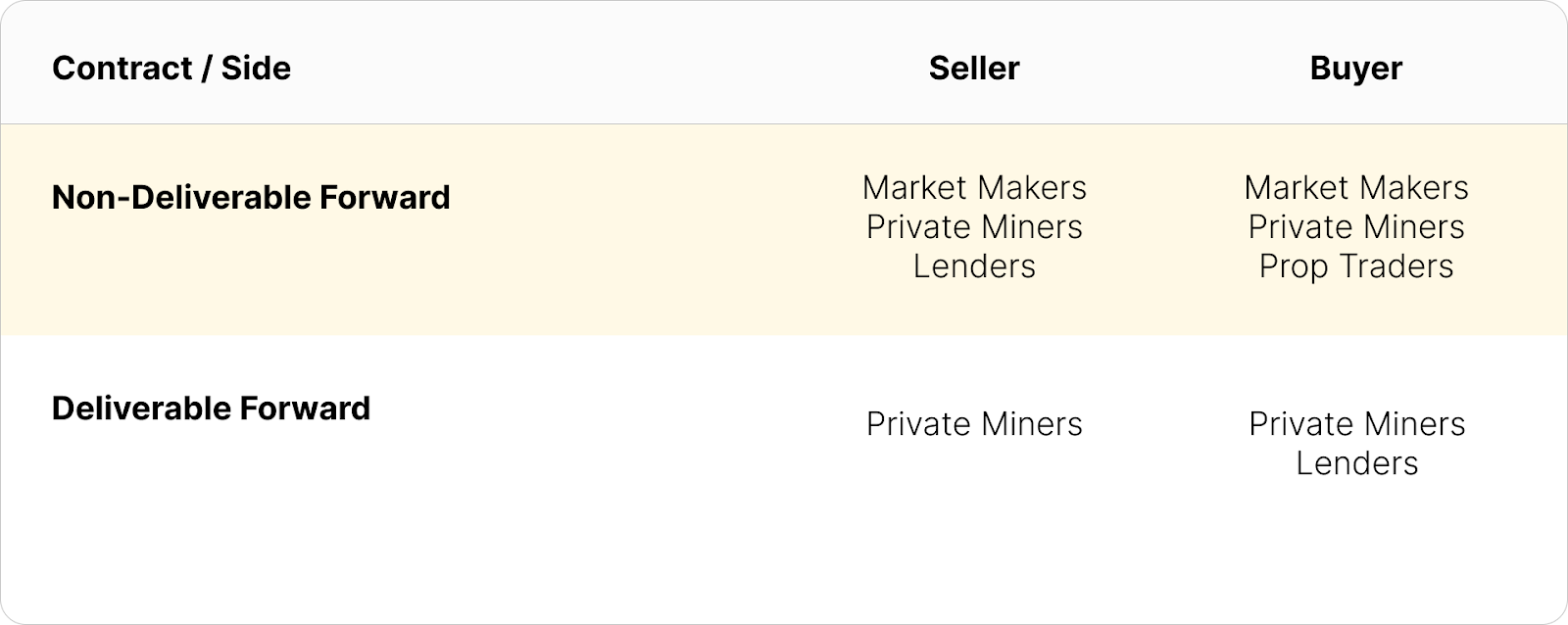

The September 2024 contract was traded by a diverse set of market participants. The primary sellers of both the deliverable (DF) and non-deliverable (NDF) September 2024 hashrate forward contracts were private mining companies, as well as lenders and market makers. Private miners were selling the NDF to hedge their revenue and selling the DF to finance upgrades in newer generation hardware.

On the other hand, lenders were using the NDF to lock in a yield on DF purchases with upfront payment. We see the discount of DF’s relative to NDF’s as the interest rate in hashrate-based lending markets. Buyers and sellers of the DF with upfront payment can use the NDF to lock-in a fixed yield (i.e., cost of capital) instead of having exposure to the uncertain and variable returns of hashprice. In September 2024, that yield or cost of capital was in the 11-13% annualized range.

Buyers of the deliverable (DF) and non-deliverable (NDF) September 2024 hashrate forward contracts involved all types of industry players: both public and private miners as well as proprietary traders bought these contracts to temporarily increase their hashrate exposure.

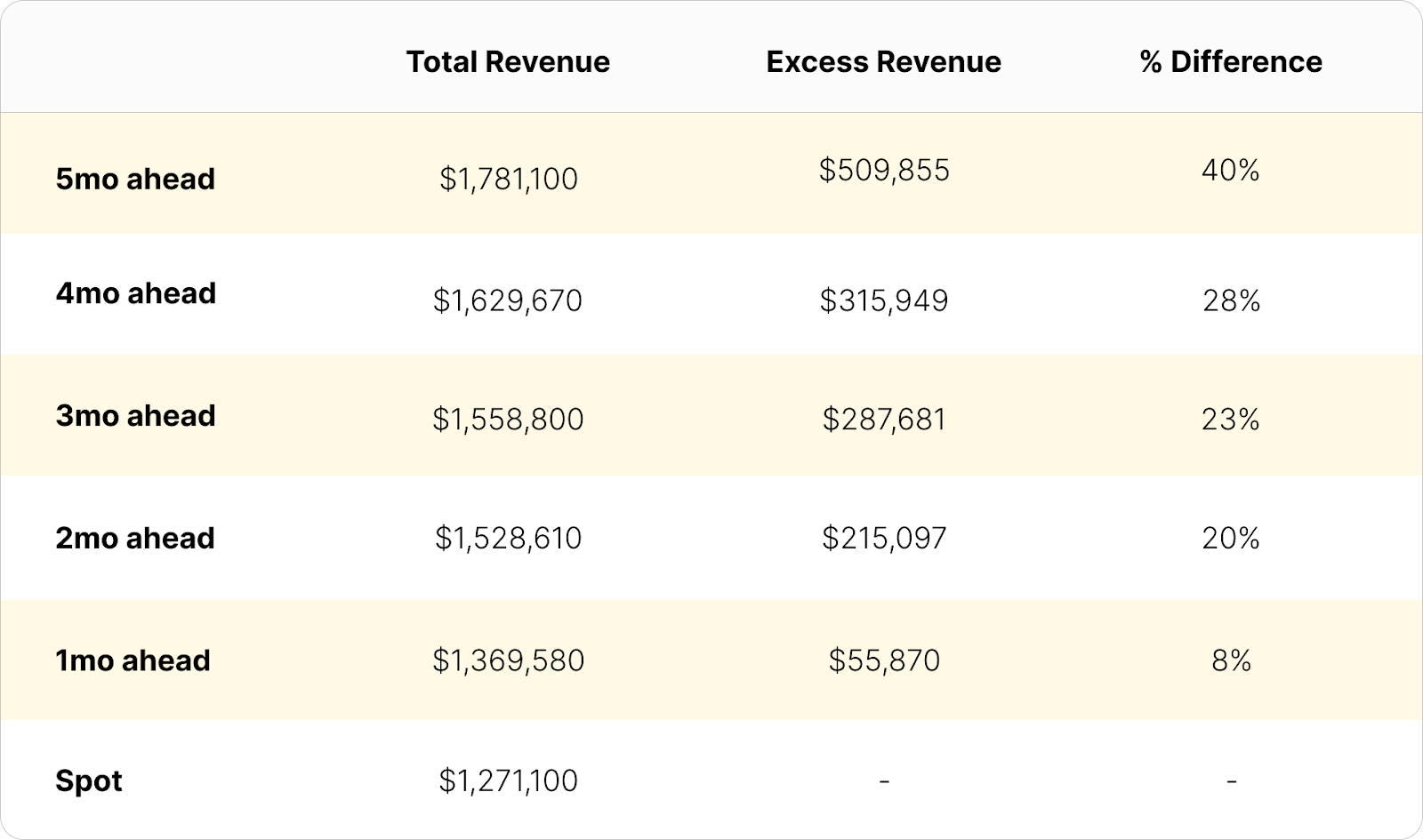

The top-performing miners in September were those who hedged early. Spot Bitcoin miners and hashrate buyers suffered the most as hashprice hit a record low. In USD, hedged miners saw higher revenues, while in BTC, they produced significantly more Bitcoin. For instance, miners who hedged USD revenues in April earned 40% more, and those who hedged Bitcoin production earned 27% more.

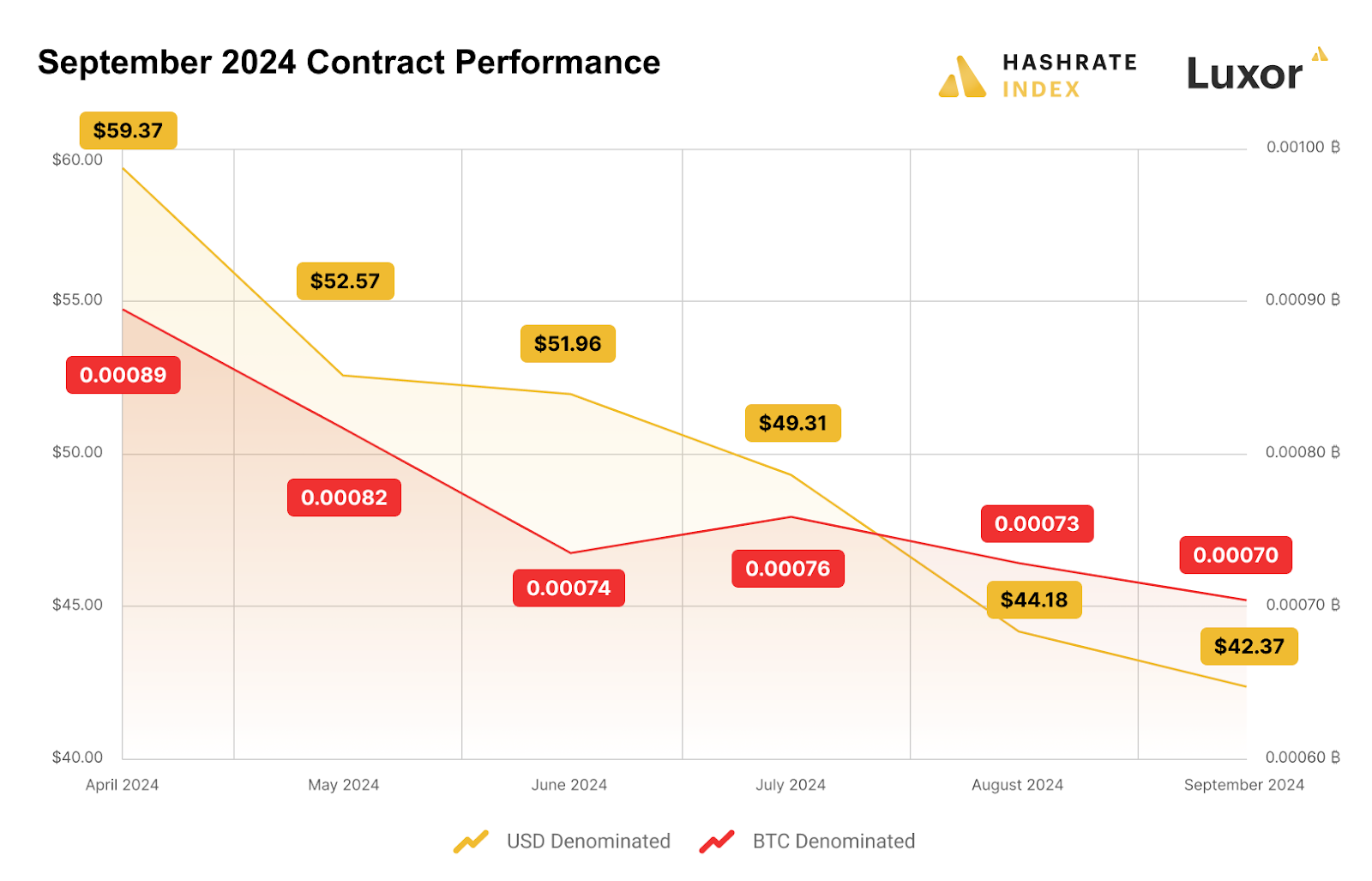

The figure below summarizes how a 1 EH mining operation would have performed, had it sold September 2024 hashrate forward versus mining spot during the month.

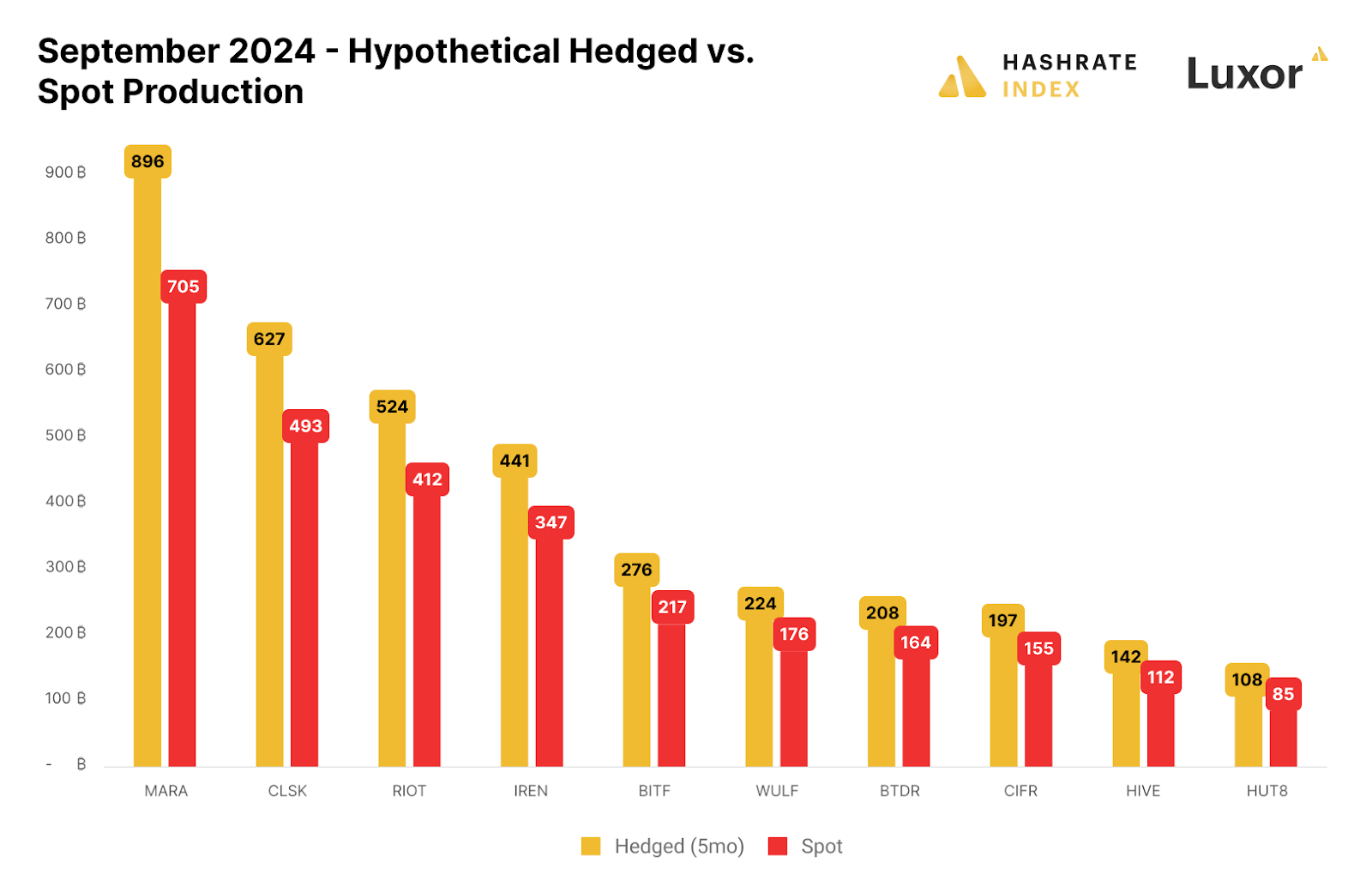

Similar to August, public mining companies were not selling September hashrate forward – yet again, an unfavorable position to be in. The figure below illustrates a hypothetical scenario of how public miners' September production would have differed if they had hedged in April 2024, right before the halving:

Please note: this figure is strictly for demonstration purposes and based on the simplifying assumption of multiplying actual production figures by the percentage difference between hashrate forward contracts’ locked-in hashprice versus spot hashprice; it excludes fees and bid/ask spreads associated with entering into hashrate forward contracts.

A second caveat: although selling forward proved to be favorable in this instance, it is critical to recognize that hedging is typically a cost of business rather than a revenue generation method. Hedgers willingly pay a price to buy certainty and obtain more predictable cash flows, which increases valuation, reduces cost of capital, and ultimately attracts investments.

How Hashrate Forward Traded in September 2024

During the month of September itself, the set of participants was a little less diverse. The sell side was predominantly private miners looking to lock-in hashprice, either to protect margins or to borrow and temporarily expand hashrate. On the other hand, the buy side consisted of private miners, lenders and speculators looking to profit on a rebound from all-time low hashprice.

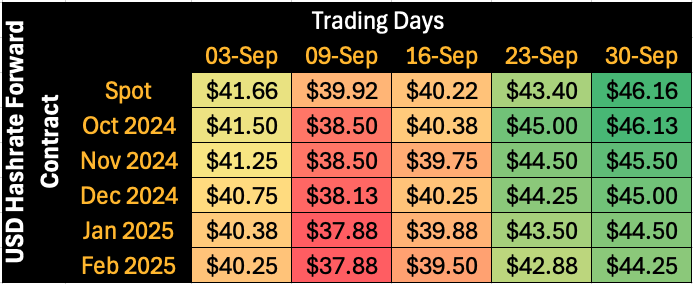

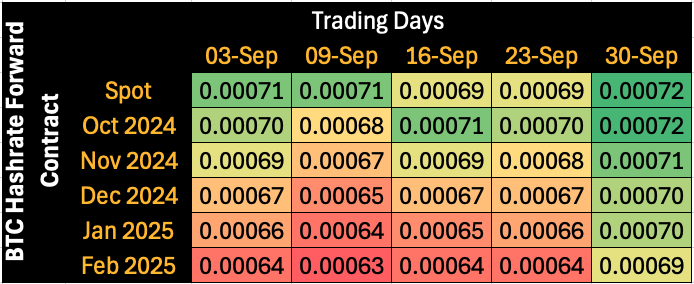

The two tables below summarize the evolution of Bitcoin hashrate forward markets during September 2024, for the subsequent five months from October 2024 through February 2025. Rows represent specific monthly hashrate contracts, while columns represent specific trading days. Cell values indicate the average daily mid-market price, except for the spot hashprice.

Looking at the color scale across each row, we can observe how market expectations around future months evolved throughout each trading day. For example, the month of February 2025 was priced at $40.25 on September 3 2024, however it gradually increased to $44.25 on September 30 as hashprice rose and mining economics improved. Looking at the color scale across each column, we can observe the shape of the forward curve during each trading day. For example, on September 23 2024, the front month (October 2024) for the BTC-denominated contract was trading in contango, whereas months further out into the future were trading in backwardation.

Throughout September, forward USD hashprice moved up in line with the rise in spot hashprice. Bitcoin prices tend to move the entire hashprice curve, whereas changes in transaction fees and expectations around network difficulty tend to have a more limited impact on certain parts of the curve.

Looking Ahead and Concluding Thoughts

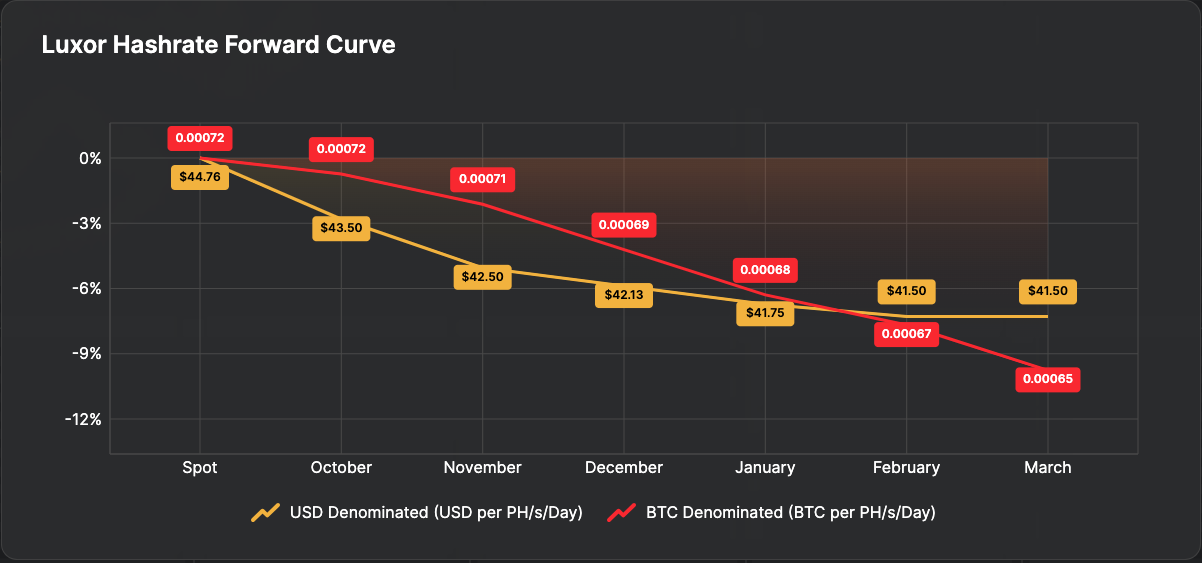

Looking forward, both USD and BTC contracts are currently trading in backwardation throughout October 2024 - March 2025. Miners may lock in a ~$42.15 hashprice for up to six months into the future. Our derivatives desk is currently seeing upfront payments and financing deals through the DF at a 10-13% (annualized) discount to the NDF curve.

As hashprice continues to hover around all-time lows, miners may consider the benefits of selling forward: hedging against hashprice falling even lower than current levels and locking in healthy margins per unit of electricity (i.e., on a kWh basis) for those operators with newer generation ASIC fleets. On the other hand, buy side participants may find the current hashprice environment to be an attractive entry point for gaining more exposure to hashrate.

Selling September 2024 hashrate forward prior to the month of September turned out to be profitable for miners hedging their production. The further out a miner hedged, the better their performance would have been.

A key question for mining companies and investors is why they didn't hedge before hashprice hit record lows. Given Bitcoin mining's capital intensity and revenue volatility, executives and investors should demand answers. In other volatile industries, hedging is standard practice – it reduces volatility, decreases cost of capital, and increases valuations.

If you’d like to learn more about Luxor’s Bitcoin mining derivatives, please reach out to [email protected] or visit https://www.luxor.tech/derivatives.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}